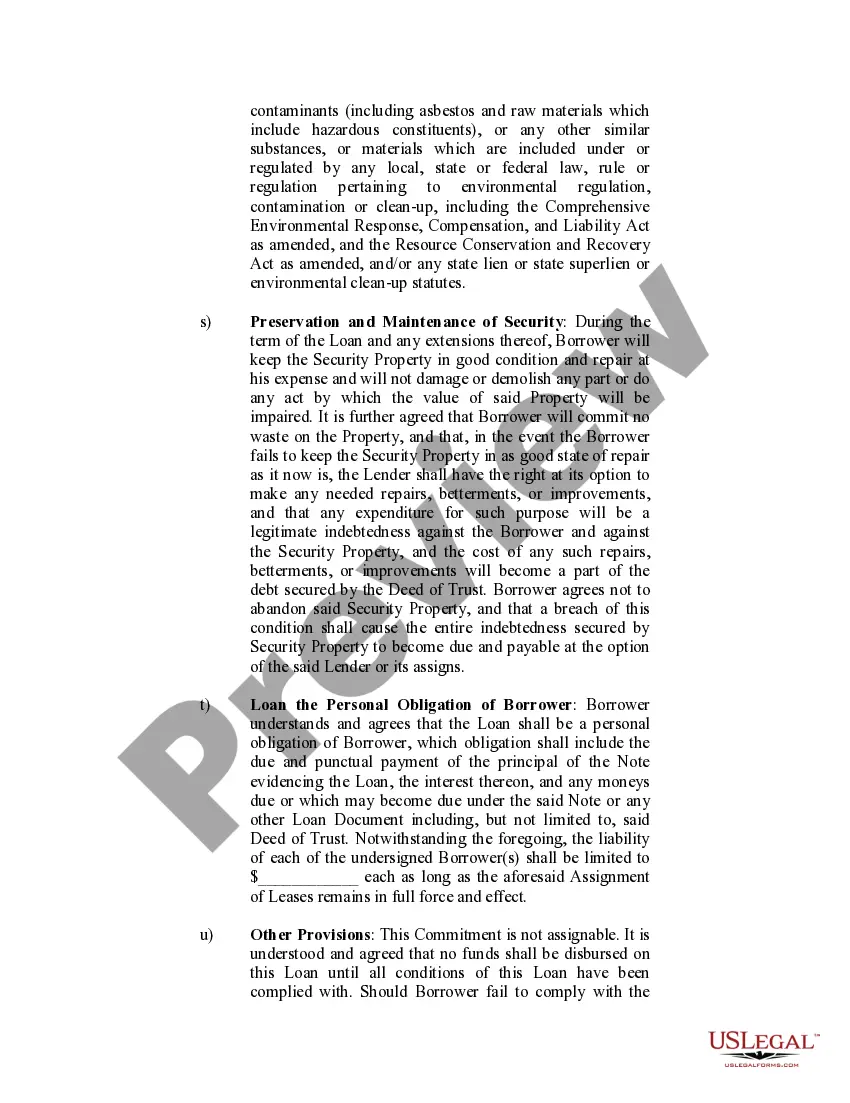

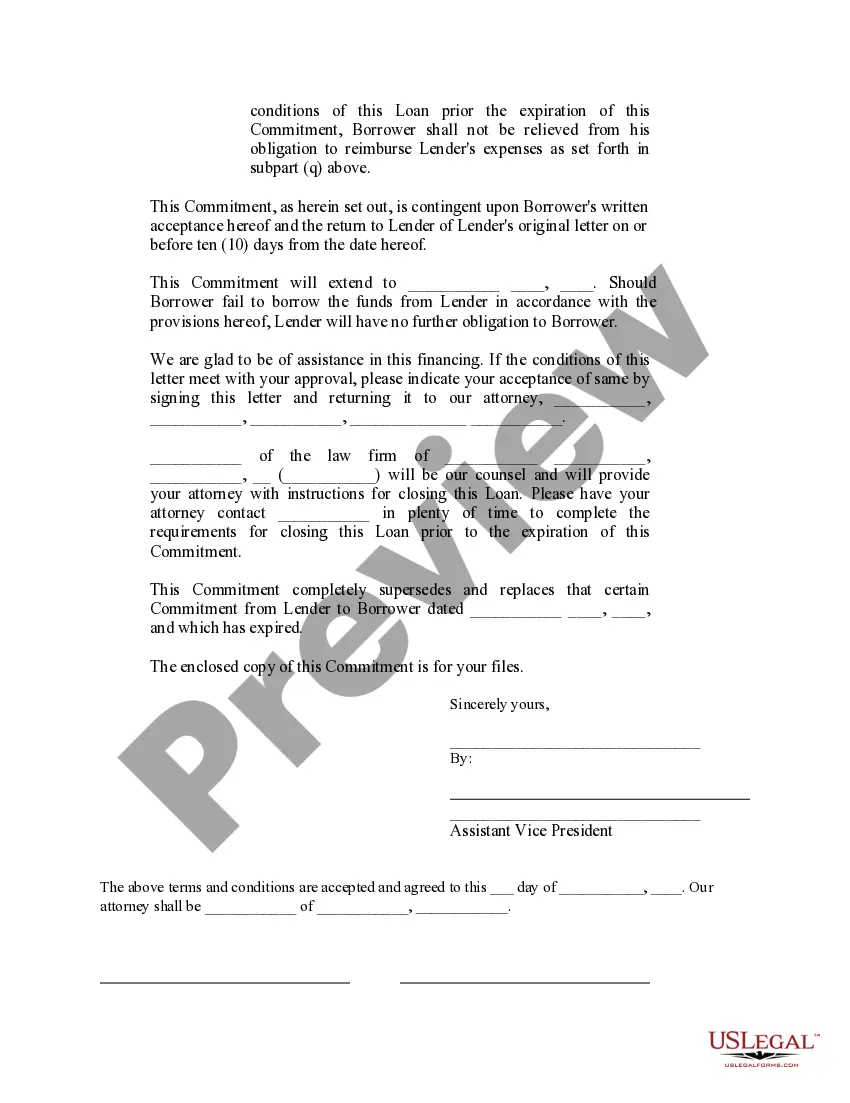

The Suffolk New York Loan Commitment Agreement refers to a legally binding document that outlines the terms and conditions between a lender and a borrower in Suffolk County, New York. The agreement serves as a commitment from the lender to provide a loan to the borrower, subject to certain conditions being met. This agreement is commonly used in various financial transactions, such as real estate purchases and business financing, where individuals or companies require funds for specific purposes. It ensures that both parties are on the same page regarding the loan, interest rates, repayment terms, and any collateral or security involved. There are several types of Loan Commitment Agreements that are commonly used in Suffolk New York: 1. Mortgage Loan Commitment Agreement: This type of agreement is prevalent in real estate transactions, particularly when purchasing a property. It specifies the terms under which the lender will provide the mortgage loan, including the loan amount, interest rate, repayment period, and any conditions precedent to funding. 2. Business Loan Commitment Agreement: This agreement is specifically designed for companies seeking financing for their operations, expansion plans, or capital investments. It outlines the terms and conditions under which the lender will provide the loan, such as the loan amount, interest rate, repayment terms, and any covenants or requirements imposed on the borrower. 3. Personal Loan Commitment Agreement: This type of agreement is tailored for individuals who require financial assistance for personal reasons, such as debt consolidation, education expenses, or major purchases. It typically covers the loan amount, interest rate, repayment schedule, and any specific provisions mutually agreed upon by the lender and the borrower. 4. Construction Loan Commitment Agreement: This agreement is common in the construction industry, where parties involved in a building project require financing. It includes details about the loan amount, interest rate, disbursement schedule, and any conditions the borrower must meet to receive the funds, such as progress milestones or inspections. Regardless of the specific type, the Suffolk New York Loan Commitment Agreement plays a crucial role in formalizing the lending process and safeguarding the interests of both the lender and the borrower. It ensures transparency, clarity, and legal enforceability of financial transactions in Suffolk County, New York.

Suffolk New York Loan Commitment Agreement

Description

How to fill out Suffolk New York Loan Commitment Agreement?

Draftwing paperwork, like Suffolk Loan Commitment Agreement, to take care of your legal affairs is a tough and time-consumming task. Many cases require an attorney’s participation, which also makes this task expensive. However, you can consider your legal affairs into your own hands and take care of them yourself. US Legal Forms is here to save the day. Our website comes with over 85,000 legal documents crafted for a variety of scenarios and life situations. We ensure each document is in adherence with the regulations of each state, so you don’t have to be concerned about potential legal pitfalls compliance-wise.

If you're already familiar with our services and have a subscription with US, you know how easy it is to get the Suffolk Loan Commitment Agreement form. Go ahead and log in to your account, download the template, and customize it to your needs. Have you lost your document? No worries. You can get it in the My Forms tab in your account - on desktop or mobile.

The onboarding process of new users is fairly easy! Here’s what you need to do before downloading Suffolk Loan Commitment Agreement:

- Make sure that your form is specific to your state/county since the rules for creating legal papers may vary from one state another.

- Discover more information about the form by previewing it or reading a brief description. If the Suffolk Loan Commitment Agreement isn’t something you were hoping to find, then use the header to find another one.

- Sign in or create an account to begin using our website and get the form.

- Everything looks good on your side? Click the Buy now button and select the subscription option.

- Select the payment gateway and enter your payment information.

- Your form is all set. You can go ahead and download it.

It’s easy to find and buy the needed template with US Legal Forms. Thousands of businesses and individuals are already taking advantage of our extensive library. Subscribe to it now if you want to check what other advantages you can get with US Legal Forms!