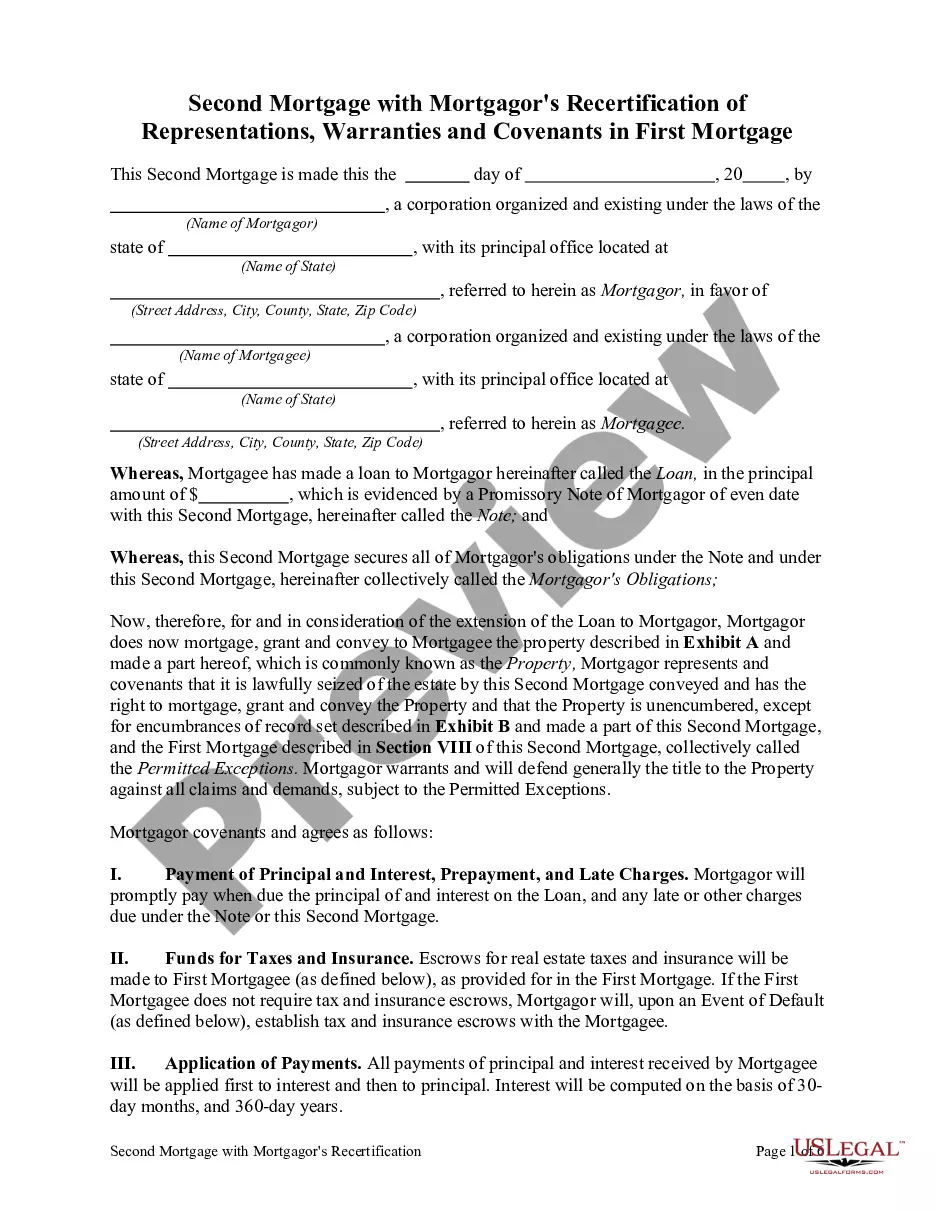

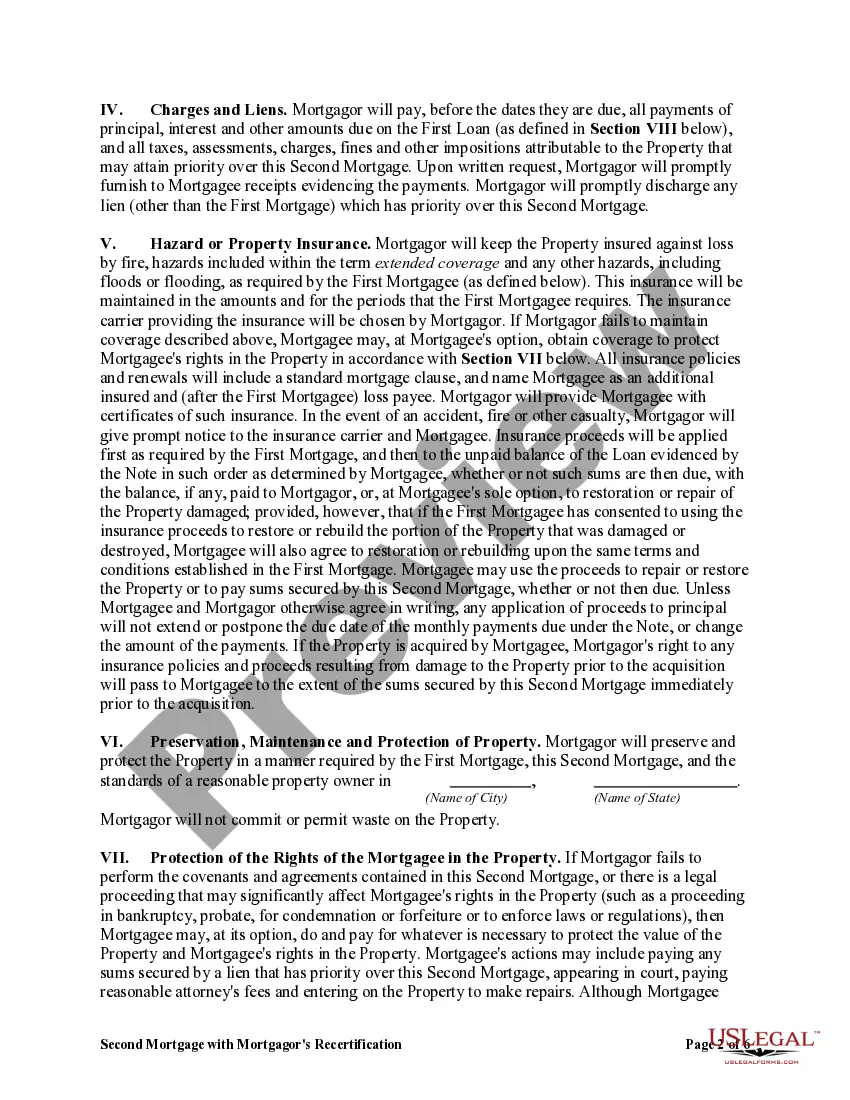

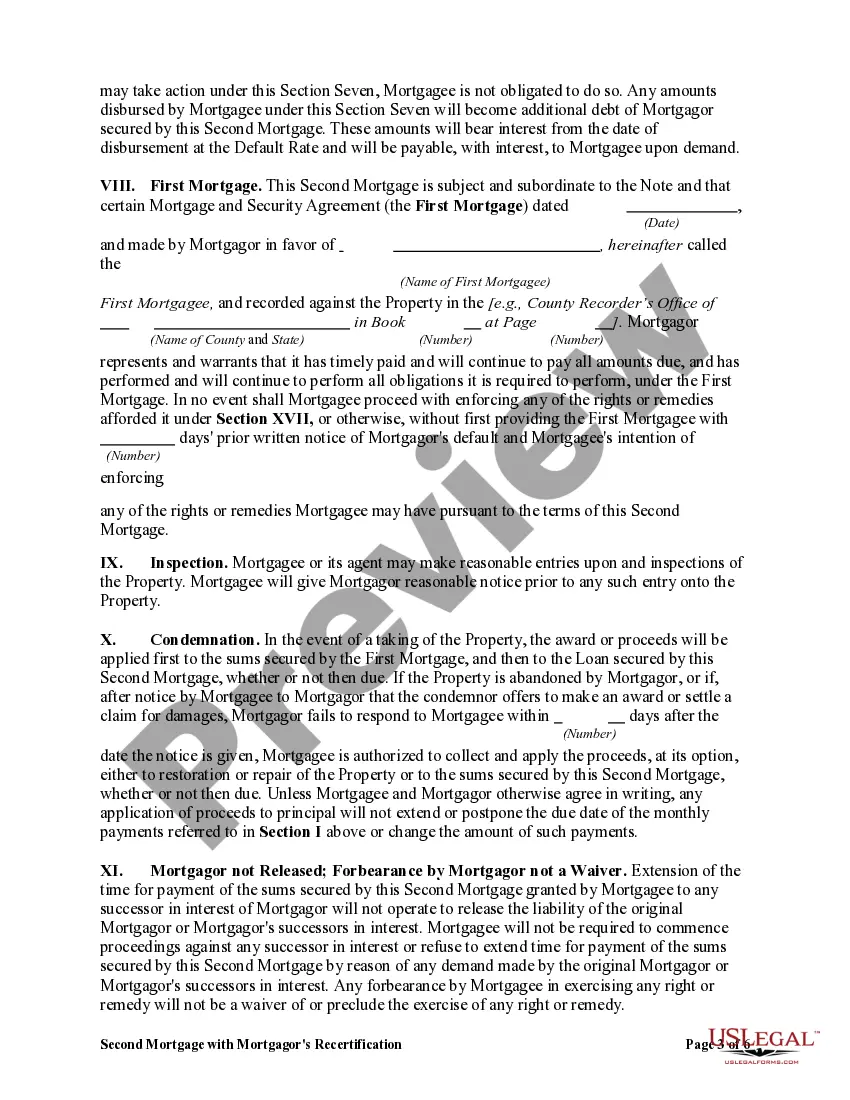

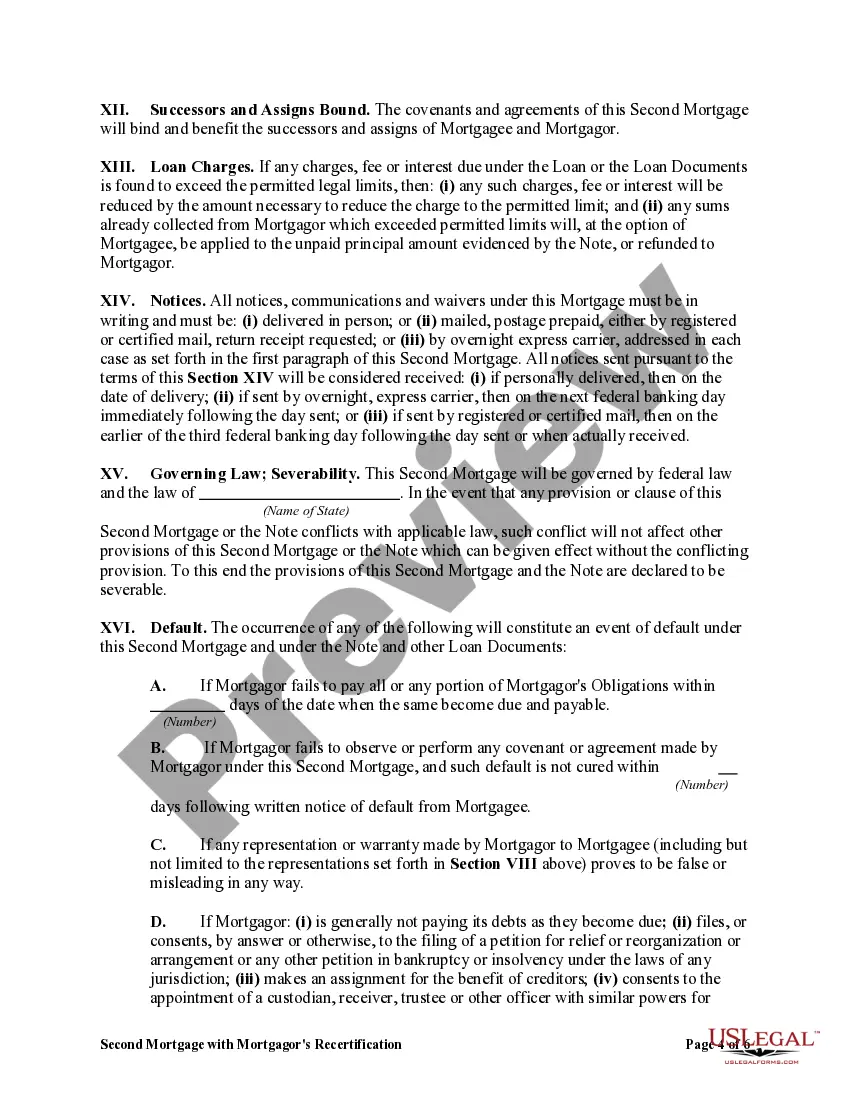

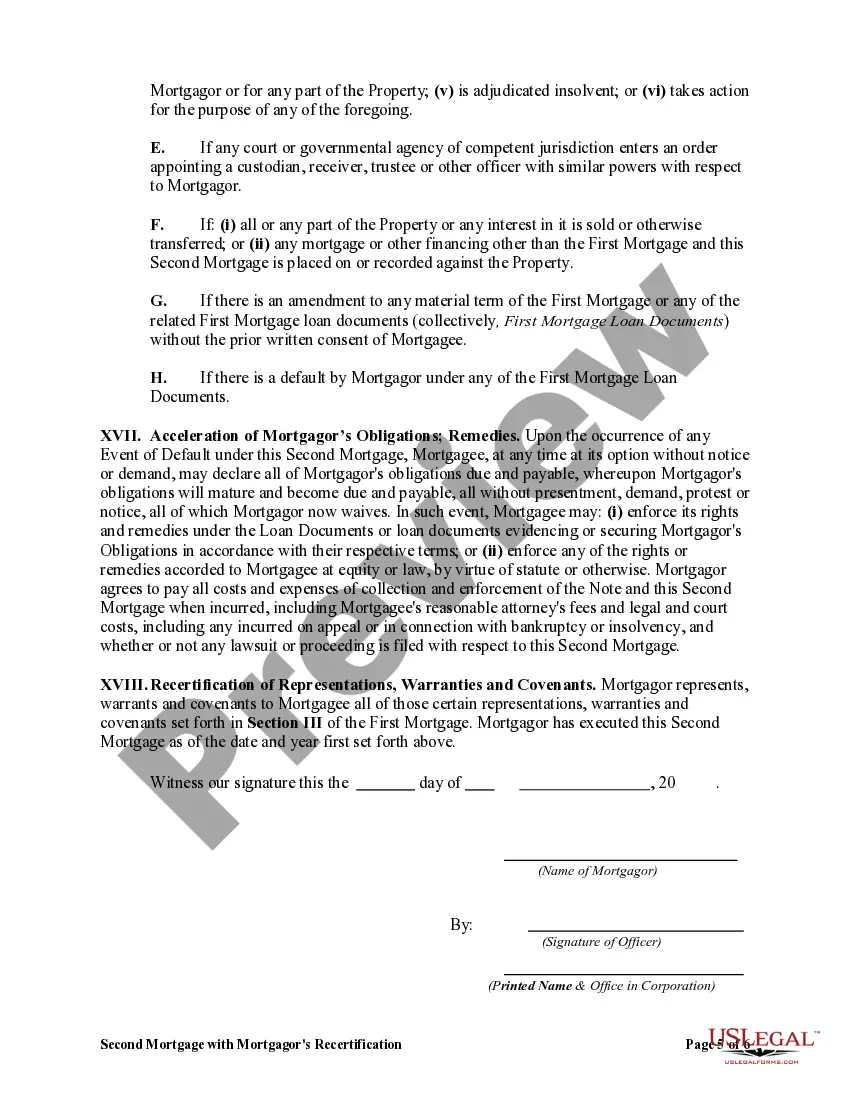

A Salt Lake Utah Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage is a specific type of mortgage agreement that involves the use of a second lien on a property located in Salt Lake City, Utah. This second mortgage is taken out after an initial first mortgage has already been established. The purpose of the second mortgage is to secure additional financing for the property owner. It can be obtained for various reasons, such as funding home improvements, consolidating debts, or covering other financial needs. However, it is important to note that this type of mortgage places the second lien holder in a subordinate position to the first mortgage lender, meaning that in the event of default, the first mortgage lender will have priority over the proceeds from the sale of the property. One crucial aspect of the Salt Lake Utah Second Mortgage with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage is the requirement for the mortgagor to recertify certain representations, warranties, and covenants made in the first mortgage agreement. This ensures that the borrower continues to affirm the accuracy and validity of the information provided during the initial mortgage process. These recertifications may include confirming the absence of any undisclosed liens or encumbrances on the property, maintaining adequate insurance coverage, and upholding the property's value. It is important to differentiate between the various types of Salt Lake Utah Second Mortgages with Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage. Some common types include: 1. Home Equity Line of Credit (HELOT): This type of second mortgage allows the borrower to access funds as needed, similar to a credit card. The borrower is given a predetermined credit limit and can withdraw funds up to that limit during the specified draw period. 2. Fixed-Rate Second Mortgage: This type of second mortgage provides the borrower with a lump sum of money upfront, which is repaid through regular monthly installments over a fixed term, often with a fixed interest rate. 3. Adjustable-Rate Second Mortgage: Unlike a fixed-rate second mortgage, the interest rate on this type of mortgage can fluctuate over time. The initial interest rate is typically lower than a fixed-rate mortgage but may change periodically according to an index, potentially resulting in higher or lower monthly payments. 4. Combination Second Mortgage: This involves obtaining both a fixed-rate and a variable-rate second mortgage simultaneously. The borrower receives a lump sum from the fixed-rate portion and a line of credit from the variable-rate portion. By providing Mortgagor's Recertification of Representations, Warranties, and Covenants in First Mortgage, lenders can ensure that the borrower remains compliant with the terms of the mortgage and maintain confidence in the accuracy of the information provided. This further protects the interests of both lenders and borrowers in Salt Lake City, Utah.

Salt Lake Utah Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage

Description

How to fill out Salt Lake Utah Second Mortgage With Mortgagor's Recertification Of Representations, Warranties And Covenants In First Mortgage?

Whether you plan to open your company, enter into a deal, apply for your ID renewal, or resolve family-related legal issues, you need to prepare specific paperwork meeting your local laws and regulations. Locating the right papers may take a lot of time and effort unless you use the US Legal Forms library.

The platform provides users with more than 85,000 professionally drafted and verified legal documents for any personal or business case. All files are grouped by state and area of use, so picking a copy like Salt Lake Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage is quick and straightforward.

The US Legal Forms website users only need to log in to their account and click the Download button next to the required template. If you are new to the service, it will take you a couple of more steps to get the Salt Lake Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage. Follow the guidelines below:

- Make sure the sample meets your personal needs and state law regulations.

- Read the form description and check the Preview if there’s one on the page.

- Use the search tab specifying your state above to locate another template.

- Click Buy Now to obtain the sample when you find the proper one.

- Opt for the subscription plan that suits you most to continue.

- Log in to your account and pay the service with a credit card or PayPal.

- Download the Salt Lake Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage in the file format you prefer.

- Print the copy or complete it and sign it electronically via an online editor to save time.

Documents provided by our website are multi-usable. Having an active subscription, you can access all of your previously purchased paperwork at any moment in the My Forms tab of your profile. Stop wasting time on a constant search for up-to-date official documents. Join the US Legal Forms platform and keep your paperwork in order with the most comprehensive online form collection!