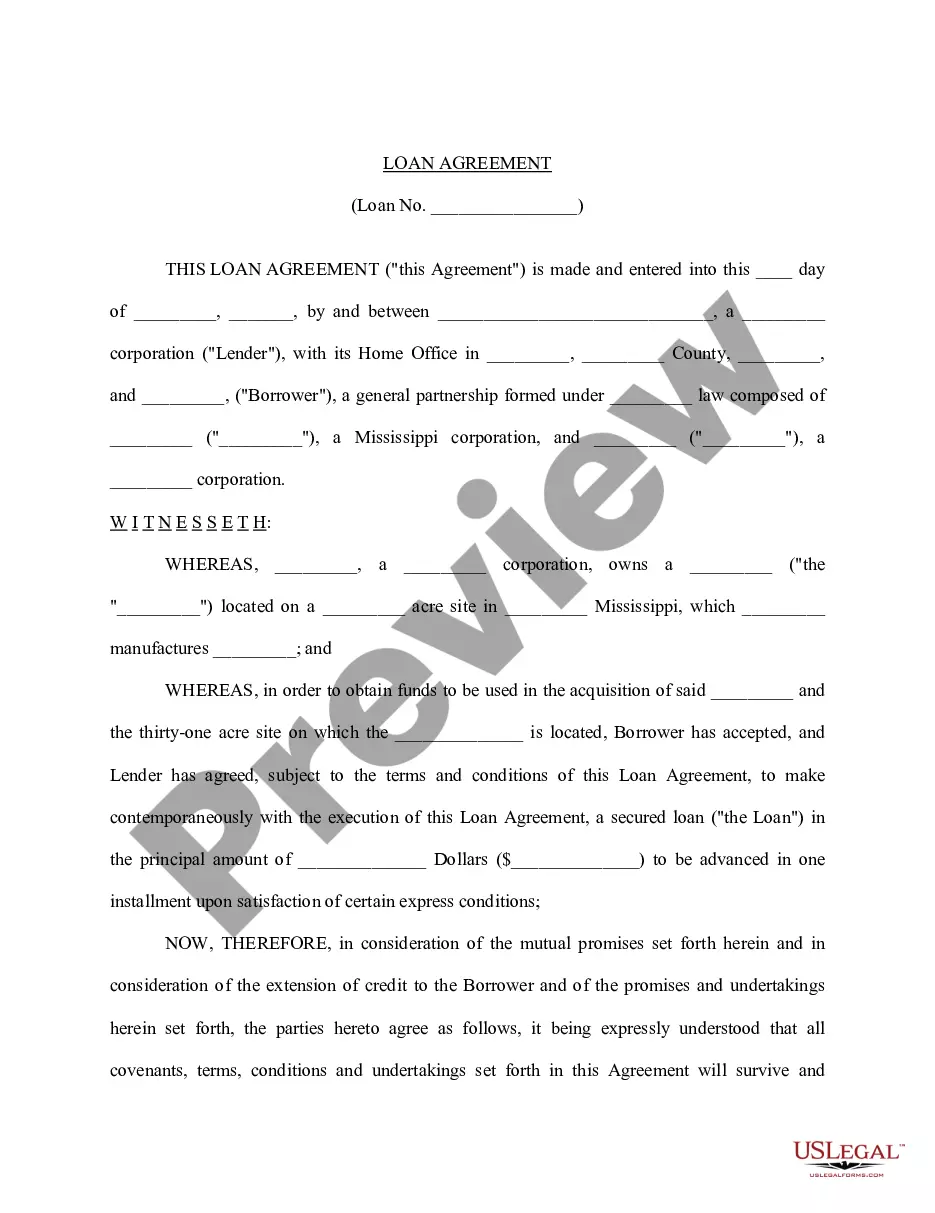

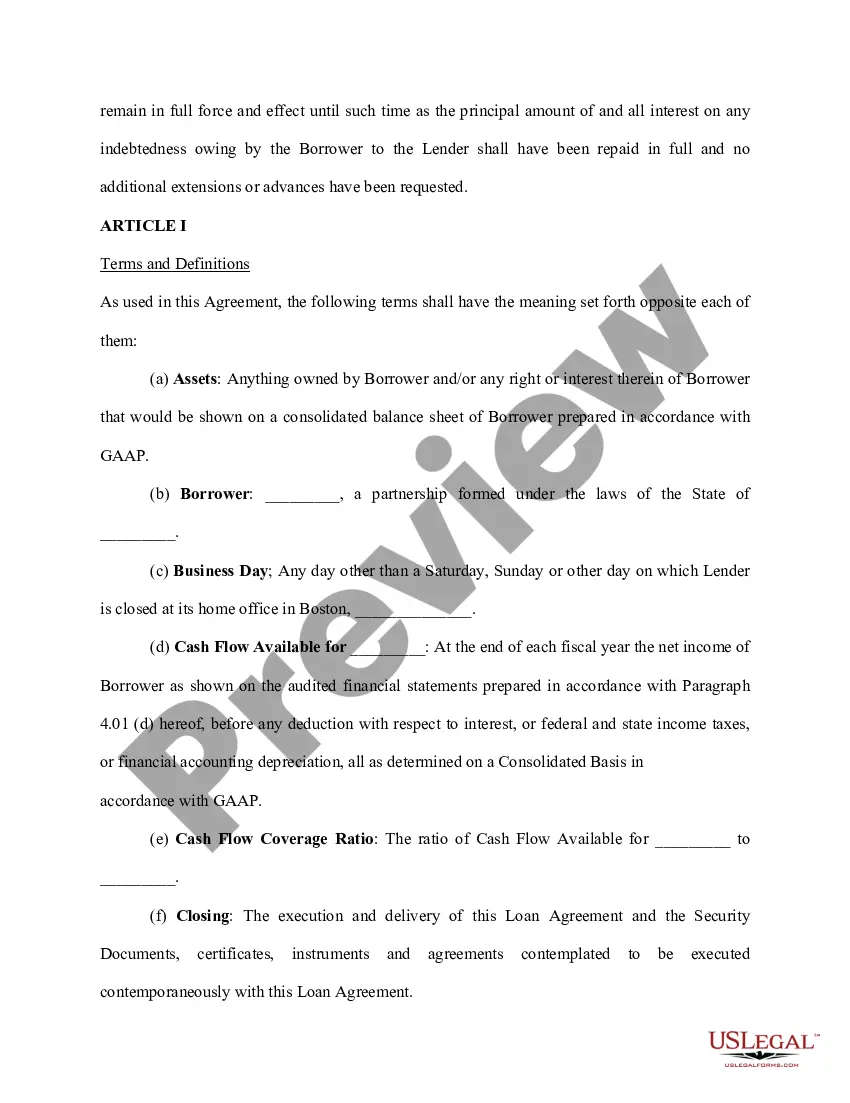

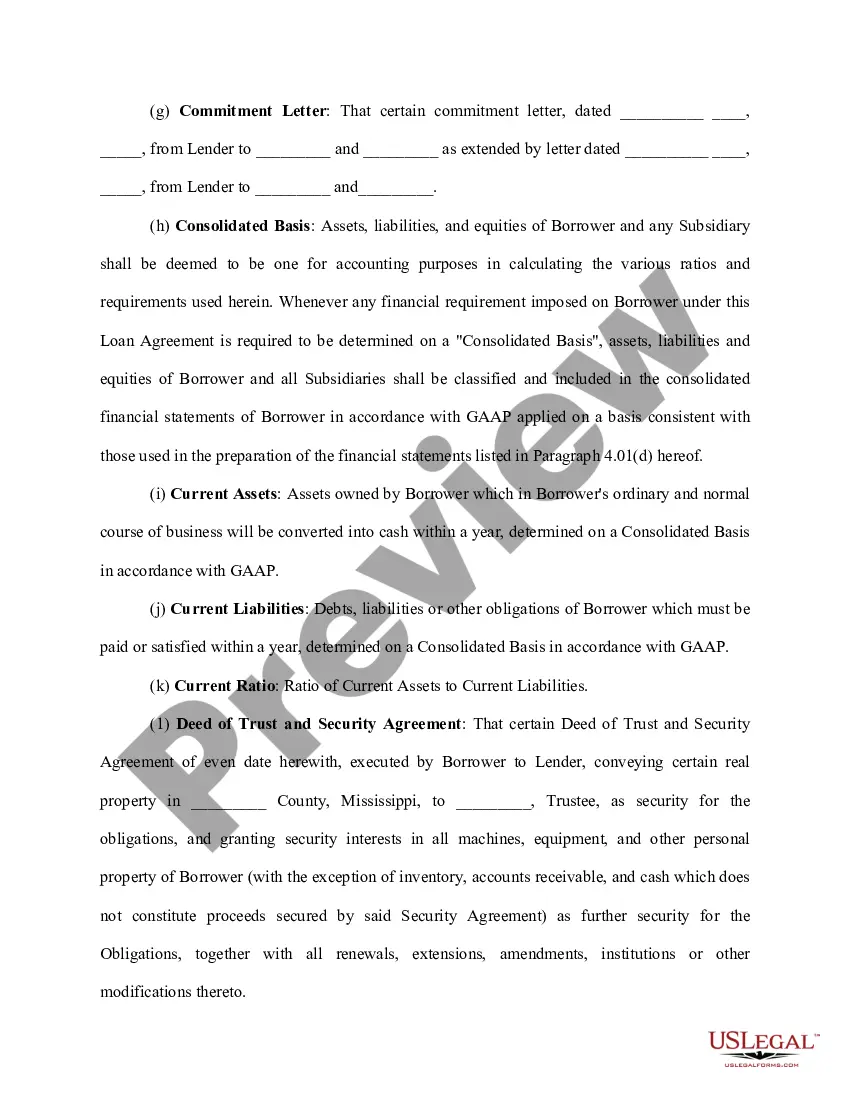

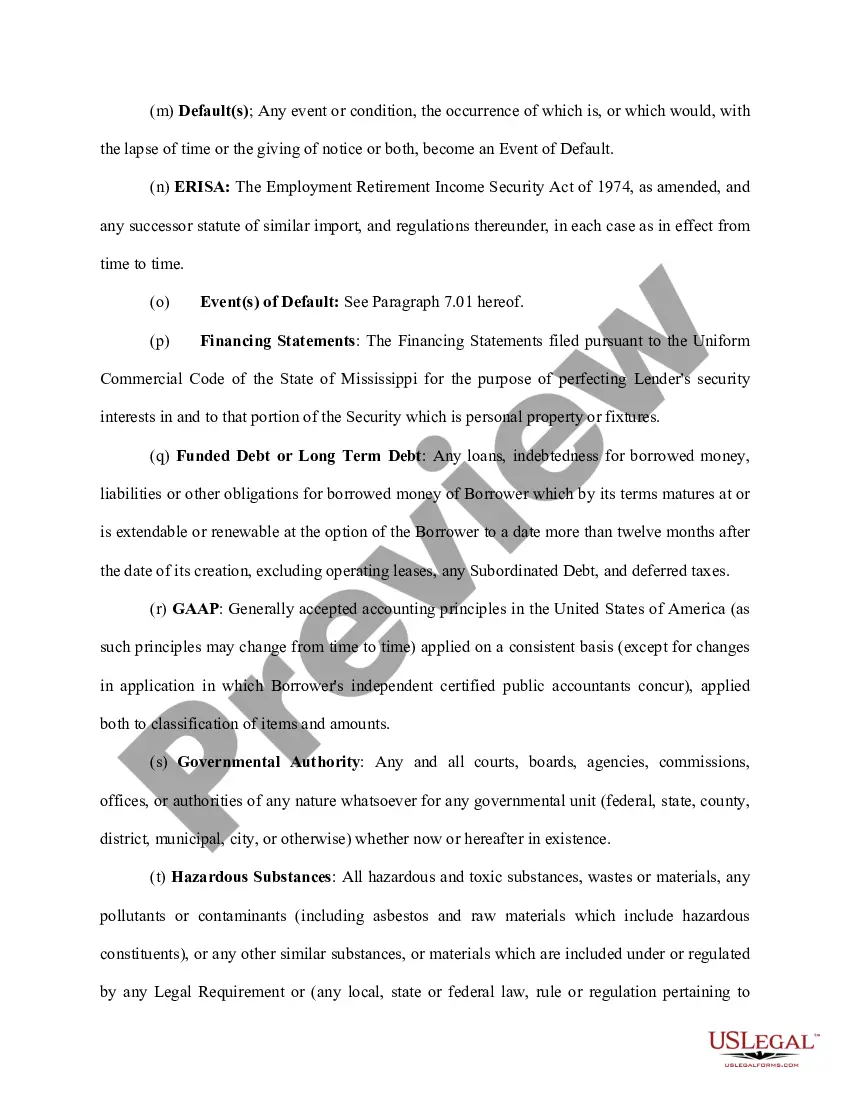

Franklin Ohio Loan Agreement for Family Member is a legally binding contract that outlines the terms and conditions of a loan agreement between family members in Franklin, Ohio. This agreement ensures transparency, clarity, and mutual understanding between the lender and borrower within a familial context. Keywords: Franklin Ohio, loan agreement, family member, terms and conditions, legally binding, transparency, clarity, mutual understanding, lender, borrower, familial context. Different types of Franklin Ohio Loan Agreement for Family Member may include: 1. Secured Loan Agreement: This type of loan agreement involves collateral or assets provided by the borrower as security for the loan. In case of default, the lender has the right to claim the collateral. 2. Unsecured Loan Agreement: In this agreement, no collateral is involved. The loan is based solely on the borrower's creditworthiness, financial stability, and trust between family members. 3. Promissory Note: A promissory note is a written promise to repay a loan according to agreed-upon terms. It includes details such as the loan amount, interest rate, repayment schedule, and consequences of default. 4. Lump-Sum Loan Agreement: A lump-sum loan agreement involves borrowing a fixed amount of money from a family member and repaying it in one installment by a specified date. 5. Installment Loan Agreement: Under this agreement, the loan amount is repaid in regular installments over a predetermined period. The terms include the installment amount, frequency, and length of the repayment period. 6. Interfamily Loan Agreement: This type of loan agreement specifies the relationship between the lender and borrower as family members and may include specific terms and conditions that are unique to family loans, such as forgiveness clauses or lower interest rates. It is vital to consult with a legal professional experienced in finance or contract law to ensure compliance with state laws and to customize the loan agreement to the specific needs and circumstances of both parties involved.

Franklin Ohio Loan Agreement for Family Member

Description

How to fill out Franklin Ohio Loan Agreement For Family Member?

A document routine always goes along with any legal activity you make. Creating a company, applying or accepting a job offer, transferring property, and lots of other life situations demand you prepare formal paperwork that varies throughout the country. That's why having it all collected in one place is so valuable.

US Legal Forms is the largest online library of up-to-date federal and state-specific legal forms. Here, you can easily locate and get a document for any personal or business objective utilized in your region, including the Franklin Loan Agreement for Family Member.

Locating samples on the platform is remarkably simple. If you already have a subscription to our service, log in to your account, find the sample through the search field, and click Download to save it on your device. Afterward, the Franklin Loan Agreement for Family Member will be available for further use in the My Forms tab of your profile.

If you are dealing with US Legal Forms for the first time, adhere to this quick guideline to get the Franklin Loan Agreement for Family Member:

- Make sure you have opened the proper page with your localised form.

- Use the Preview mode (if available) and scroll through the sample.

- Read the description (if any) to ensure the form corresponds to your requirements.

- Search for another document via the search option in case the sample doesn't fit you.

- Click Buy Now once you locate the required template.

- Select the suitable subscription plan, then sign in or register for an account.

- Select the preferred payment method (with credit card or PayPal) to continue.

- Choose file format and download the Franklin Loan Agreement for Family Member on your device.

- Use it as needed: print it or fill it out electronically, sign it, and file where requested.

This is the simplest and most reliable way to obtain legal documents. All the samples provided by our library are professionally drafted and checked for correspondence to local laws and regulations. Prepare your paperwork and manage your legal affairs effectively with the US Legal Forms!