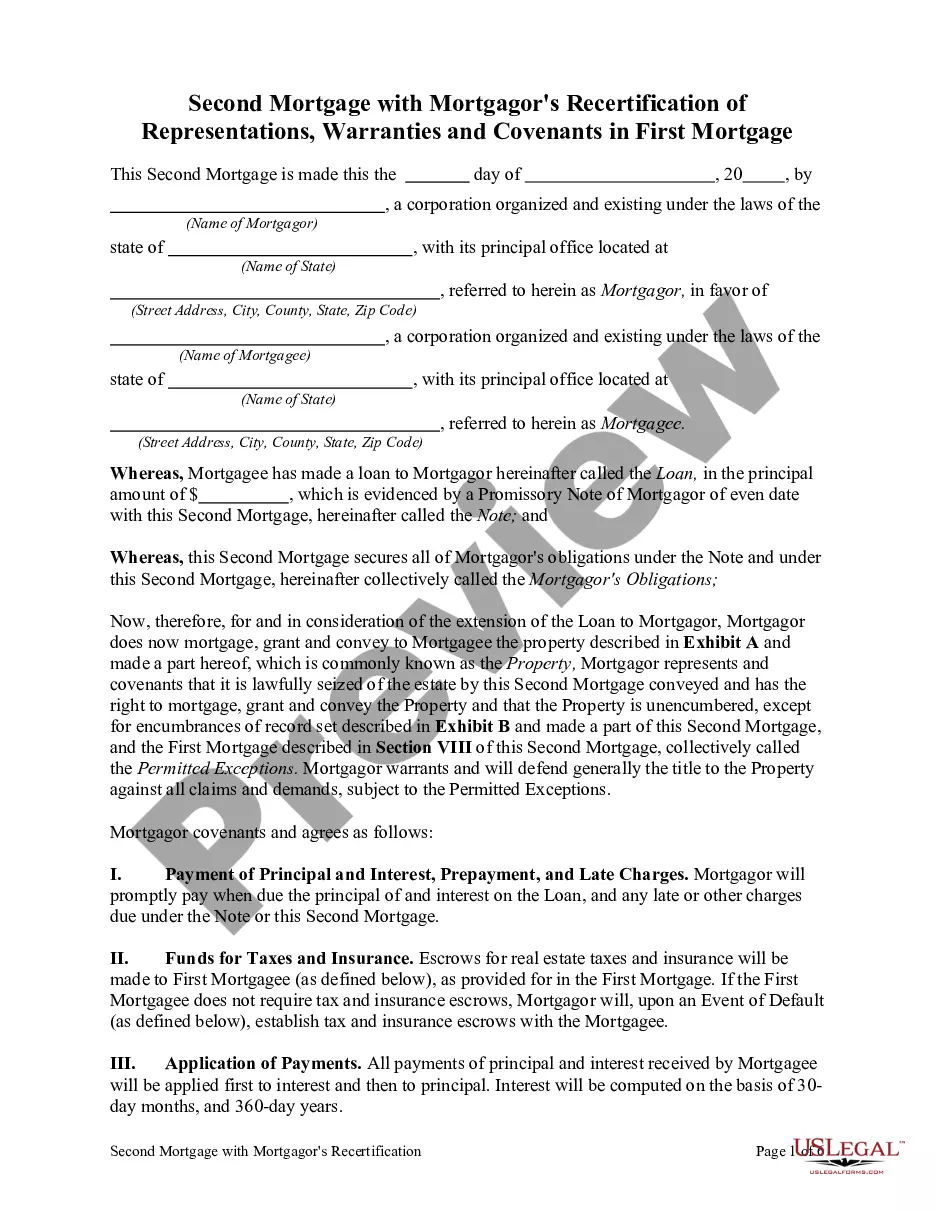

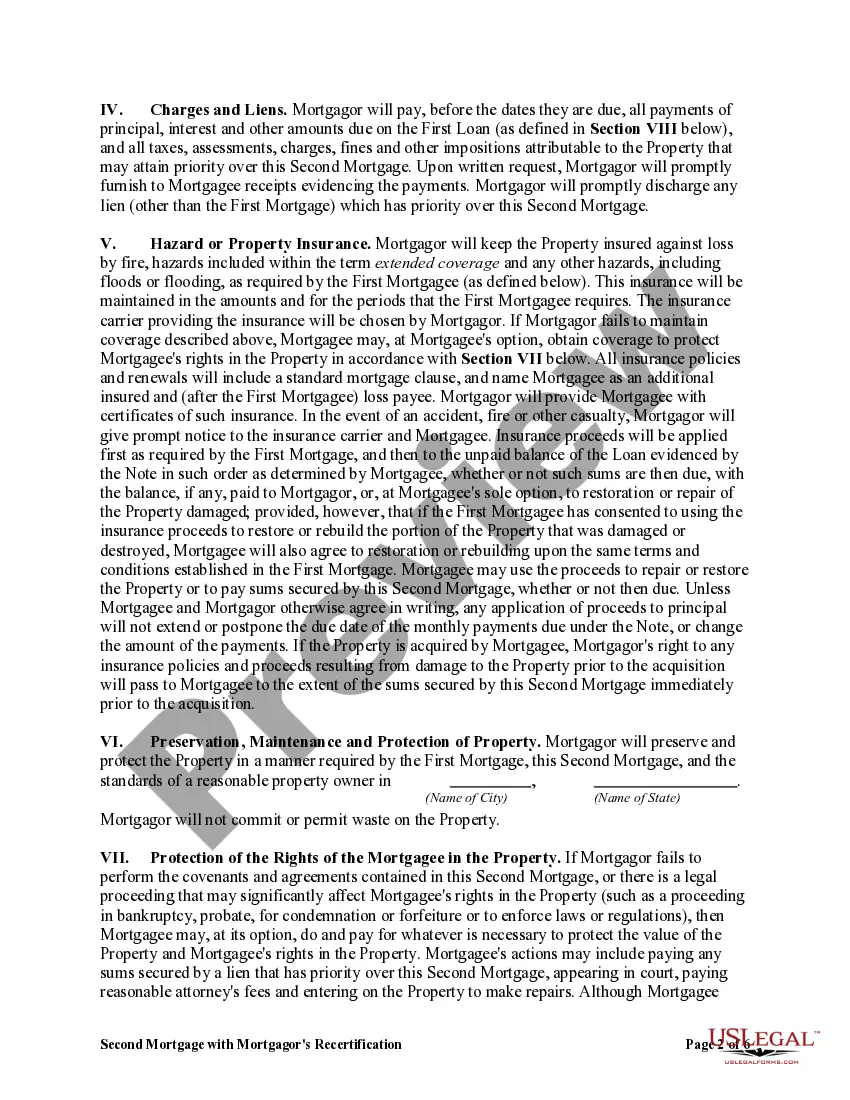

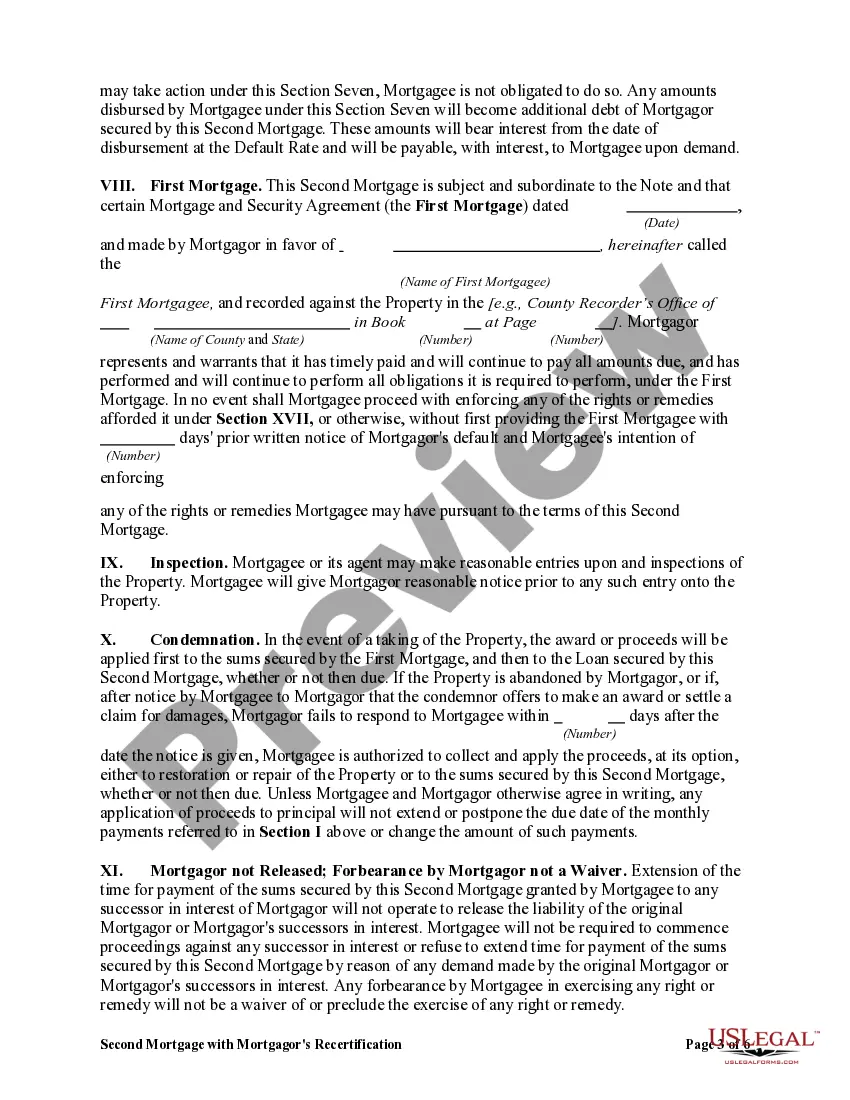

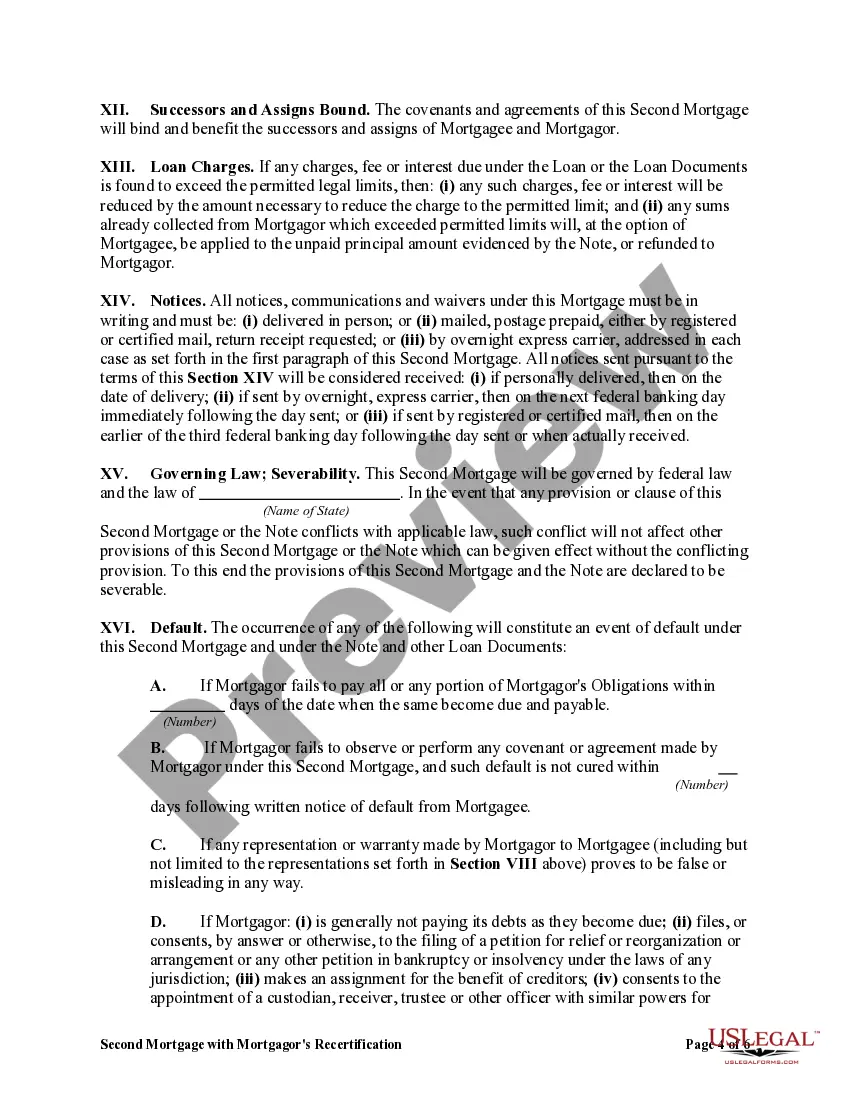

Hillsborough Florida Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage is a legally binding agreement that outlines the specific terms and conditions related to the mortgage agreement between a borrower (mortgagor) and a lender. It serves as an additional loan secured by the same property that had been pledged as collateral in the first mortgage. This type of second mortgage is commonly used by homeowners in Hillsborough, Florida, who require additional funds while retaining their existing first mortgage. By obtaining a second mortgage, borrowers can tap into the equity of their property, which is the difference between the property's value and the outstanding balance of the first mortgage. The Hillsborough Florida Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage requires the borrower to provide updated information and reaffirm certain representations, warranties, and covenants made in the original first mortgage agreement. The purpose of this recertification is to ensure that there have been no material changes in the borrower's financial situation, property condition, or any other relevant factors that could impact the lender's security interest in the property. It is important to note that there may be different variations or types of Hillsborough Florida Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage. These could include: 1. Fixed-Rate Second Mortgage: This type of second mortgage offers a fixed interest rate throughout the loan term, providing borrowers with stability and predictable monthly payments. 2. Adjustable-Rate Second Mortgage: With an adjustable-rate second mortgage, the interest rate is subject to periodic adjustments based on market conditions, potentially leading to changes in the monthly payment amount. 3. Home Equity Line of Credit (HELOT): A HELOT allows borrowers to access a line of credit with a predetermined limit, from which they can withdraw funds as needed. In this case, the second mortgage is in the form of a revolving credit line. Regardless of the specific type of second mortgage, it is crucial for the borrower to carefully review and understand the terms and conditions, including the recertification requirements. It is also advisable to consult with a qualified attorney or financial advisor to ensure compliance and make informed decisions regarding this financial arrangement.

Hillsborough Florida Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage

Description

How to fill out Hillsborough Florida Second Mortgage With Mortgagor's Recertification Of Representations, Warranties And Covenants In First Mortgage?

How much time does it typically take you to create a legal document? Considering that every state has its laws and regulations for every life sphere, locating a Hillsborough Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage suiting all regional requirements can be stressful, and ordering it from a professional lawyer is often costly. Many online services offer the most popular state-specific templates for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most comprehensive online collection of templates, collected by states and areas of use. Aside from the Hillsborough Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage, here you can find any specific form to run your business or personal affairs, complying with your regional requirements. Specialists verify all samples for their validity, so you can be certain to prepare your documentation correctly.

Using the service is fairly straightforward. If you already have an account on the platform and your subscription is valid, you only need to log in, pick the needed form, and download it. You can pick the file in your profile anytime later on. Otherwise, if you are new to the platform, there will be a few more actions to complete before you obtain your Hillsborough Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage:

- Check the content of the page you’re on.

- Read the description of the template or Preview it (if available).

- Search for another form utilizing the related option in the header.

- Click Buy Now when you’re certain in the selected file.

- Select the subscription plan that suits you most.

- Register for an account on the platform or log in to proceed to payment options.

- Make a payment via PalPal or with your credit card.

- Switch the file format if needed.

- Click Download to save the Hillsborough Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage.

- Print the sample or use any preferred online editor to fill it out electronically.

No matter how many times you need to use the purchased template, you can locate all the samples you’ve ever downloaded in your profile by opening the My Forms tab. Give it a try!