Cash flow is the movement of cash into or out of a business, project, or financial product. It is usually measured during a specified, finite period of time. Measurement of cash flow can be used for calculating other parameters that give information on a company's value and situation. Cash flow can e.g. be used for calculating parameters:

To determine a project's rate of return or value. The time of cash flows into and out of projects are used as inputs in financial models such as internal rate of return and net present value.

To determine problems with a business's liquidity. Being profitable does not necessarily mean being liquid. A company can fail because of a shortage of cash even while profitable.

As an alternative measure of a business's profits when it is believed that accrual accounting concepts do not represent economic realities. For example, a company may be notionally profitable but generating little operational cash (as may be the case for a company that barters its products rather than selling for cash). In such a case, the company may be deriving additional operating cash by issuing shares or raising additional debt finance.

Cash flow can be used to evaluate the 'quality' of income generated by accrual accounting. When net income is composed of large non-cash items it is considered low quality.

To evaluate the risks within a financial product, e.g. matching cash requirements, evaluating default risk, re-investment requirements, etc.

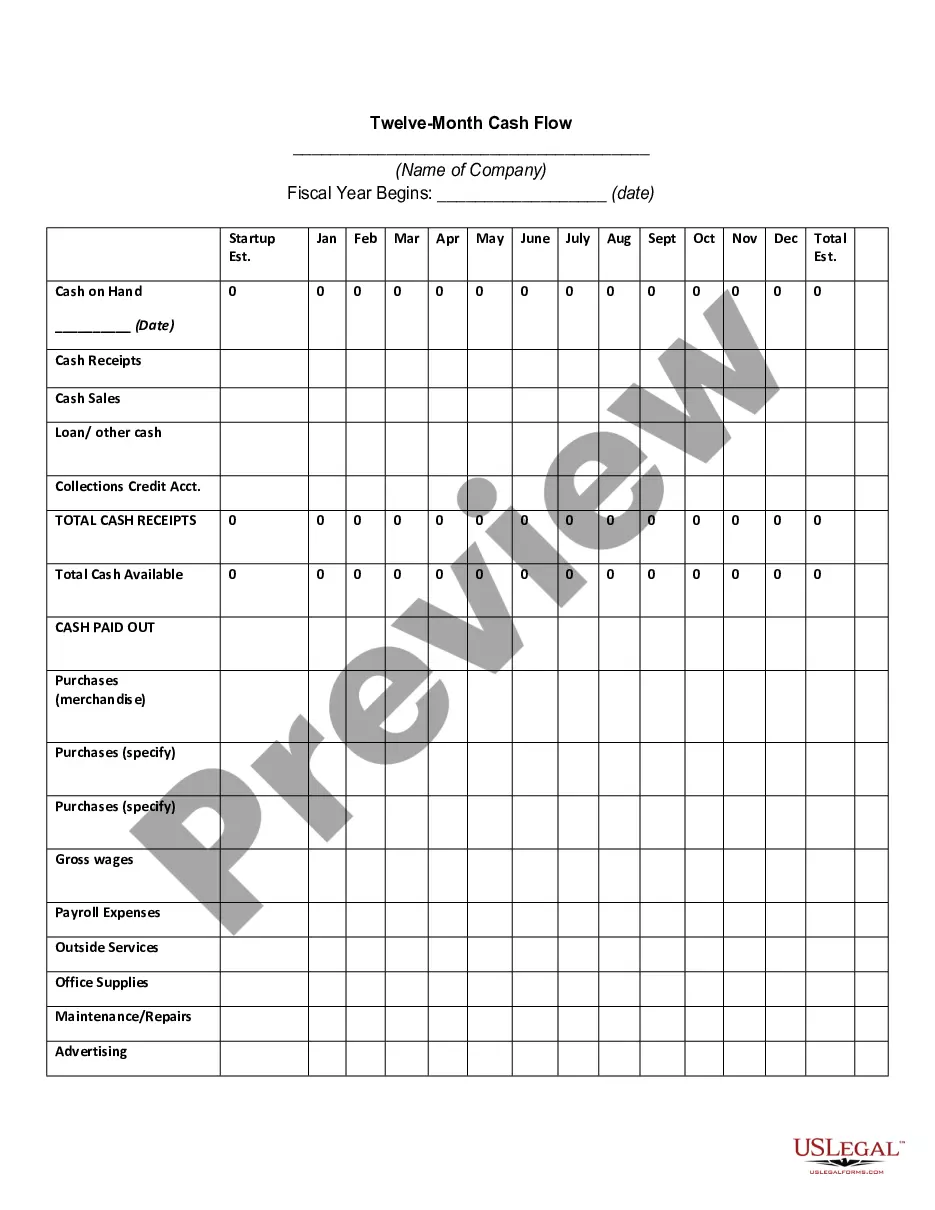

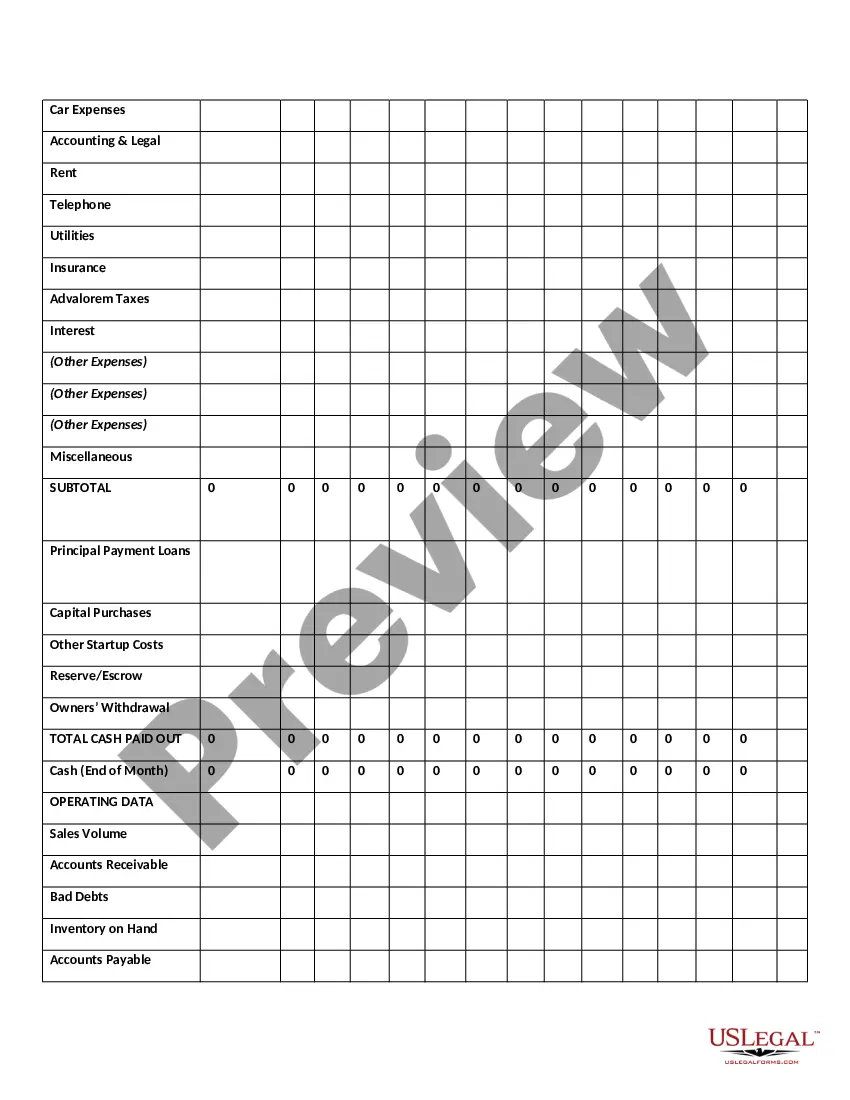

Mecklenburg North Carolina Twelve-Month Cash Flow is a financial statement that provides a detailed overview of the cash inflows and outflows for a period of twelve months in Mecklenburg County, North Carolina. This cash flow statement is crucial for individuals, businesses, and organizations to manage their finances effectively and make informed decisions. In this statement, various types of cash flow are categorized and described. Here are some key categories: 1. Operating Cash Flow: This category refers to the cash generated or used in day-to-day operations. It includes income from sales, payments received from customers, salaries, supplier payments, and other operating expenses. 2. Investment Cash Flow: Mecklenburg County may generate or use cash for investment purposes, such as buying or selling real estate, equipment, or investments. This category shows the cash inflows or outflows resulting from these investment activities. 3. Financing Cash Flow: Cash flows associated with borrowing, repaying loans, raising capital, issuing stocks, or paying dividends fall under financing cash flow. It provides insights into how Mecklenburg County manages its financial obligations and capital structure. 4. Non-operating Cash Flow: Mecklenburg County's cash flows that are not directly related to operating, investing, or financing activities are categorized as non-operating cash flows. These may include gains or losses from the sale of assets, interest income, or any other miscellaneous cash flows. 5. Net Cash Flow: This reflects the overall cash position of Mecklenburg County at the end of the twelve-month period. It is calculated by subtracting total cash outflows from total cash inflows across all categories. Mecklenburg North Carolina Twelve-Month Cash Flow statements are crucial tools for financial analysis, budgeting, and forecasting. They provide stakeholders with a comprehensive understanding of the county's cash flow situation, allowing them to assess its financial health, identify potential cash flow issues, and make strategic decisions accordingly. By regularly monitoring and analyzing the various components of the Mecklenburg Twelve-Month Cash Flow, both individuals and organizations can gain valuable insights into the fiscal stability and liquidity of Mecklenburg County in North Carolina.Mecklenburg North Carolina Twelve-Month Cash Flow is a financial statement that provides a detailed overview of the cash inflows and outflows for a period of twelve months in Mecklenburg County, North Carolina. This cash flow statement is crucial for individuals, businesses, and organizations to manage their finances effectively and make informed decisions. In this statement, various types of cash flow are categorized and described. Here are some key categories: 1. Operating Cash Flow: This category refers to the cash generated or used in day-to-day operations. It includes income from sales, payments received from customers, salaries, supplier payments, and other operating expenses. 2. Investment Cash Flow: Mecklenburg County may generate or use cash for investment purposes, such as buying or selling real estate, equipment, or investments. This category shows the cash inflows or outflows resulting from these investment activities. 3. Financing Cash Flow: Cash flows associated with borrowing, repaying loans, raising capital, issuing stocks, or paying dividends fall under financing cash flow. It provides insights into how Mecklenburg County manages its financial obligations and capital structure. 4. Non-operating Cash Flow: Mecklenburg County's cash flows that are not directly related to operating, investing, or financing activities are categorized as non-operating cash flows. These may include gains or losses from the sale of assets, interest income, or any other miscellaneous cash flows. 5. Net Cash Flow: This reflects the overall cash position of Mecklenburg County at the end of the twelve-month period. It is calculated by subtracting total cash outflows from total cash inflows across all categories. Mecklenburg North Carolina Twelve-Month Cash Flow statements are crucial tools for financial analysis, budgeting, and forecasting. They provide stakeholders with a comprehensive understanding of the county's cash flow situation, allowing them to assess its financial health, identify potential cash flow issues, and make strategic decisions accordingly. By regularly monitoring and analyzing the various components of the Mecklenburg Twelve-Month Cash Flow, both individuals and organizations can gain valuable insights into the fiscal stability and liquidity of Mecklenburg County in North Carolina.