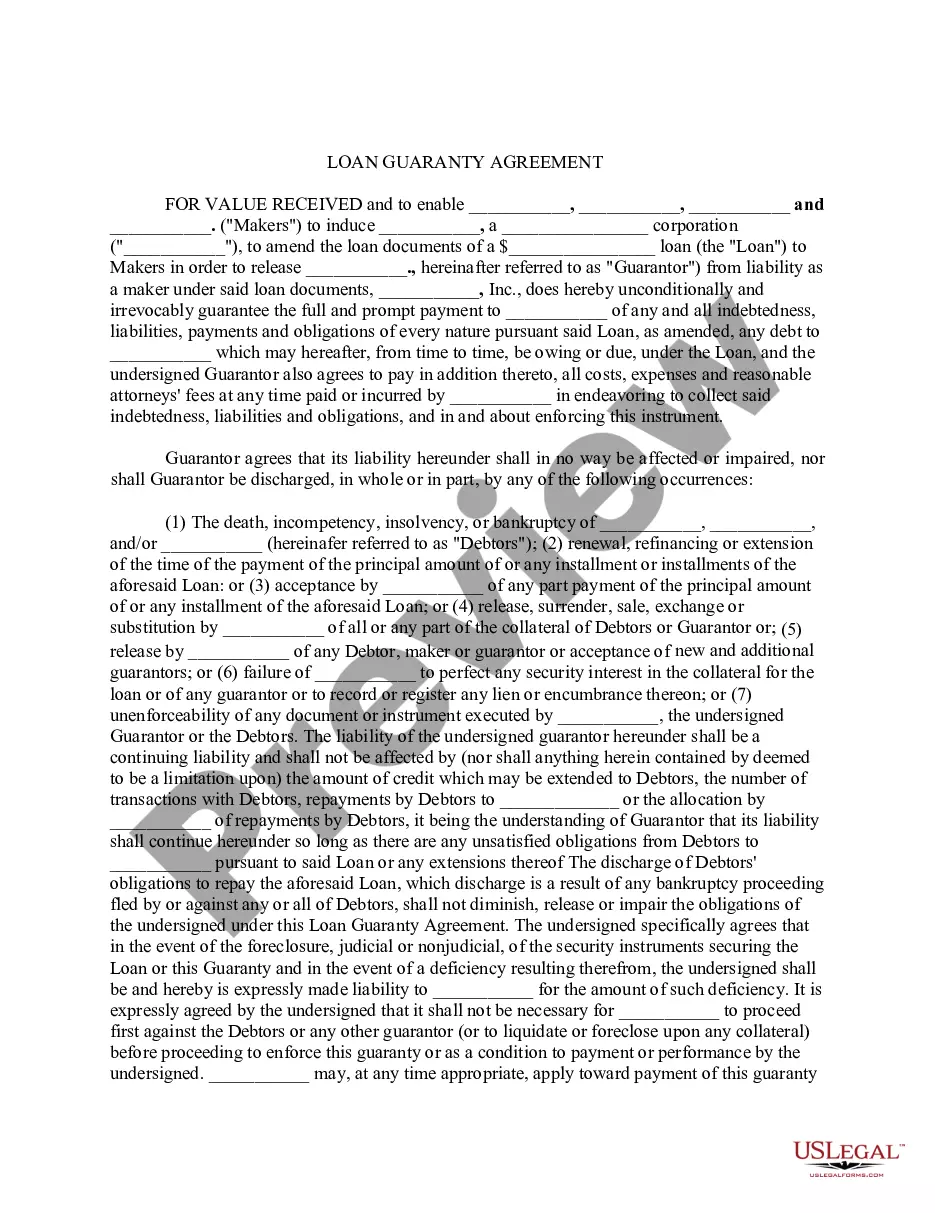

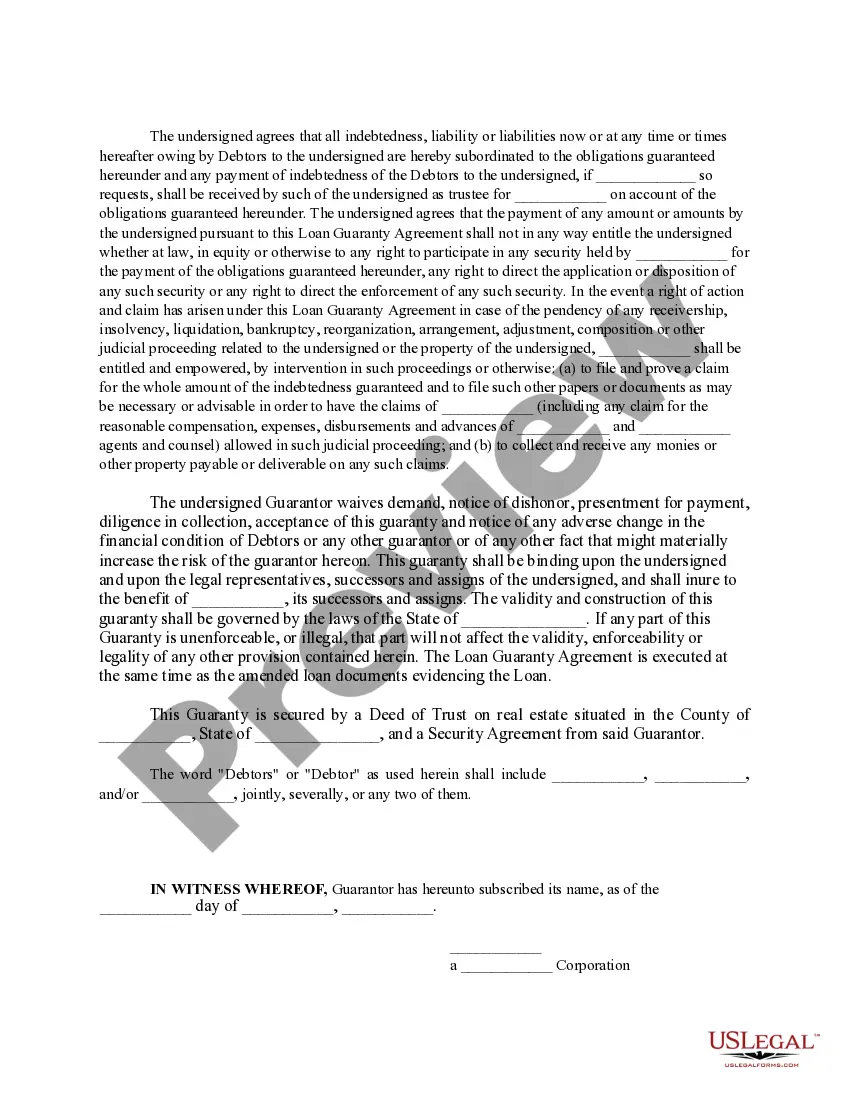

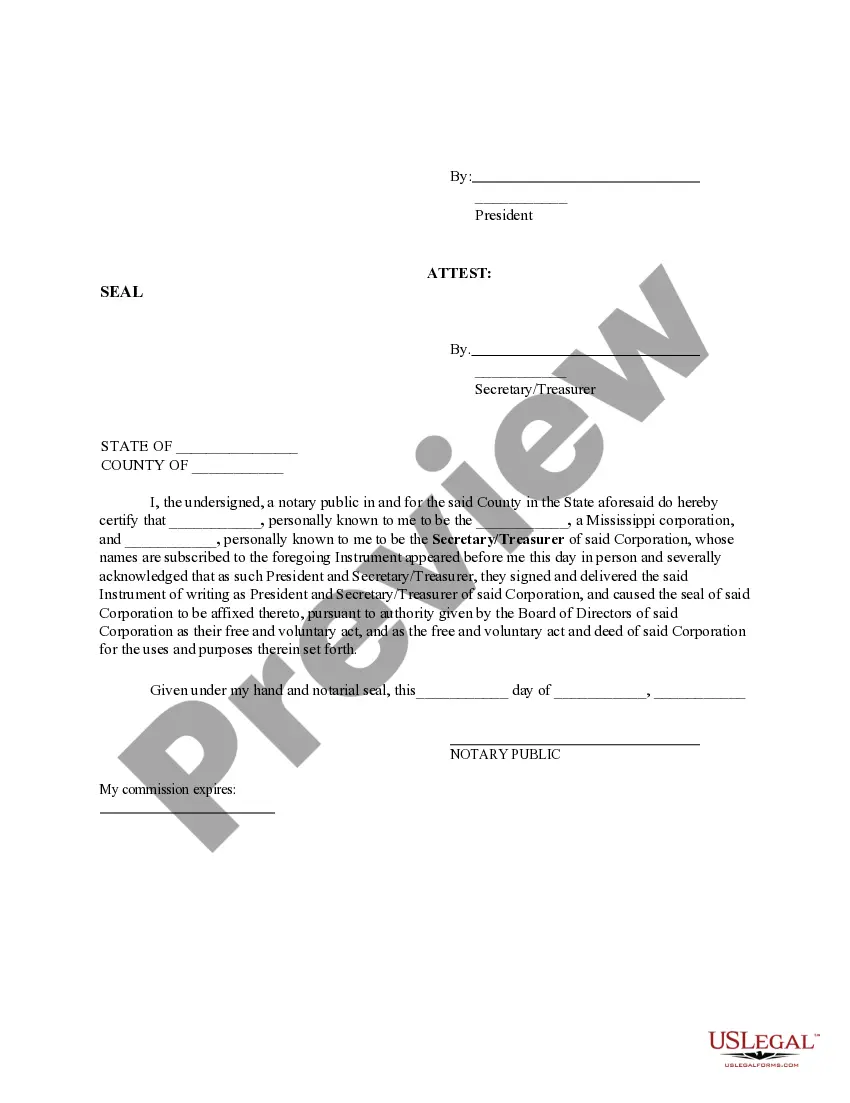

A Wake North Carolina Loan Guaranty Agreement is a legally binding contract between a lender and a guarantor in the state of North Carolina. It serves as a means to guarantee the repayment of a loan in case the borrower defaults on their obligations. This agreement provides an extra layer of security for lenders, ensuring that they can recover their funds even if the borrower is unable to repay the loan. Keywords: Wake North Carolina, Loan Guaranty Agreement, lender, guarantor, repayment, default, obligations, security, funds. There are different types of Wake North Carolina Loan Guaranty Agreements, each with its own purpose and terms. Some commonly known ones include: 1. Personal Loan Guaranty Agreement: This type of agreement is commonly used for personal loans where an individual acts as a guarantor for the borrower. The guarantor takes on the responsibility of repaying the loan if the borrower defaults. 2. Business Loan Guaranty Agreement: This agreement is specifically designed for business loans, where either an individual or another business entity acts as a guarantor. It ensures that the lender can recover the loan amount even if the borrower's business fails or faces financial difficulties. 3. Real Estate Loan Guaranty Agreement: This type of agreement applies to loans secured by real estate properties. The guarantor offers a guarantee that the loan will be repaid in full, either by the borrower or the guarantor themselves, in case of default. 4. Small Business Administration (SBA) Loan Guaranty Agreement: This agreement is specific to loans made by the Small Business Administration, which provides a guarantee to lenders that a portion of the loan will be repaid by the SBA in case of default. It encourages lenders to provide loans to small businesses by reducing the risk associated with lending. In summary, a Wake North Carolina Loan Guaranty Agreement is a legally binding contract that ensures lenders have an additional layer of security when providing loans. It covers various types of loans, including personal, business, real estate, and those supported by the Small Business Administration. The agreement serves to protect lenders' funds and encourages economic growth by enabling easier access to credit.

Wake North Carolina Loan Guaranty Agreement

Description

How to fill out Wake North Carolina Loan Guaranty Agreement?

Laws and regulations in every area differ from state to state. If you're not an attorney, it's easy to get lost in various norms when it comes to drafting legal documentation. To avoid costly legal assistance when preparing the Wake Loan Guaranty Agreement, you need a verified template legitimate for your county. That's when using the US Legal Forms platform is so advantageous.

US Legal Forms is a trusted by millions online library of more than 85,000 state-specific legal templates. It's a great solution for specialists and individuals looking for do-it-yourself templates for various life and business scenarios. All the documents can be used many times: once you pick a sample, it remains available in your profile for further use. Therefore, if you have an account with a valid subscription, you can just log in and re-download the Wake Loan Guaranty Agreement from the My Forms tab.

For new users, it's necessary to make a couple of more steps to get the Wake Loan Guaranty Agreement:

- Take a look at the page content to make sure you found the correct sample.

- Utilize the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your criteria.

- Utilize the Buy Now button to get the document when you find the right one.

- Opt for one of the subscription plans and log in or create an account.

- Decide how you prefer to pay for your subscription (with a credit card or PayPal).

- Select the format you want to save the document in and click Download.

- Complete and sign the document in writing after printing it or do it all electronically.

That's the simplest and most cost-effective way to get up-to-date templates for any legal reasons. Find them all in clicks and keep your paperwork in order with the US Legal Forms!