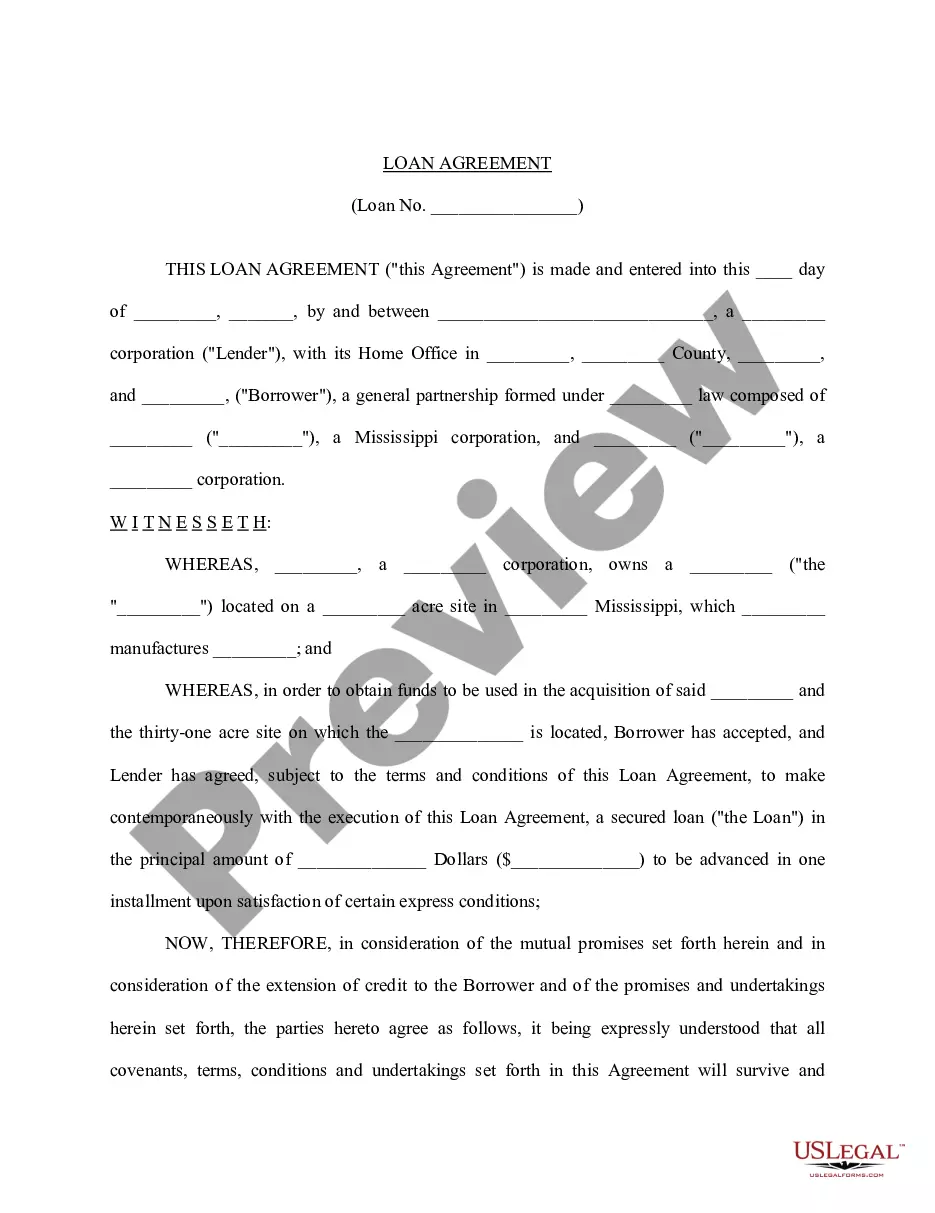

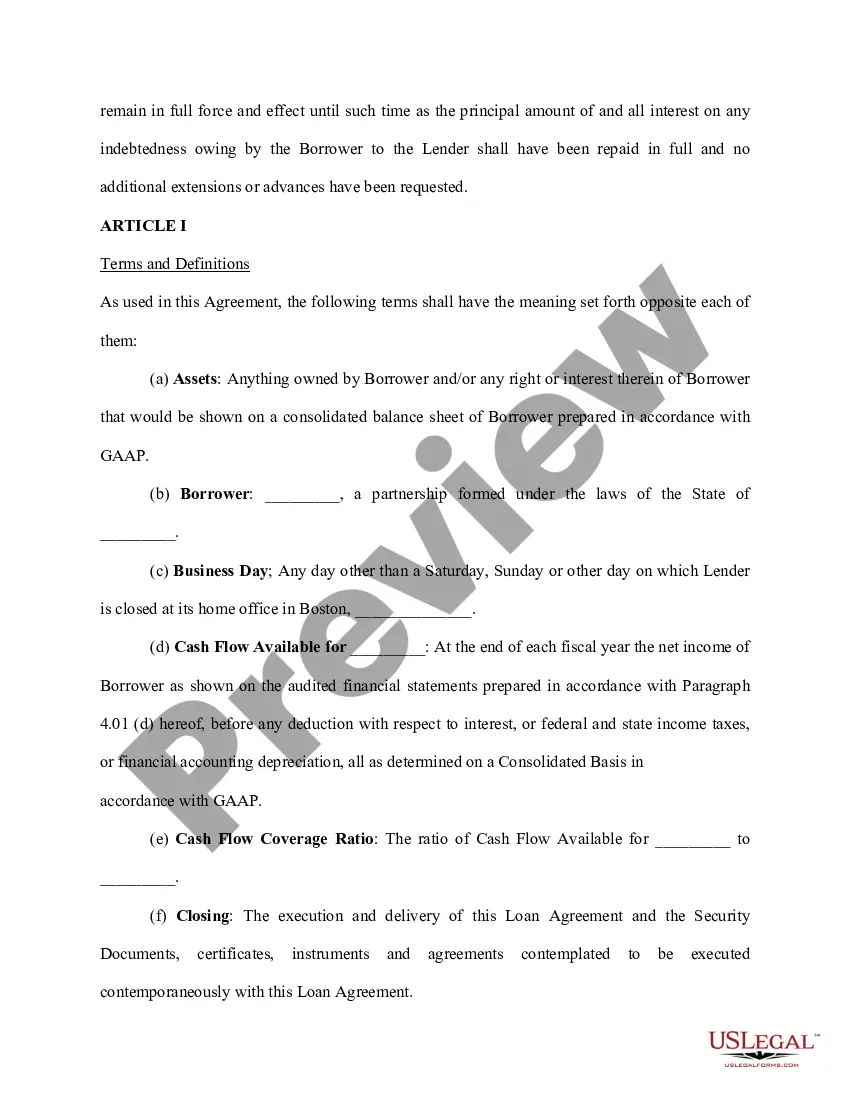

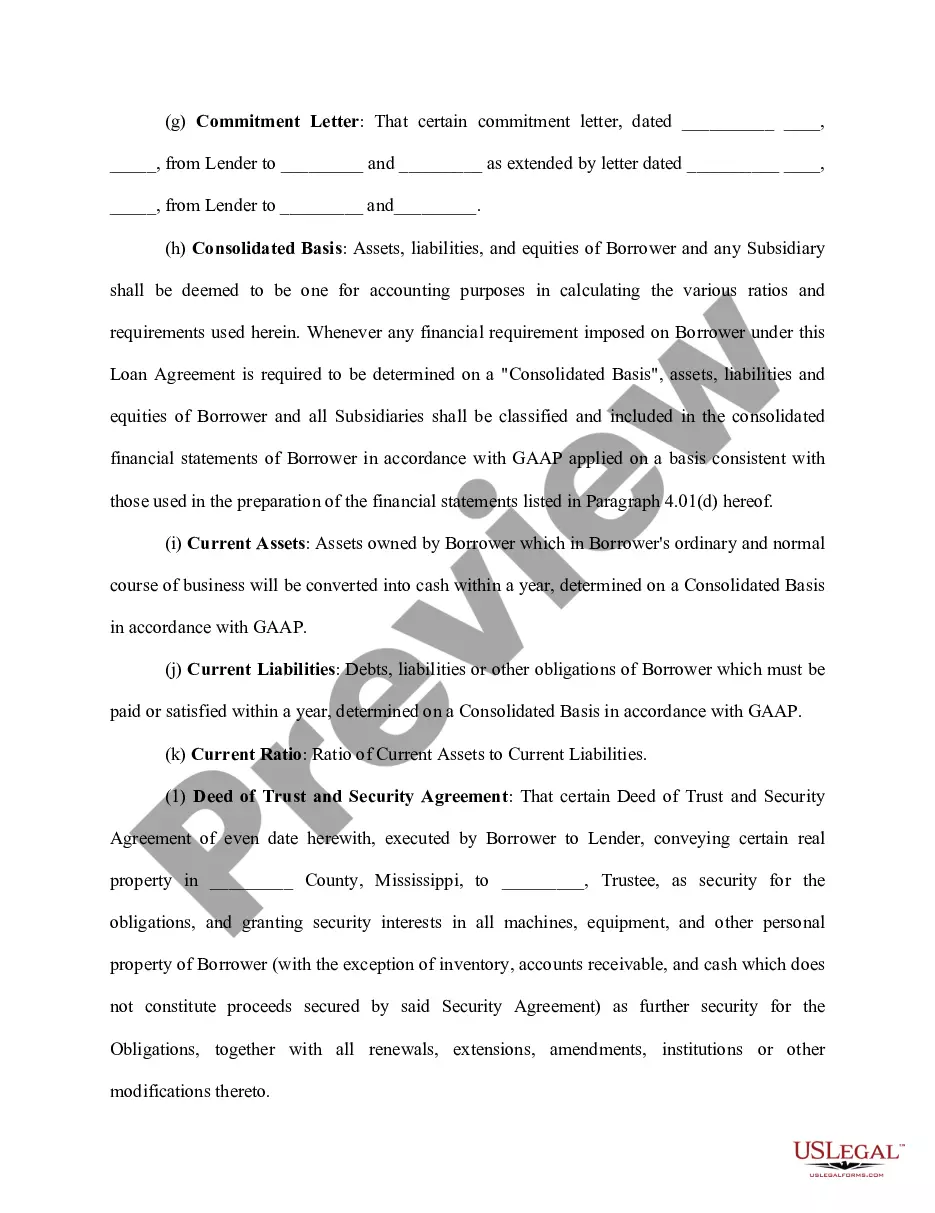

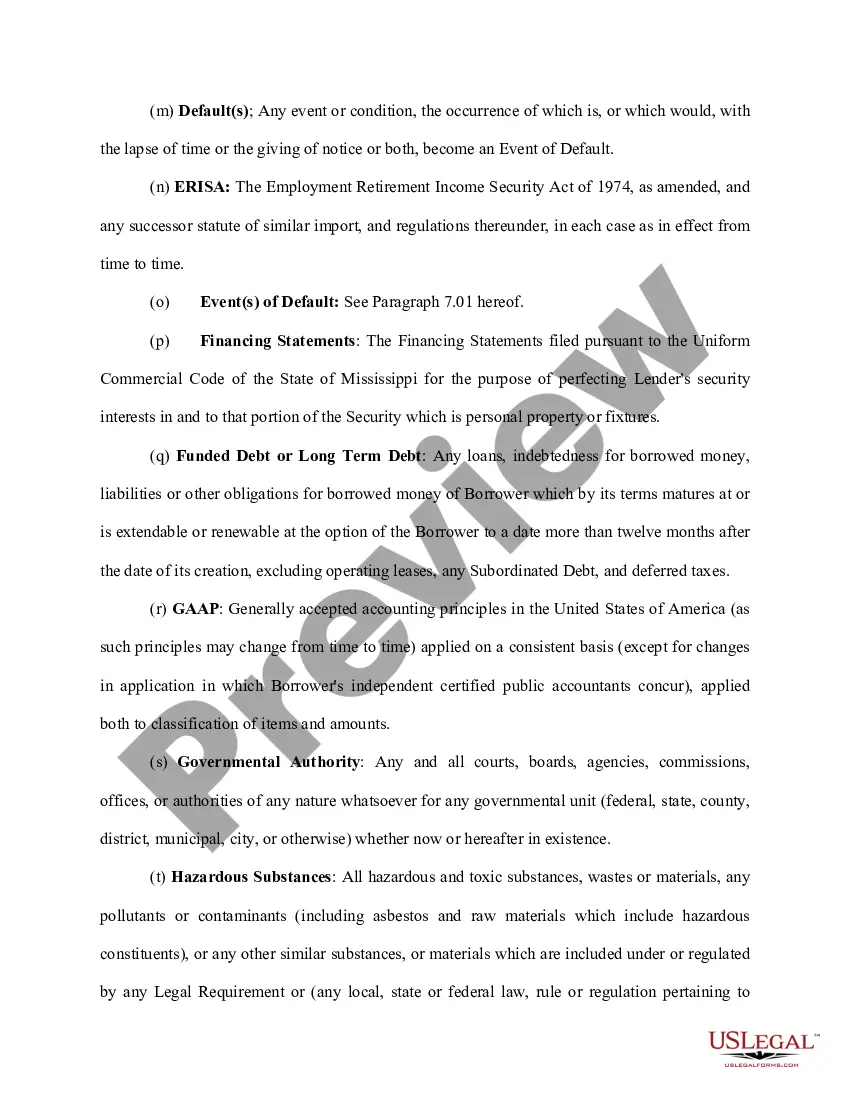

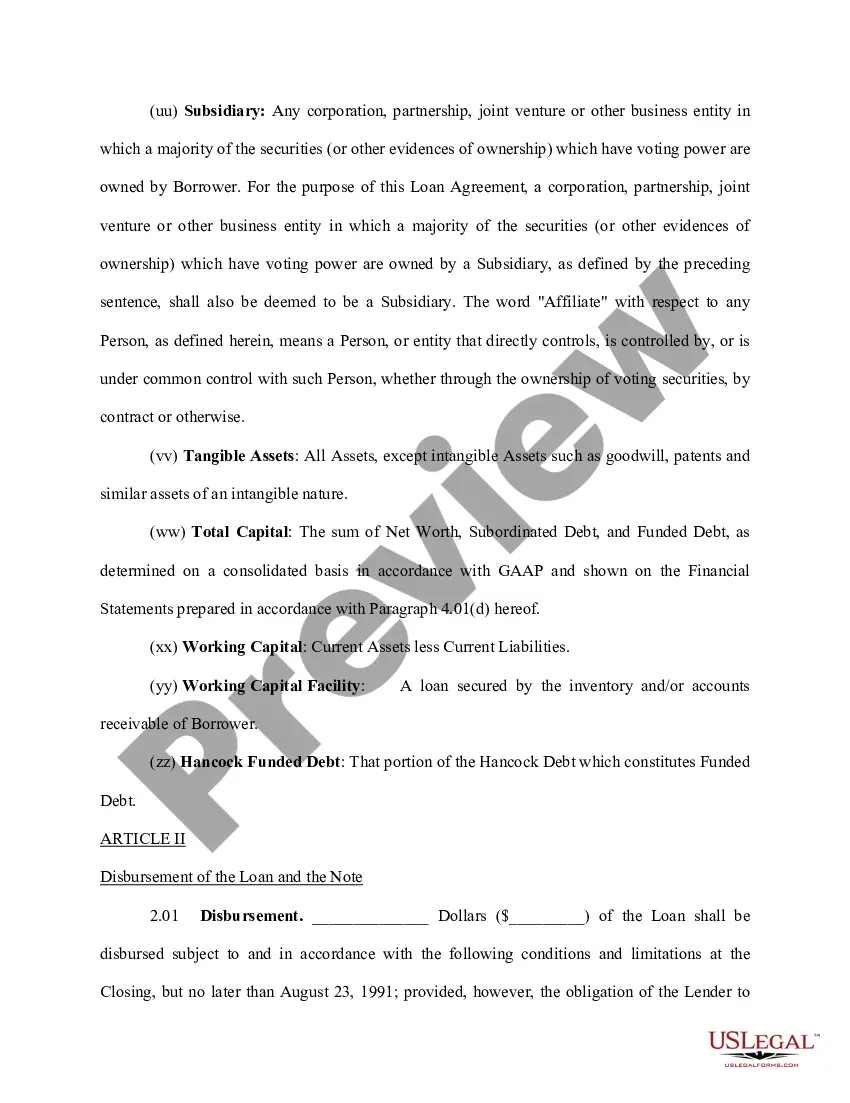

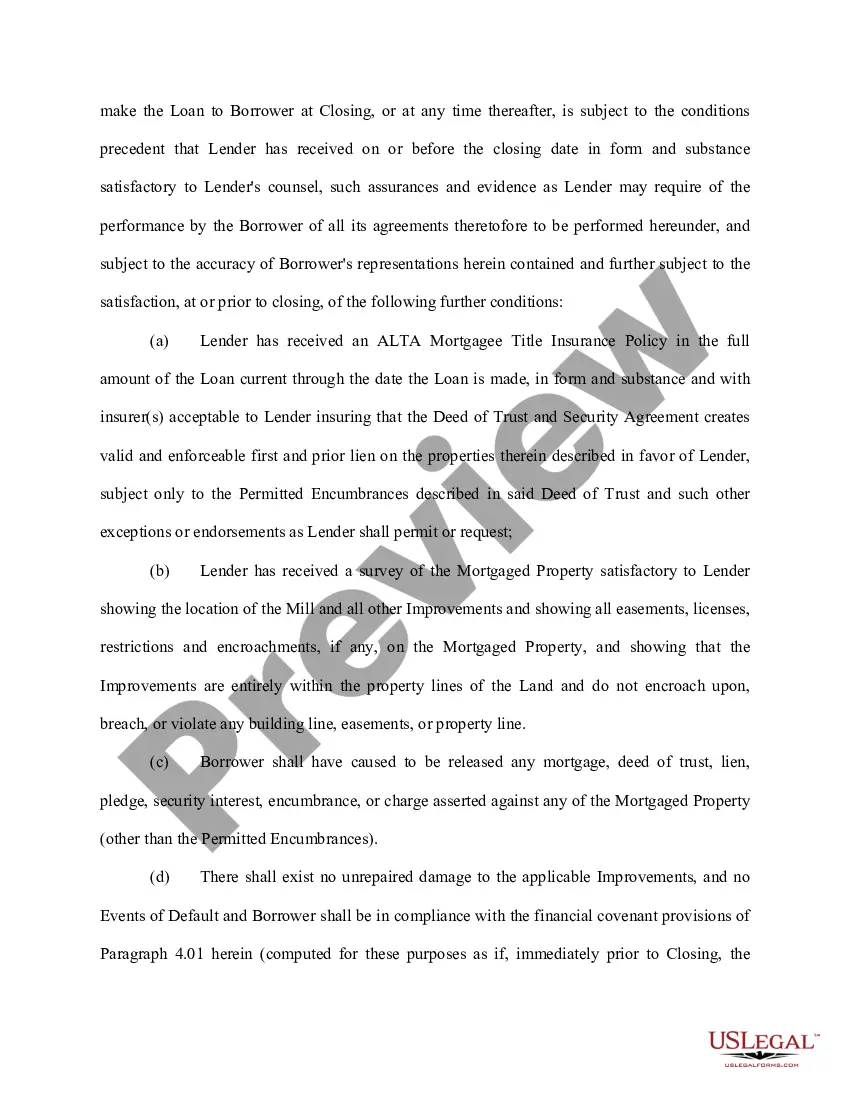

Wake North Carolina Loan Agreement for Employees is a legally binding contract between the employer and employee that outlines the details of a loan provided by the employer to the employee. This agreement ensures transparency and protects both parties involved. In Wake North Carolina, there are two main types of loan agreements for employees: 1. Promissory Note Agreement: This type of loan agreement is used when the employer provides a loan to the employee, and the employee promises to repay the borrowed amount within a specified time frame. The agreement includes the loan amount, interest rate (if applicable), repayment terms, and any penalties for late or missed payments. Both parties sign the agreement to create a legally binding contract. 2. Salary Advance Agreement: This type of loan agreement allows employees to request an advance on their salary. The employer provides a portion of the employee's future earnings in advance, which the employee agrees to repay in installments through payroll deductions. The agreement specifies the advance amount, repayment terms, and any applicable fees or interest charges. Both types of agreements include key provisions such as the purpose of the loan, the total amount borrowed, the repayment schedule, and any additional terms and conditions agreed upon by the employer and employee. It is essential for employers to clearly communicate the terms and expectations to avoid misunderstandings or disputes. When drafting a Wake North Carolina Loan Agreement for Employees, some relevant keywords to include might be: loan agreement, employee loan, promissory note, salary advance, repayment terms, interest rate, installments, payroll deductions, principal amount, late payment fees, signatures, and legal obligations.

Wake North Carolina Loan Agreement for Employees

Description

How to fill out Wake North Carolina Loan Agreement For Employees?

Whether you plan to start your company, enter into an agreement, apply for your ID update, or resolve family-related legal issues, you need to prepare specific paperwork corresponding to your local laws and regulations. Finding the right papers may take a lot of time and effort unless you use the US Legal Forms library.

The platform provides users with more than 85,000 expertly drafted and verified legal templates for any individual or business occasion. All files are grouped by state and area of use, so opting for a copy like Wake Loan Agreement for Employees is fast and easy.

The US Legal Forms website users only need to log in to their account and click the Download key next to the required template. If you are new to the service, it will take you a few additional steps to get the Wake Loan Agreement for Employees. Follow the guide below:

- Make sure the sample fulfills your personal needs and state law regulations.

- Look through the form description and check the Preview if available on the page.

- Use the search tab providing your state above to find another template.

- Click Buy Now to get the sample once you find the right one.

- Choose the subscription plan that suits you most to proceed.

- Sign in to your account and pay the service with a credit card or PayPal.

- Download the Wake Loan Agreement for Employees in the file format you require.

- Print the copy or fill it out and sign it electronically via an online editor to save time.

Documents provided by our website are multi-usable. Having an active subscription, you can access all of your earlier acquired paperwork at any moment in the My Forms tab of your profile. Stop wasting time on a constant search for up-to-date official documentation. Sign up for the US Legal Forms platform and keep your paperwork in order with the most comprehensive online form library!