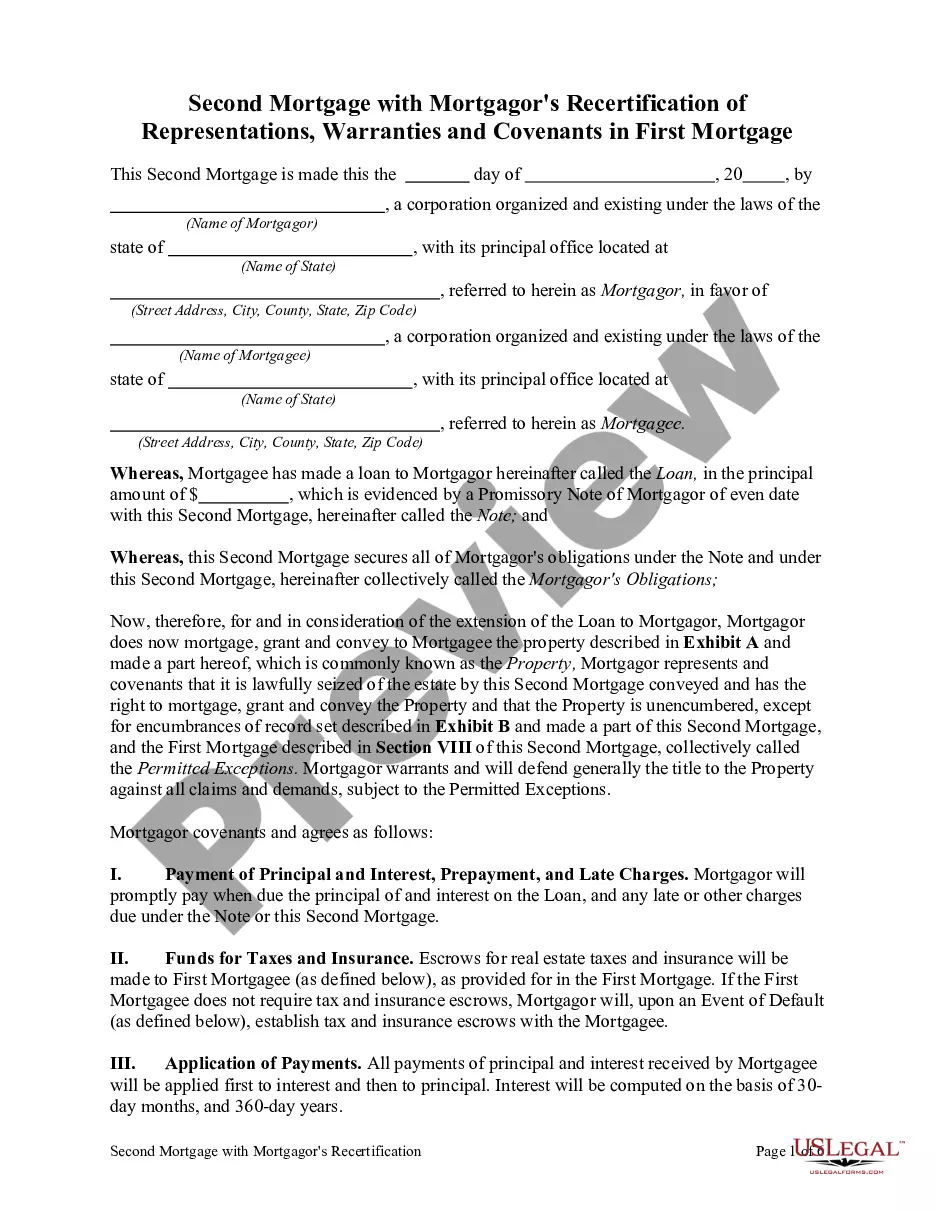

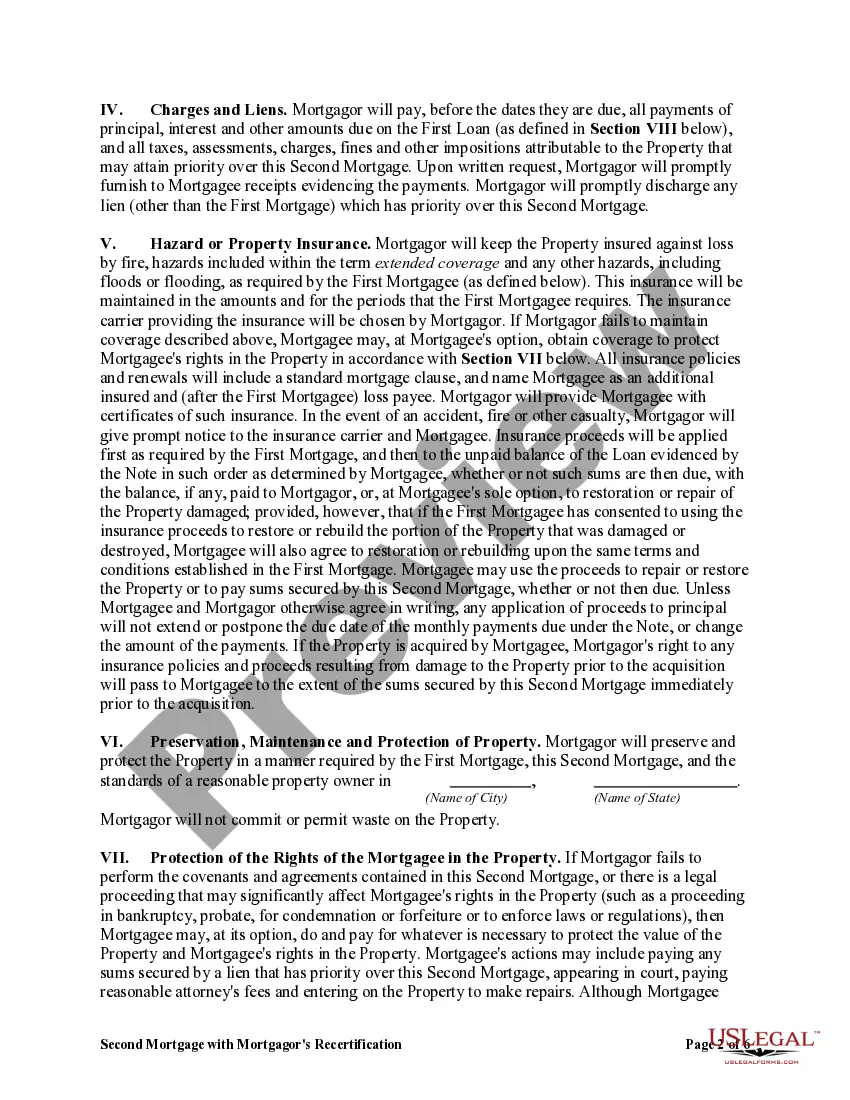

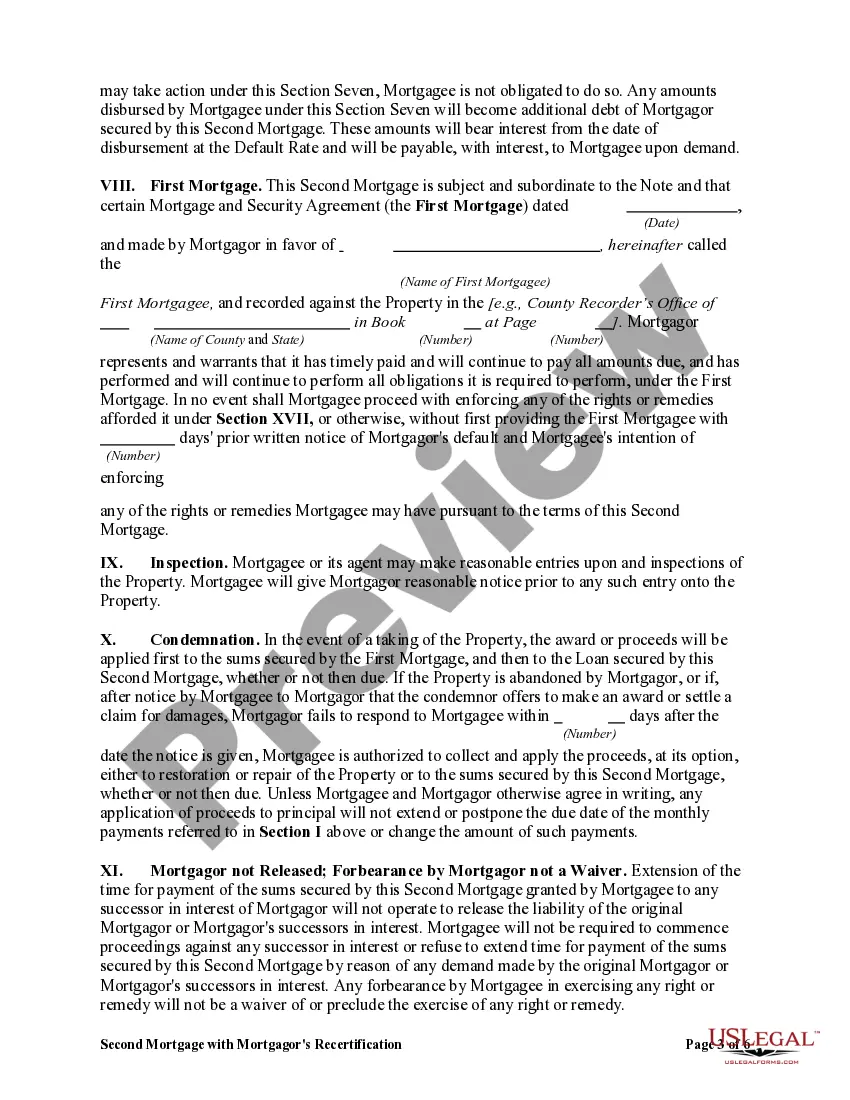

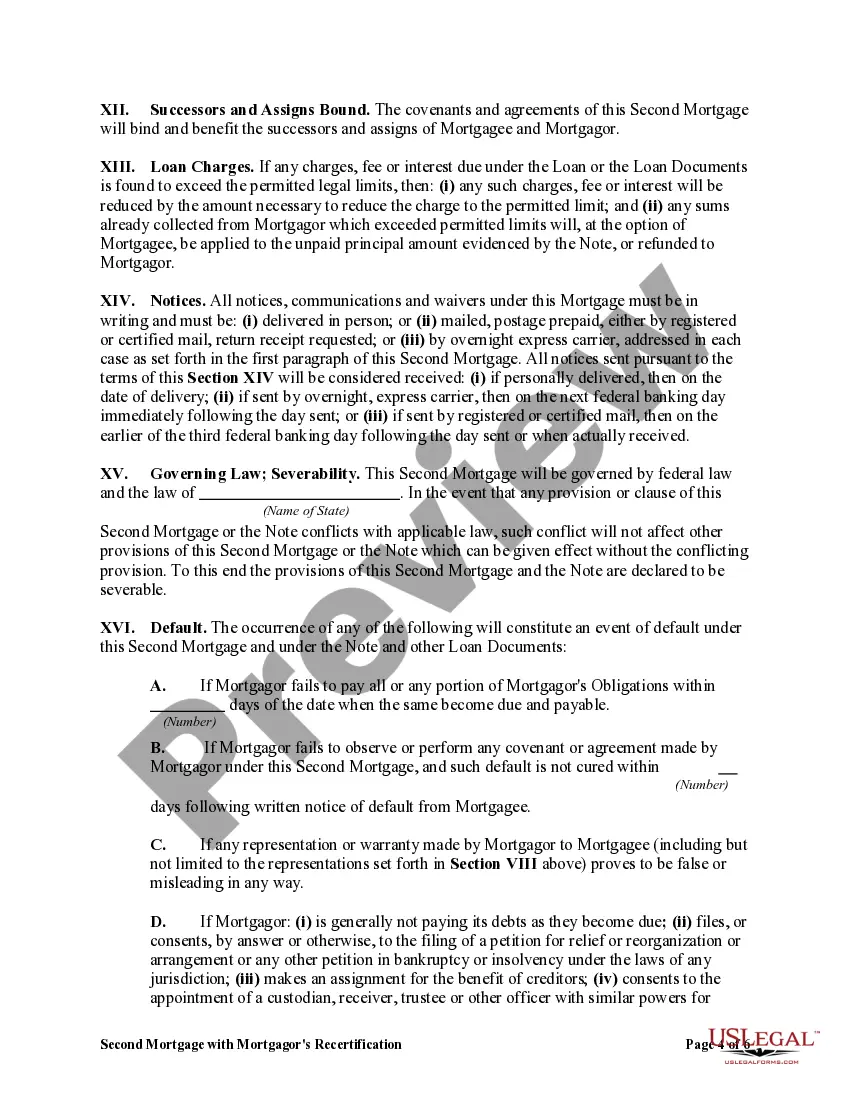

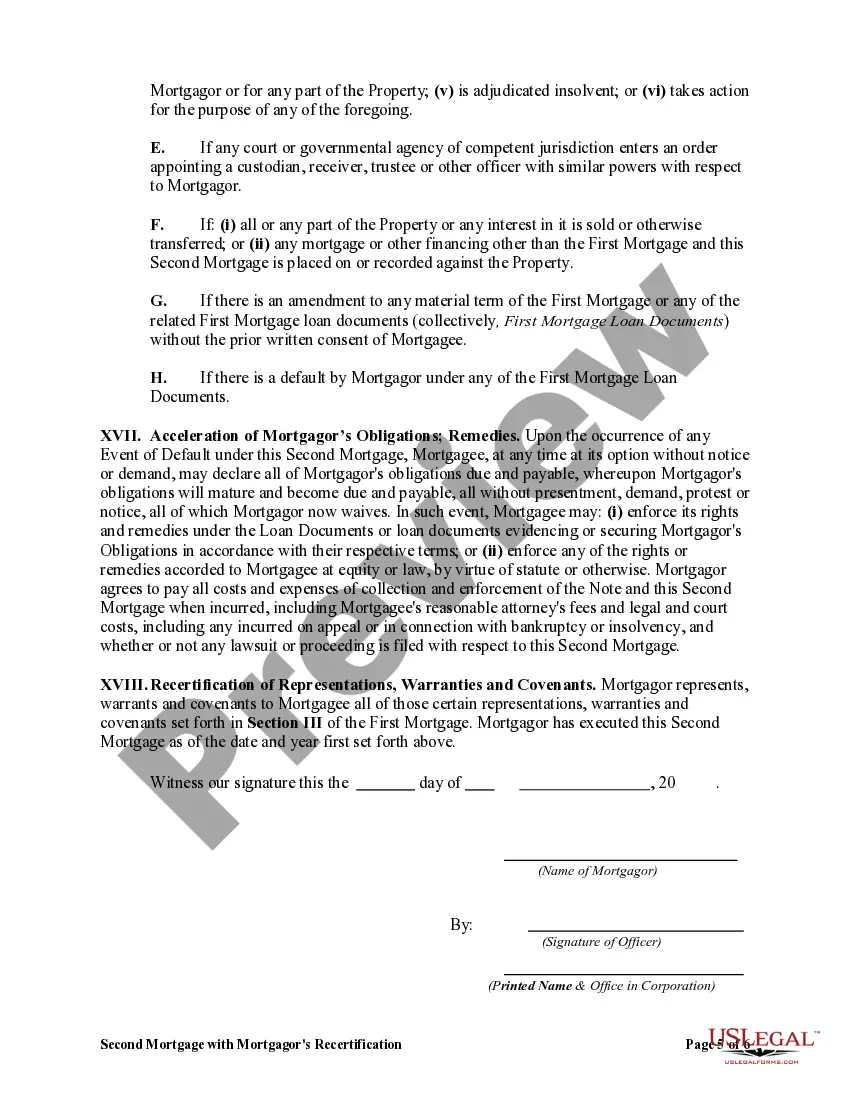

Wake North Carolina Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage is a type of loan for homeowners in Wake County, North Carolina who already have an existing mortgage on their property. This second mortgage is typically used for various purposes such as home renovations, debt consolidation, or to cover unexpected expenses. The main feature of this type of mortgage is the requirement for the mortgagor (borrower) to recertify the representations, warranties, and covenants made in their first mortgage agreement. This means that the borrower must reaffirm that all the information provided in the initial mortgage application is still accurate and that there have been no significant changes in their financial or personal situation since obtaining the first mortgage. The recertification process involves providing updated financial documents, such as income statements, tax returns, and credit reports. The lender will carefully evaluate these documents to ensure the borrower's continued eligibility for a second mortgage. By recertifying their representations, warranties, and covenants, the borrower demonstrates their commitment to maintaining the terms and conditions of their original mortgage agreement. This reassures the lender that the borrower's financial situation has not significantly deteriorated, reducing the risk associated with approving the second mortgage. There can be different types of Wake North Carolina Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage depending on the specific terms and conditions set by the lender. Some of these variations may include: 1. Fixed-Rate Second Mortgage: This type of second mortgage offers a fixed interest rate throughout the loan term, providing predictability and stability in monthly payments. 2. Adjustable-Rate Second Mortgage: In this case, the interest rate on the second mortgage can fluctuate based on market conditions. This type of mortgage may be suitable for borrowers who anticipate paying off the loan within a shorter period. 3. Home Equity Line of Credit (HELOT): A HELOT is a revolving line of credit secured by the equity in the borrower's home. It allows the borrower to withdraw funds as needed, up to a predetermined credit limit. 4. Cash-Out Refinance: This option involves refinancing the existing mortgage and obtaining a larger loan amount than the current outstanding balance. The borrower can then receive the difference in cash, which can be used for various purposes. It is essential for prospective borrowers to carefully consider their financial situation and evaluate the terms and conditions of each type of second mortgage before making a decision. Consulting with a mortgage professional or financial advisor can provide valuable guidance in selecting the most appropriate option.

Wake North Carolina Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage

Description

How to fill out Wake North Carolina Second Mortgage With Mortgagor's Recertification Of Representations, Warranties And Covenants In First Mortgage?

How much time does it normally take you to draw up a legal document? Given that every state has its laws and regulations for every life sphere, finding a Wake Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage meeting all local requirements can be exhausting, and ordering it from a professional attorney is often expensive. Many online services offer the most common state-specific documents for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most extensive online collection of templates, gathered by states and areas of use. Apart from the Wake Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage, here you can get any specific document to run your business or personal deeds, complying with your county requirements. Experts check all samples for their actuality, so you can be sure to prepare your paperwork properly.

Using the service is remarkably easy. If you already have an account on the platform and your subscription is valid, you only need to log in, opt for the needed sample, and download it. You can get the file in your profile at any moment later on. Otherwise, if you are new to the website, there will be some extra steps to complete before you obtain your Wake Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage:

- Examine the content of the page you’re on.

- Read the description of the sample or Preview it (if available).

- Look for another document using the related option in the header.

- Click Buy Now once you’re certain in the selected file.

- Decide on the subscription plan that suits you most.

- Sign up for an account on the platform or log in to proceed to payment options.

- Make a payment via PalPal or with your credit card.

- Change the file format if needed.

- Click Download to save the Wake Second Mortgage with Mortgagor's Recertification of Representations, Warranties and Covenants in First Mortgage.

- Print the sample or use any preferred online editor to fill it out electronically.

No matter how many times you need to use the purchased document, you can locate all the files you’ve ever downloaded in your profile by opening the My Forms tab. Try it out!