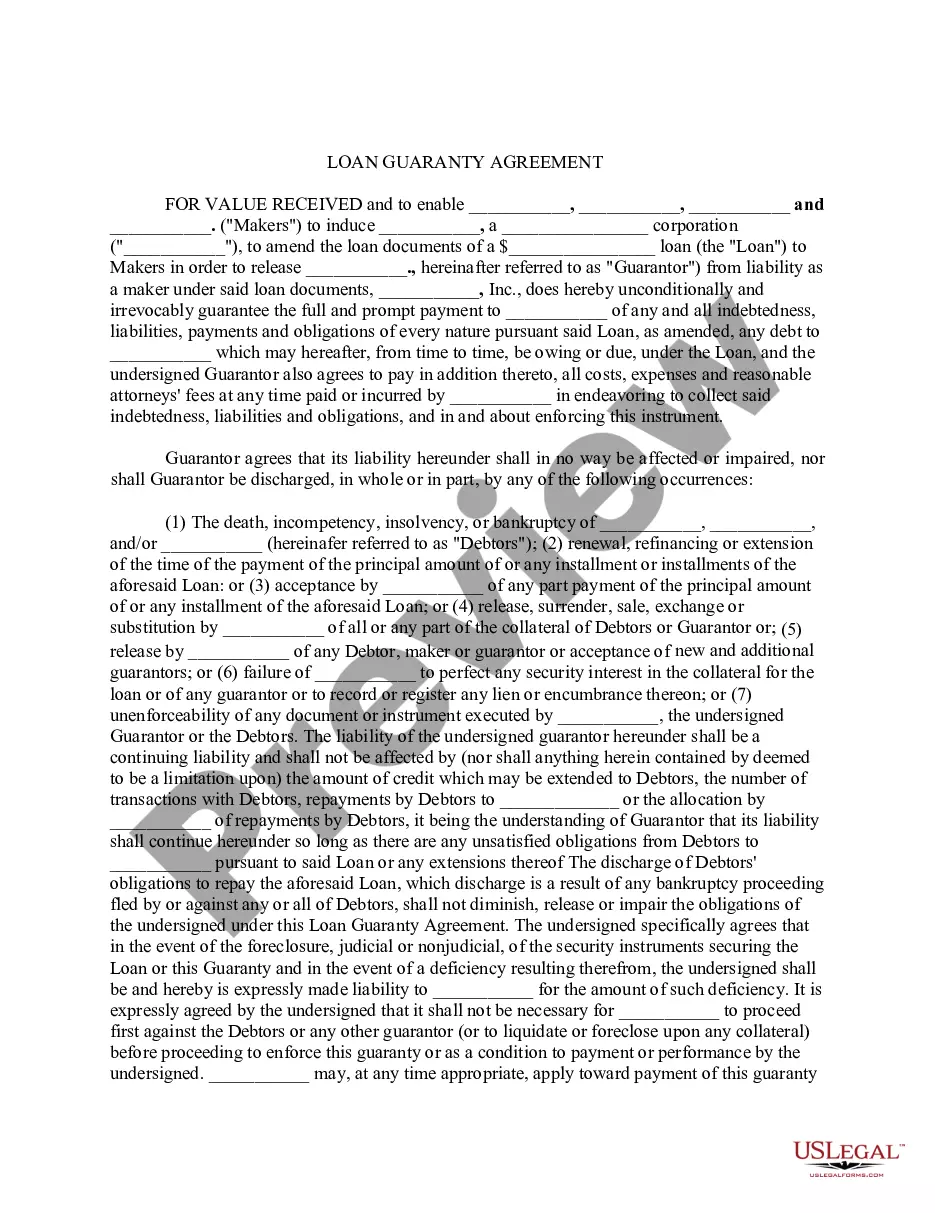

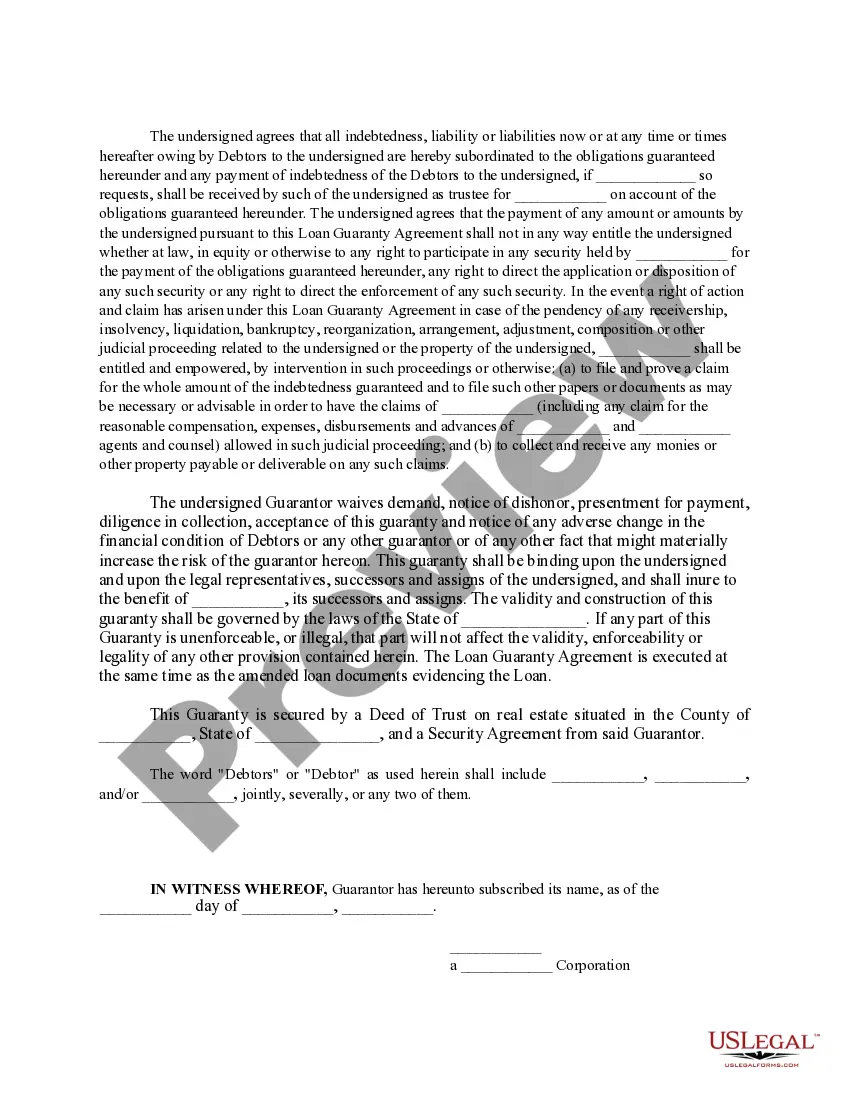

Contra Costa California Loan Guaranty Agreement is a legally binding contract entered into between a lender and a borrower in Contra Costa County, California. This agreement provides a guarantee or assurance to the lender that if the borrower fails to repay the loan, a third party (guarantor) will step in and fulfill the borrower's obligations. The purpose of the Contra Costa California Loan Guaranty Agreement is to minimize the risk for the lender by ensuring that the borrowed funds will be repaid in accordance with the terms and conditions outlined in the loan agreement. The guarantor agrees to repay the outstanding loan amount, including any interest and fees, in case the borrower defaults. This agreement serves as a form of security for lenders, enabling them to provide loans to borrowers who might not otherwise meet their stringent lending criteria. It enhances the borrower's creditworthiness by having a third-party guarantor who takes on the responsibility of repayment if the borrower faces financial difficulties. The Contra Costa California Loan Guaranty Agreement typically specifies the following key elements: 1. Parties involved: It identifies the lender, borrower, and guarantor. It mentions their legal names, addresses, and contact details. 2. Loan details: It outlines the loan amount, the purpose of the loan, interest rate, repayment terms, and any additional fees or charges. 3. Guarantor's obligations: It clearly defines the guarantor's responsibilities, stating that they will fulfill the borrower's obligations if the borrower fails to repay the loan. 4. Default provisions: It describes the conditions under which the loan is considered in default and the procedures to be followed in such situations. 5. Termination: It specifies the circumstances under which the guarantor's obligations will be terminated, for example, upon full repayment or upon mutual agreement. Types of Contra Costa California Loan Guaranty Agreements may include: 1. Personal Guaranty: This type of agreement involves an individual or individuals personally guaranteeing the loan repayment on behalf of the borrower. 2. Corporate Guaranty: In cases where the borrower is a corporation or business entity, another corporation or business entity acts as the guarantor, assuming responsibility for the loan. 3. Limited Guaranty: This type of agreement limits the guarantor's liability to a portion or specific amount of the loan, providing a level of protection for the guarantor. In conclusion, the Contra Costa California Loan Guaranty Agreement is a crucial legal instrument that provides lenders with an additional layer of security and ensures borrowers' access to financing. It outlines the obligations and responsibilities of the guarantor while offering protection to the lender in case of default.

Contra Costa California Loan Guaranty Agreement

Description

How to fill out Contra Costa California Loan Guaranty Agreement?

Preparing legal paperwork can be burdensome. Besides, if you decide to ask a lawyer to draft a commercial contract, documents for proprietorship transfer, pre-marital agreement, divorce papers, or the Contra Costa Loan Guaranty Agreement, it may cost you a fortune. So what is the best way to save time and money and draft legitimate documents in total compliance with your state and local laws and regulations? US Legal Forms is an excellent solution, whether you're searching for templates for your personal or business needs.

US Legal Forms is the most extensive online catalog of state-specific legal documents, providing users with the up-to-date and professionally verified templates for any scenario accumulated all in one place. Therefore, if you need the latest version of the Contra Costa Loan Guaranty Agreement, you can easily find it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample using the Download button. If you haven't subscribed yet, here's how you can get the Contra Costa Loan Guaranty Agreement:

- Look through the page and verify there is a sample for your region.

- Check the form description and use the Preview option, if available, to ensure it's the sample you need.

- Don't worry if the form doesn't satisfy your requirements - look for the right one in the header.

- Click Buy Now when you find the needed sample and select the best suitable subscription.

- Log in or register for an account to purchase your subscription.

- Make a transaction with a credit card or through PayPal.

- Opt for the file format for your Contra Costa Loan Guaranty Agreement and save it.

Once done, you can print it out and complete it on paper or upload the samples to an online editor for a faster and more convenient fill-out. US Legal Forms allows you to use all the documents ever acquired multiple times - you can find your templates in the My Forms tab in your profile. Give it a try now!