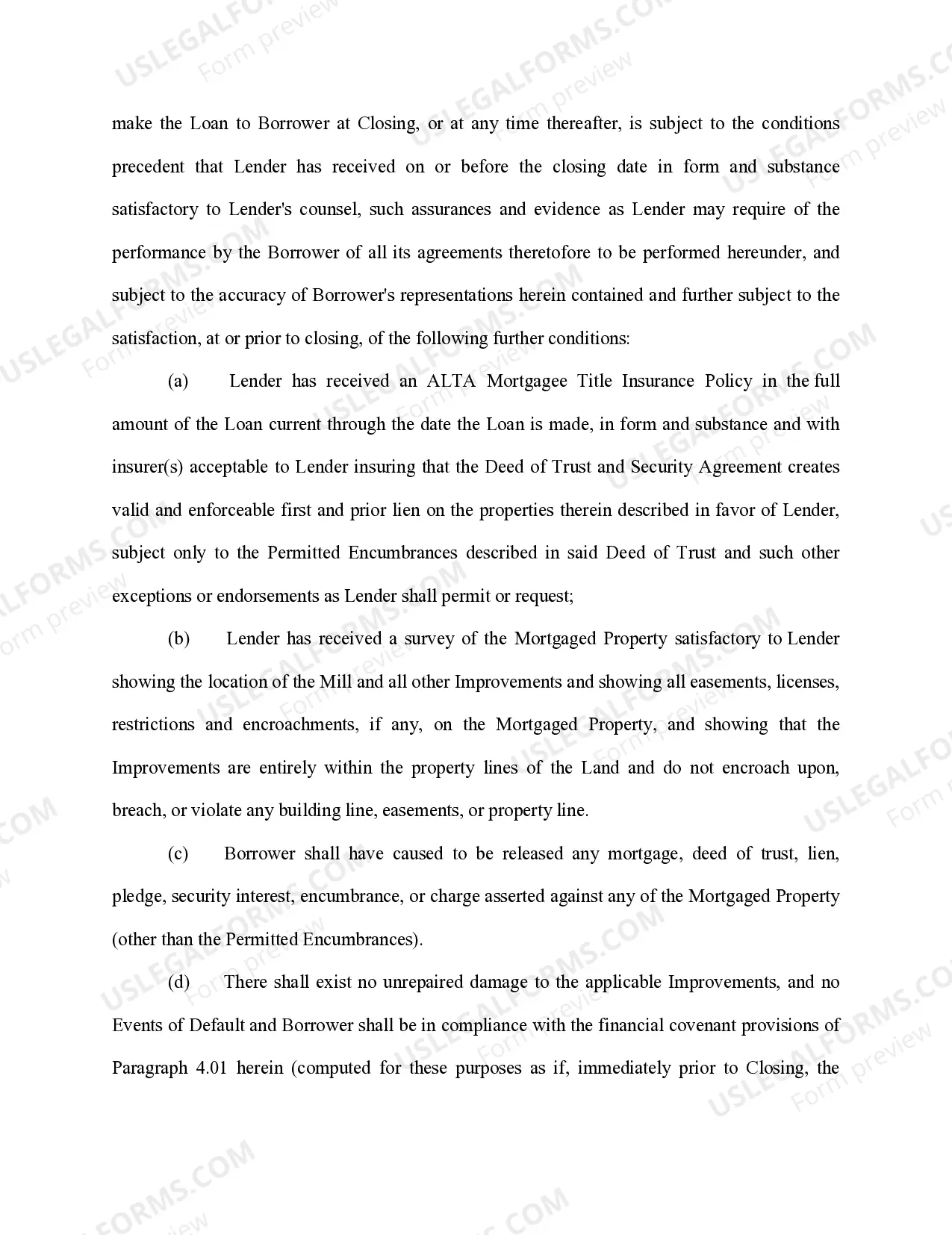

A San Diego California Loan Agreement for Personal Loan is a legally binding contract that outlines the terms and conditions of a personal loan between a lender and a borrower in San Diego, California. This agreement ensures that both parties are aware of their rights and responsibilities regarding the loan. The Loan Agreement contains various key elements, such as the loan amount, interest rate, repayment schedule, late payment penalties, and any collateral provided by the borrower. It also includes provisions on how disputes will be resolved and any legal jurisdiction specific to San Diego, California. There are different types of San Diego California Loan Agreements for Personal Loans, depending on the specific needs and requirements of the borrower and lender. Some common types include: 1. Traditional or Unsecured Personal Loan Agreement: This type of loan agreement does not require the borrower to provide any collateral. The lender relies solely on the borrower's creditworthiness to assess the risk of the loan. 2. Secured Personal Loan Agreement: In this case, the borrower provides collateral, such as a vehicle or property, which the lender can claim if the borrower defaults on the loan. This type of agreement offers more security to the lender and may result in lower interest rates for the borrower. 3. Co-Signed Personal Loan Agreement: A co-signed agreement involves a third party, typically with a stronger credit history, who guarantees the repayment of the loan. This provides additional security for the lender and may help borrowers with limited credit history or lower credit scores. 4. Payday Loan Agreement: Also known as a cash advance, this type of loan agreement allows borrowers to receive a short-term loan, typically due on their next payday. These loans often come with higher interest rates and fees. It is essential for both parties to carefully review and understand the terms and conditions of the San Diego California Loan Agreement for Personal Loan before signing. Seeking legal advice or consulting a financial professional can also be beneficial to ensure that the agreement is fair and in compliance with applicable laws and regulations.

San Diego California Loan Agreement for Personal Loan

Description

How to fill out San Diego California Loan Agreement For Personal Loan?

How much time does it usually take you to draft a legal document? Since every state has its laws and regulations for every life situation, locating a San Diego Loan Agreement for Personal Loan suiting all regional requirements can be tiring, and ordering it from a professional attorney is often pricey. Numerous web services offer the most popular state-specific templates for download, but using the US Legal Forms library is most beneficial.

US Legal Forms is the most comprehensive web collection of templates, gathered by states and areas of use. Apart from the San Diego Loan Agreement for Personal Loan, here you can find any specific form to run your business or individual deeds, complying with your county requirements. Professionals check all samples for their validity, so you can be certain to prepare your paperwork correctly.

Using the service is pretty easy. If you already have an account on the platform and your subscription is valid, you only need to log in, opt for the needed sample, and download it. You can get the document in your profile at any moment later on. Otherwise, if you are new to the platform, there will be some extra steps to complete before you get your San Diego Loan Agreement for Personal Loan:

- Check the content of the page you’re on.

- Read the description of the template or Preview it (if available).

- Search for another form using the corresponding option in the header.

- Click Buy Now when you’re certain in the chosen document.

- Choose the subscription plan that suits you most.

- Create an account on the platform or log in to proceed to payment options.

- Make a payment via PalPal or with your credit card.

- Switch the file format if needed.

- Click Download to save the San Diego Loan Agreement for Personal Loan.

- Print the sample or use any preferred online editor to complete it electronically.

No matter how many times you need to use the purchased template, you can find all the samples you’ve ever saved in your profile by opening the My Forms tab. Try it out!