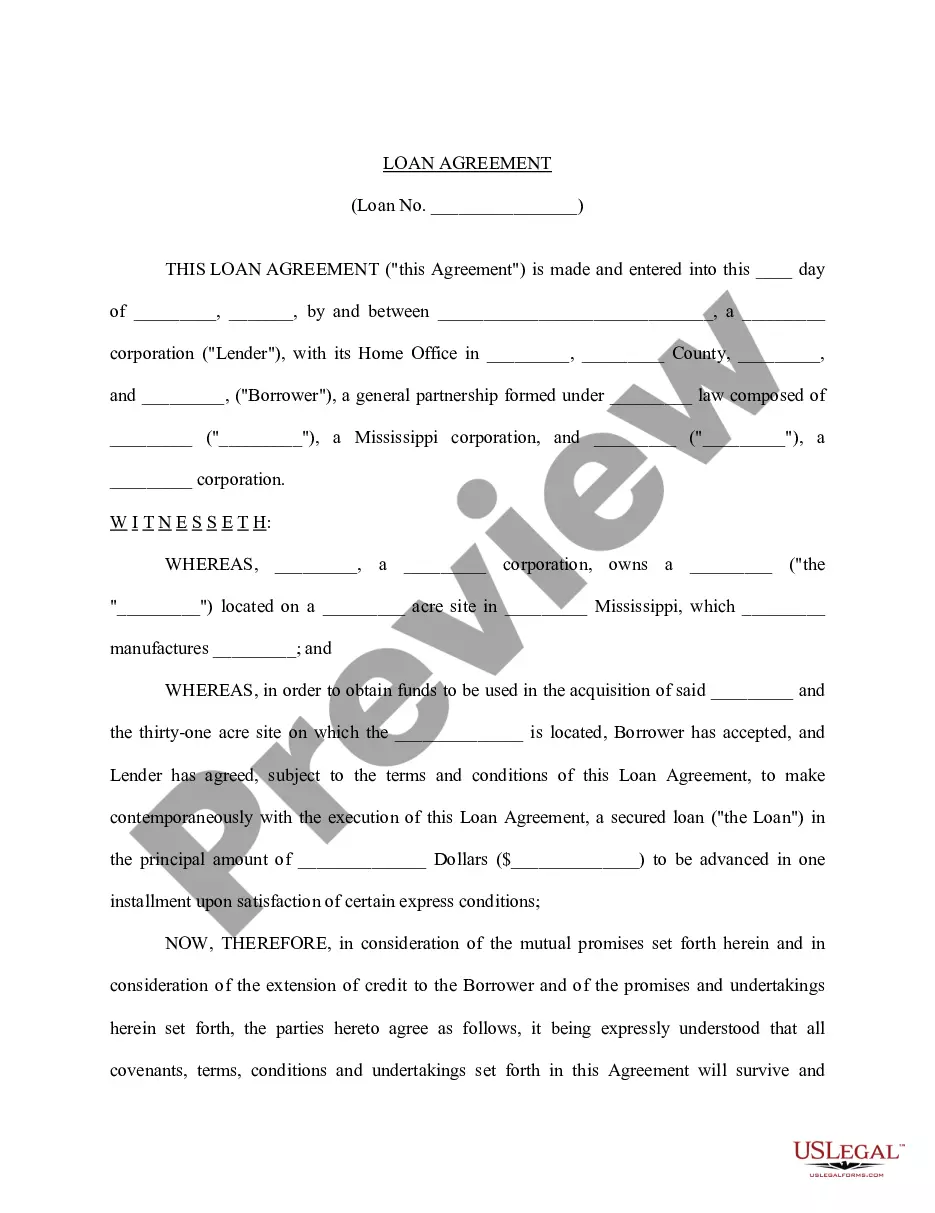

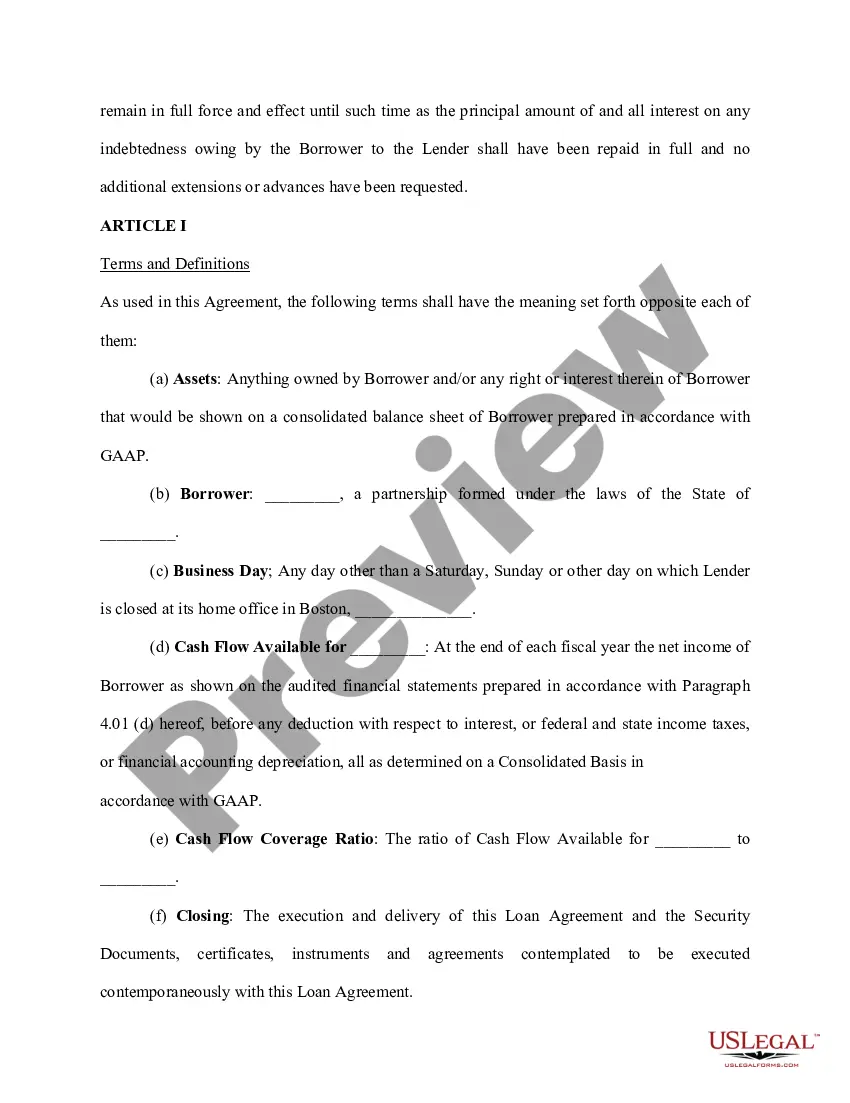

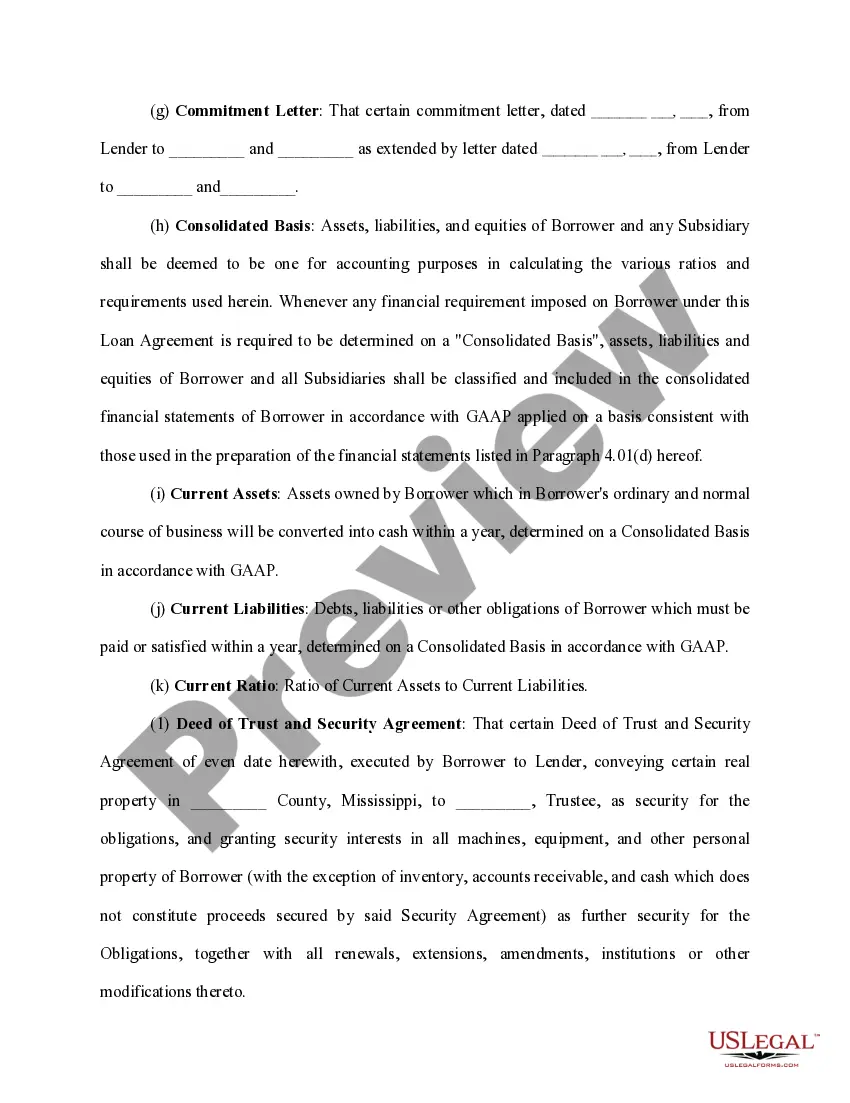

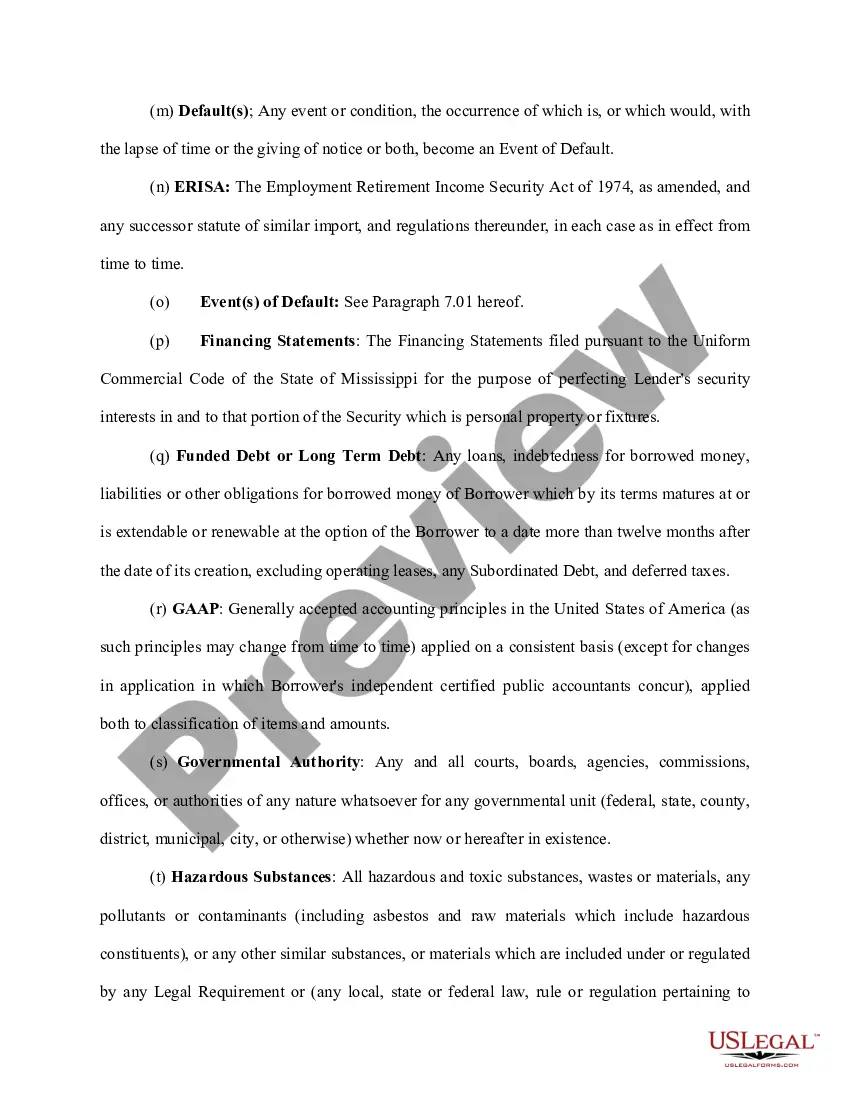

Maricopa Arizona Loan Agreement for Equipment is a legal contract outlining the terms and conditions between a lender and a borrower regarding the financing of equipment in Maricopa, Arizona. This agreement serves as a binding document that specifies the obligations, responsibilities, and rights of both parties involved. The purpose of the Maricopa Arizona Loan Agreement for Equipment is to establish a clear understanding of the loaned equipment, its usage, and the repayment terms. It ensures that the lender receives the agreed compensation for providing the equipment while safeguarding the borrower's interests by defining the conditions and restrictions associated with the loan. In Maricopa, Arizona, there are several types of Loan Agreements for Equipment available: 1. Operating Lease Agreement for Equipment: This type of loan agreement allows the borrower to use the equipment for a specific duration while paying periodic lease payments. At the end of the lease term, the borrower can either return the equipment or purchase it at a predetermined price. 2. Finance Lease Agreement for Equipment: This agreement provides the borrower with a way to acquire the equipment for an extended period while making fixed monthly payments. After completing the lease term, the borrower usually has the option to purchase the equipment at its fair market value or return it. 3. Capital Lease Agreement for Equipment: This type of loan agreement allows the borrower to lease the equipment for a more extended period, often closer to the equipment's useful life. The borrower is treated as the owner of the equipment for accounting and tax purposes and is responsible for maintaining and insuring it throughout the lease term. 4. Sale-Leaseback Agreement for Equipment: In this arrangement, the borrower sells an owned piece of equipment to the lender and subsequently leases it back. This type of agreement provides the borrower with immediate cash while allowing continued usage of the equipment. The Maricopa Arizona Loan Agreement for Equipment includes vital elements such as detailed descriptions of the equipment, loan amount, interest rates, repayment terms, default provisions, insurance requirements, and any additional terms agreed upon by both parties. It is crucial for both the lender and the borrower to thoroughly review and understand all the provisions within the agreement before signing to ensure a mutually beneficial agreement and avoid any potential disputes.

Maricopa Arizona Loan Agreement for Equipment

Description

How to fill out Maricopa Arizona Loan Agreement For Equipment?

A document routine always accompanies any legal activity you make. Creating a company, applying or accepting a job offer, transferring property, and lots of other life situations require you prepare formal documentation that varies throughout the country. That's why having it all collected in one place is so valuable.

US Legal Forms is the largest online collection of up-to-date federal and state-specific legal templates. On this platform, you can easily locate and download a document for any personal or business purpose utilized in your region, including the Maricopa Loan Agreement for Equipment.

Locating templates on the platform is extremely simple. If you already have a subscription to our service, log in to your account, find the sample using the search bar, and click Download to save it on your device. After that, the Maricopa Loan Agreement for Equipment will be available for further use in the My Forms tab of your profile.

If you are dealing with US Legal Forms for the first time, adhere to this quick guideline to get the Maricopa Loan Agreement for Equipment:

- Make sure you have opened the right page with your regional form.

- Make use of the Preview mode (if available) and scroll through the template.

- Read the description (if any) to ensure the template corresponds to your needs.

- Search for another document using the search tab in case the sample doesn't fit you.

- Click Buy Now when you locate the necessary template.

- Decide on the suitable subscription plan, then log in or create an account.

- Select the preferred payment method (with credit card or PayPal) to continue.

- Opt for file format and download the Maricopa Loan Agreement for Equipment on your device.

- Use it as needed: print it or fill it out electronically, sign it, and send where requested.

This is the simplest and most trustworthy way to obtain legal paperwork. All the samples available in our library are professionally drafted and verified for correspondence to local laws and regulations. Prepare your paperwork and manage your legal affairs effectively with the US Legal Forms!