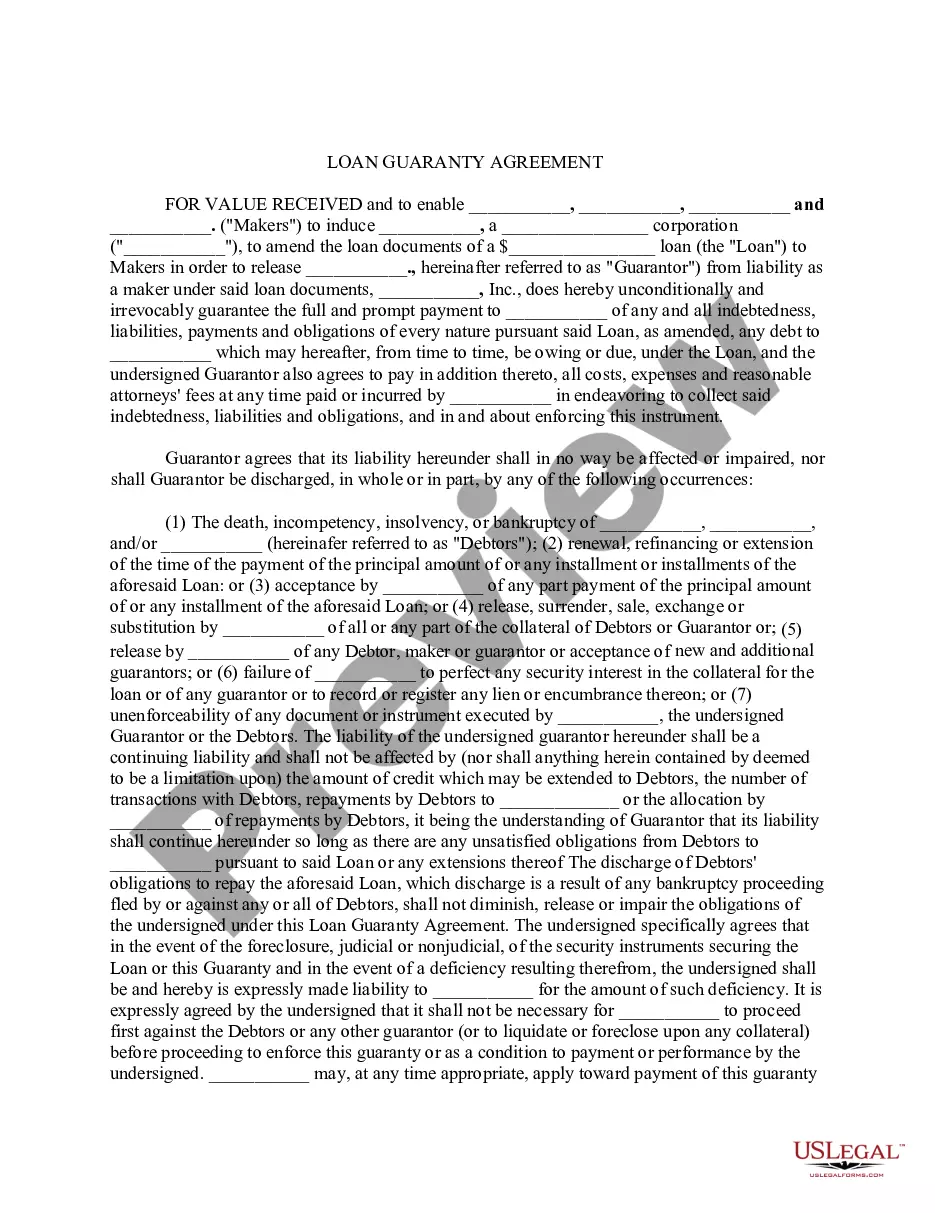

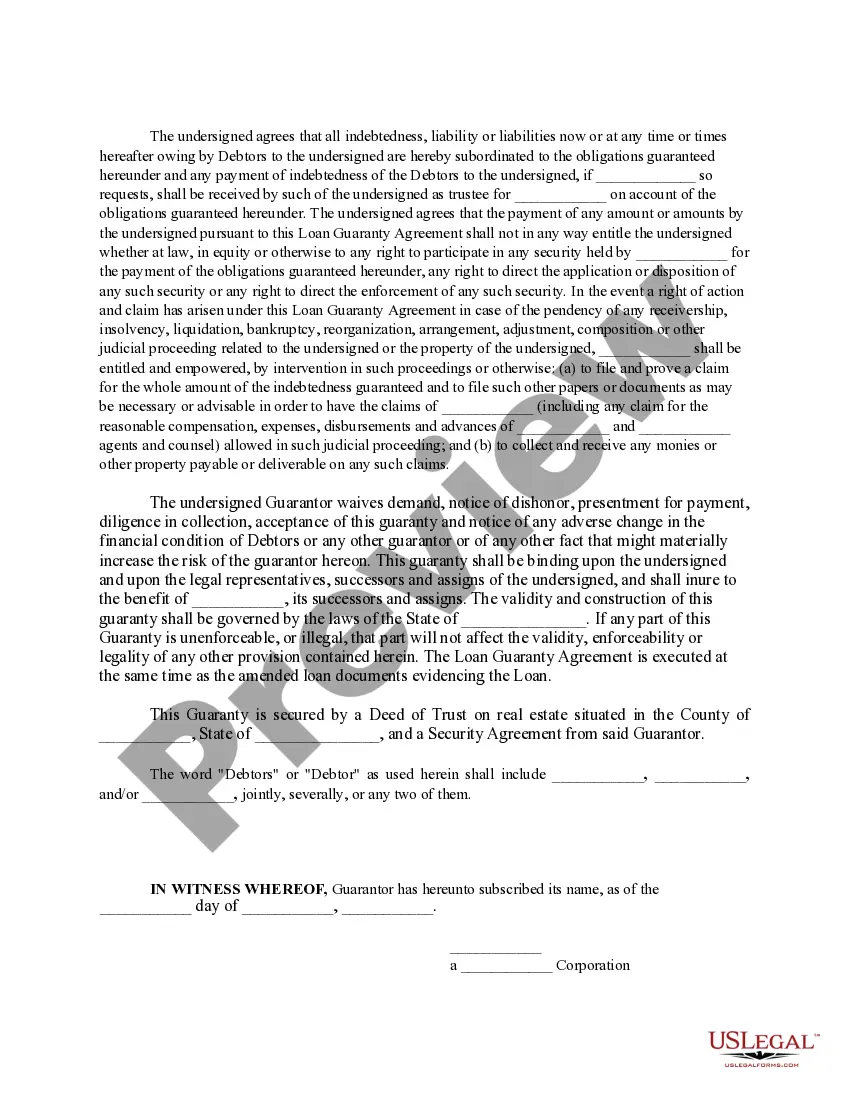

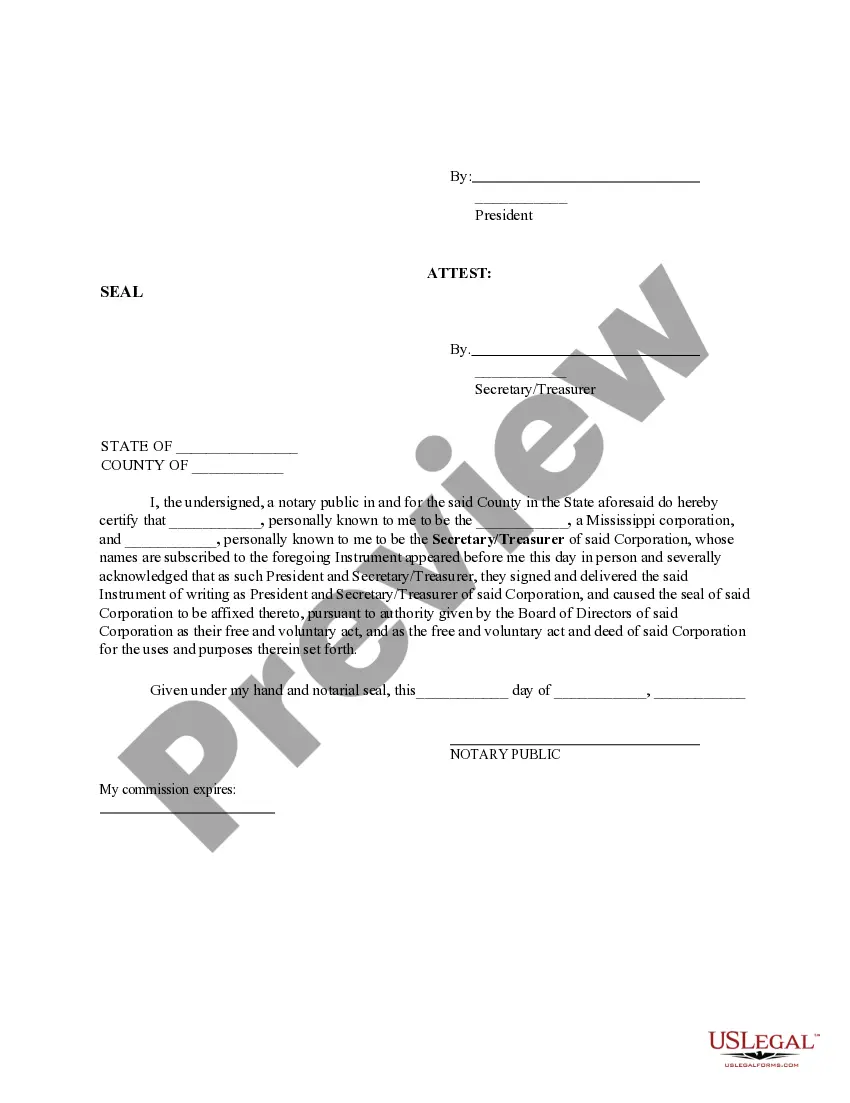

Nassau New York Loan Guaranty Agreement is a legally binding document that protects lenders from potential default by borrowers. It is a financial instrument designed to provide an added layer of security for lenders when issuing loans in Nassau County, New York. This agreement outlines the terms and conditions under which a guarantor agrees to be held liable for the loan in case the borrower fails to repay the debt. Nassau New York Loan Guaranty Agreements are typically utilized in various lending scenarios, including personal loans, business loans, mortgage loans, and commercial loans. These agreements provide lenders with financial assurance and minimize the risk associated with lending in Nassau County, New York. A Nassau New York Loan Guaranty Agreement typically includes essential details such as the names and contact information of the guarantor and borrower, the loan amount, interest rate, repayment terms, and any additional provisions or conditions. It also outlines the extent of the guarantor's liability, including whether it covers partial or full repayment of the loan. Additionally, the agreement may specify the circumstances under which the guarantor's obligation will be triggered, such as the borrower's default or bankruptcy. In Nassau County, New York, different types of Loan Guaranty Agreements may exist to cater to specific lending requirements. These may include: 1. Personal Loan Guaranty Agreement: This agreement occurs when an individual acts as the guarantor for a personal loan, ensuring the lender's protection if the borrower defaults. 2. Business Loan Guaranty Agreement: In this case, a business owner or partner guarantees repayment of a loan obtained for business purposes, reducing the lender's risk. 3. Mortgage Loan Guaranty Agreement: When someone acts as a guarantor for a mortgage loan, they assure the lender that the mortgage will be repaid, even if the borrower defaults. 4. Commercial Loan Guaranty Agreement: This agreement applies to loans taken by businesses for commercial purposes and involves a guarantor who promises to repay the loan if the borrower cannot. 5. Secondary Loan Guaranty Agreement: This type of agreement occurs when a guarantor supports a secondary loan or acts as a backup should the primary borrower default. Nassau New York Loan Guaranty Agreements play a crucial role in facilitating lending activities in Nassau County. Lenders are more likely to provide loans with the assurance of a guarantor, knowing they have recourse in case of non-payment. Borrowers, on the other hand, may benefit from lower interest rates or higher borrowing limits by having a guarantor with a strong credit history.

Nassau New York Loan Guaranty Agreement

Description

How to fill out Nassau New York Loan Guaranty Agreement?

Draftwing forms, like Nassau Loan Guaranty Agreement, to take care of your legal matters is a difficult and time-consumming task. Many situations require an attorney’s involvement, which also makes this task expensive. However, you can get your legal issues into your own hands and take care of them yourself. US Legal Forms is here to the rescue. Our website comes with over 85,000 legal documents crafted for different cases and life situations. We make sure each form is compliant with the laws of each state, so you don’t have to worry about potential legal issues compliance-wise.

If you're already familiar with our services and have a subscription with US, you know how easy it is to get the Nassau Loan Guaranty Agreement template. Go ahead and log in to your account, download the form, and personalize it to your requirements. Have you lost your form? No worries. You can get it in the My Forms tab in your account - on desktop or mobile.

The onboarding flow of new users is just as straightforward! Here’s what you need to do before getting Nassau Loan Guaranty Agreement:

- Make sure that your form is compliant with your state/county since the rules for creating legal paperwork may vary from one state another.

- Discover more information about the form by previewing it or reading a brief description. If the Nassau Loan Guaranty Agreement isn’t something you were looking for, then use the header to find another one.

- Sign in or register an account to begin using our service and get the document.

- Everything looks good on your end? Click the Buy now button and select the subscription plan.

- Select the payment gateway and type in your payment details.

- Your template is all set. You can try and download it.

It’s an easy task to find and purchase the appropriate document with US Legal Forms. Thousands of businesses and individuals are already benefiting from our extensive library. Sign up for it now if you want to check what other perks you can get with US Legal Forms!