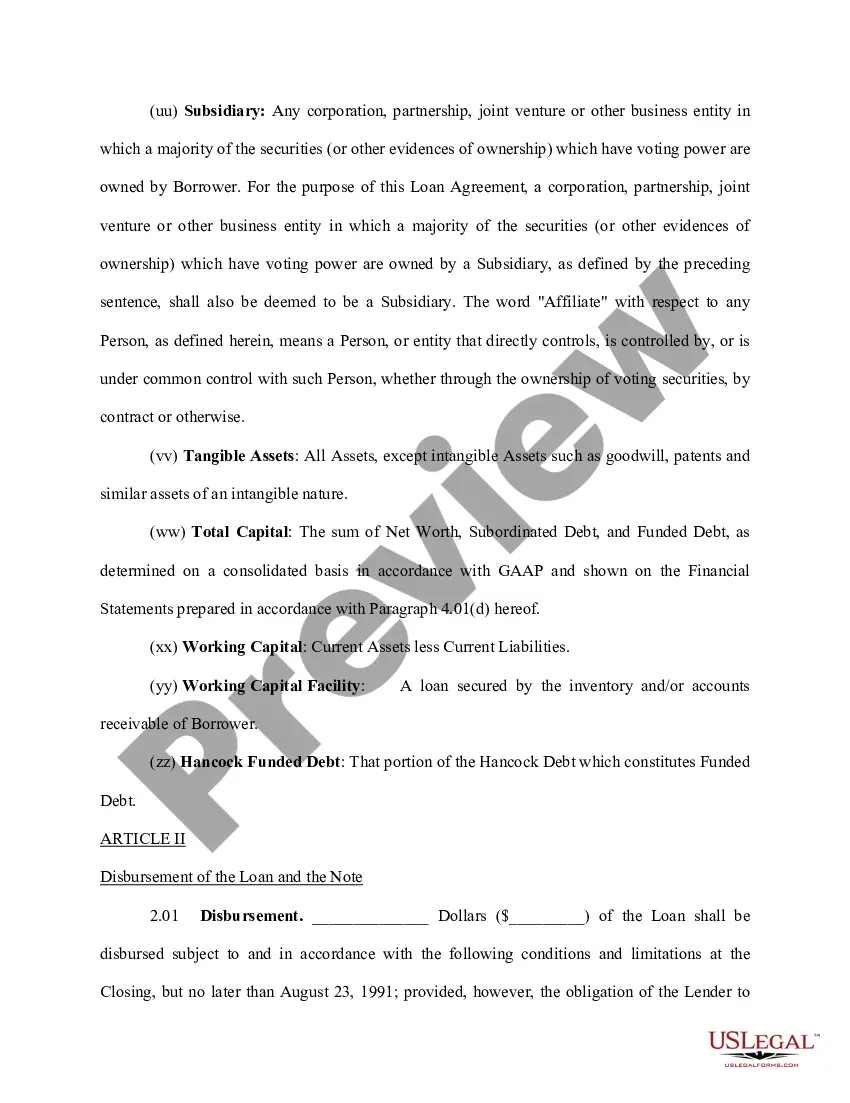

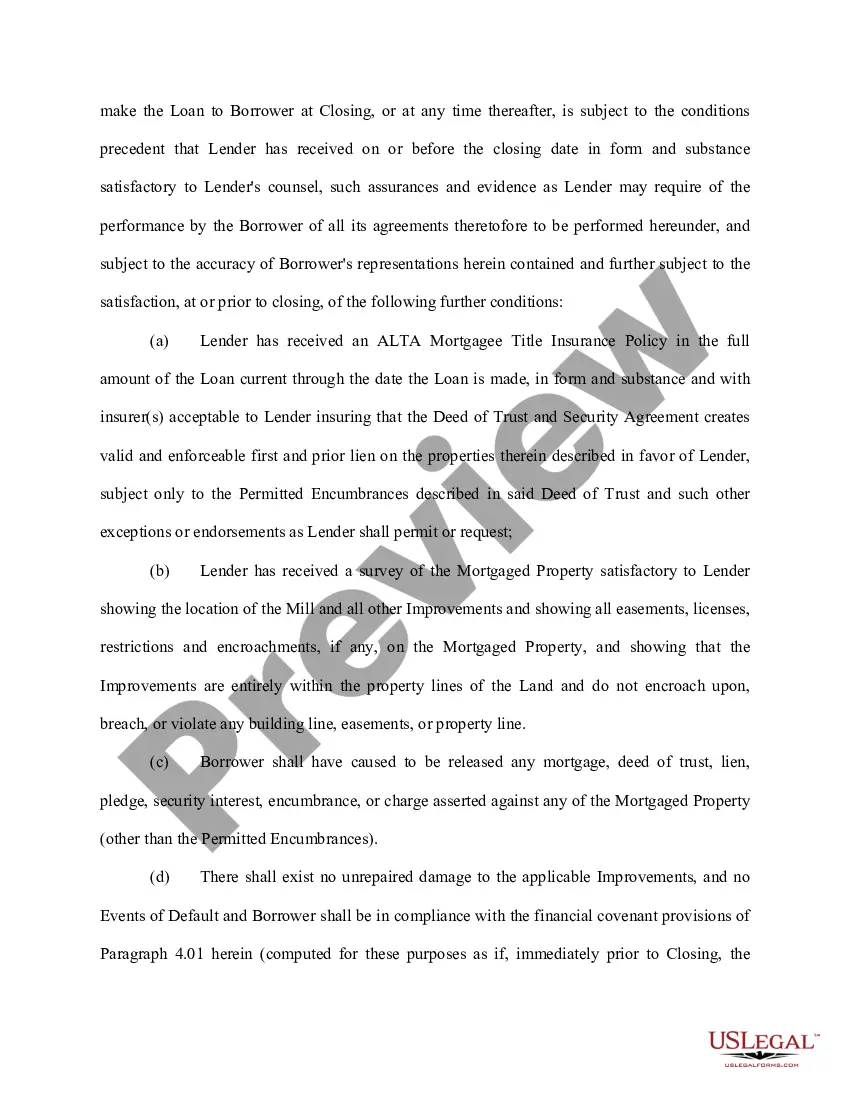

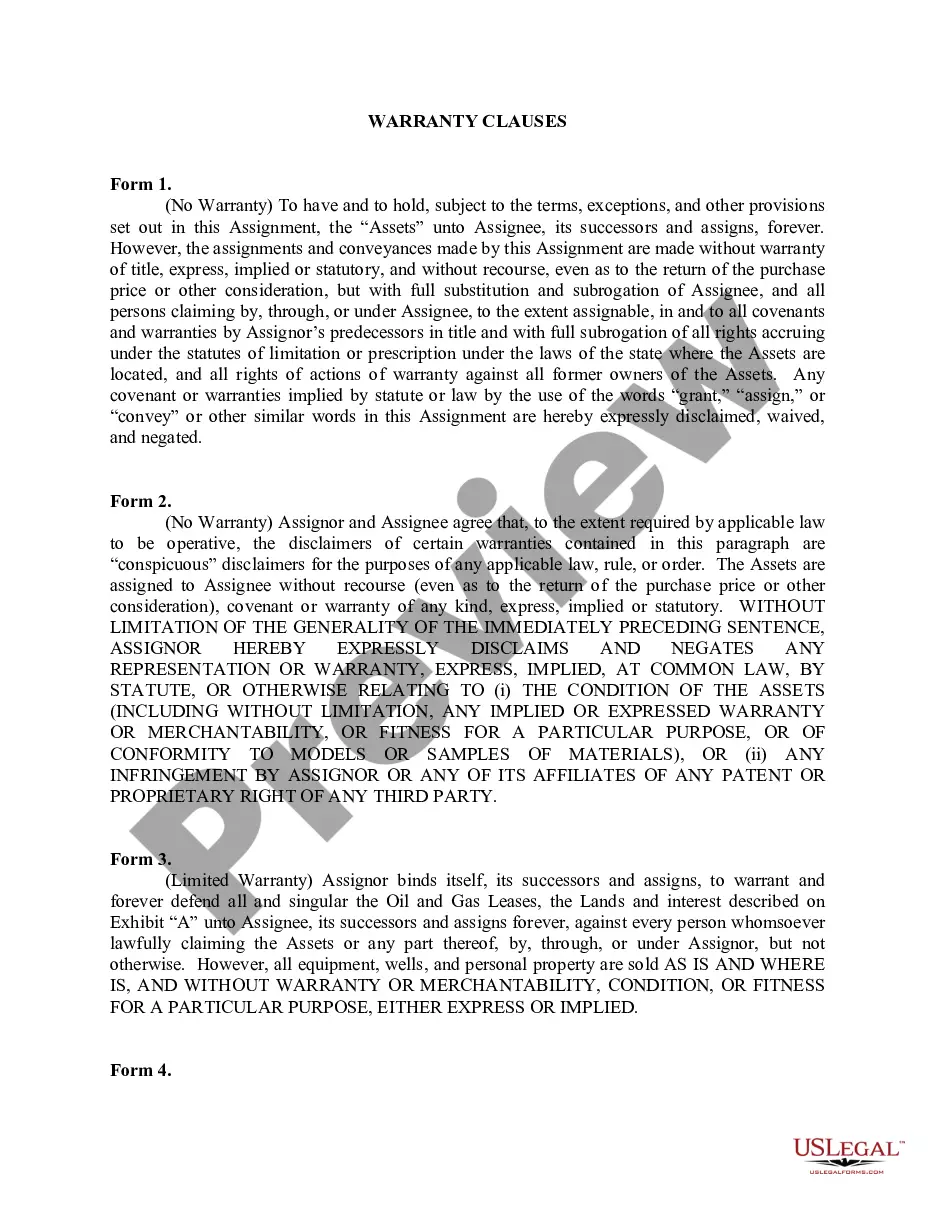

Los Angeles California Loan Agreement for Employees refers to a legally binding contract between an employer and an employee in Los Angeles, California, regarding the terms and conditions of a loan provided by the employer to the employee. This loan agreement outlines the loan amount, repayment terms, interest rates, and any other specific terms and conditions agreed upon by both parties. In Los Angeles, California, there are various types of loan agreements for employees that employers may offer: 1. Personal Loan Agreement: This type of loan agreement allows employees to borrow funds from their employer for personal reasons such as medical expenses, education, or home improvement. 2. Educational Loan Agreement: Employers may provide educational loans to employees who require financial assistance for pursuing higher education or skill development programs. 3. Relocation Loan Agreement: In the case of employees relocating to Los Angeles, companies may offer relocation loans to cover expenses related to moving and settling down, including housing deposits, transportation costs, or renting furniture. 4. Emergency Loan Agreement: Sometimes, employees may face unforeseen financial emergencies. Employers may offer emergency loans to assist employees in managing such situations, like medical emergencies or unexpected repairs. 5. Travel Loan Agreement: For business-related travel, companies may offer employees travel loans to cover expenses such as airfare, accommodations, and meals during their business trip. 6. Technology Loan Agreement: In industries where technological tools are crucial, employers may provide loans for employees to purchase laptops, smartphones, or other necessary technological devices. Whatever the type of loan agreement, it is essential for both the employer and the employee to carefully read and understand the terms and conditions before signing the agreement. The loan agreement should specify the loan repayment schedule, interest rates, any penalties or fees for late payments, and consequences of defaulting on the loan. To ensure a fair loan agreement for all parties involved, it is advisable to consult with legal professionals to draft or review such agreements, complying with the relevant employment laws and regulations in Los Angeles, California.

Los Angeles California Loan Agreement for Employees

Description

How to fill out Los Angeles California Loan Agreement For Employees?

Preparing paperwork for the business or personal needs is always a huge responsibility. When drawing up a contract, a public service request, or a power of attorney, it's essential to take into account all federal and state laws and regulations of the particular area. However, small counties and even cities also have legislative procedures that you need to consider. All these details make it tense and time-consuming to create Los Angeles Loan Agreement for Employees without expert help.

It's easy to avoid spending money on attorneys drafting your documentation and create a legally valid Los Angeles Loan Agreement for Employees by yourself, using the US Legal Forms online library. It is the biggest online catalog of state-specific legal templates that are professionally verified, so you can be certain of their validity when selecting a sample for your county. Earlier subscribed users only need to log in to their accounts to download the needed document.

If you still don't have a subscription, follow the step-by-step guideline below to obtain the Los Angeles Loan Agreement for Employees:

- Look through the page you've opened and verify if it has the sample you require.

- To accomplish this, use the form description and preview if these options are presented.

- To find the one that meets your requirements, utilize the search tab in the page header.

- Recheck that the sample complies with juridical criteria and click Buy Now.

- Choose the subscription plan, then sign in or register for an account with the US Legal Forms.

- Utilize your credit card or PayPal account to pay for your subscription.

- Download the selected file in the preferred format, print it, or fill it out electronically.

The great thing about the US Legal Forms library is that all the documentation you've ever purchased never gets lost - you can get it in your profile within the My Forms tab at any moment. Join the platform and easily get verified legal forms for any situation with just a few clicks!