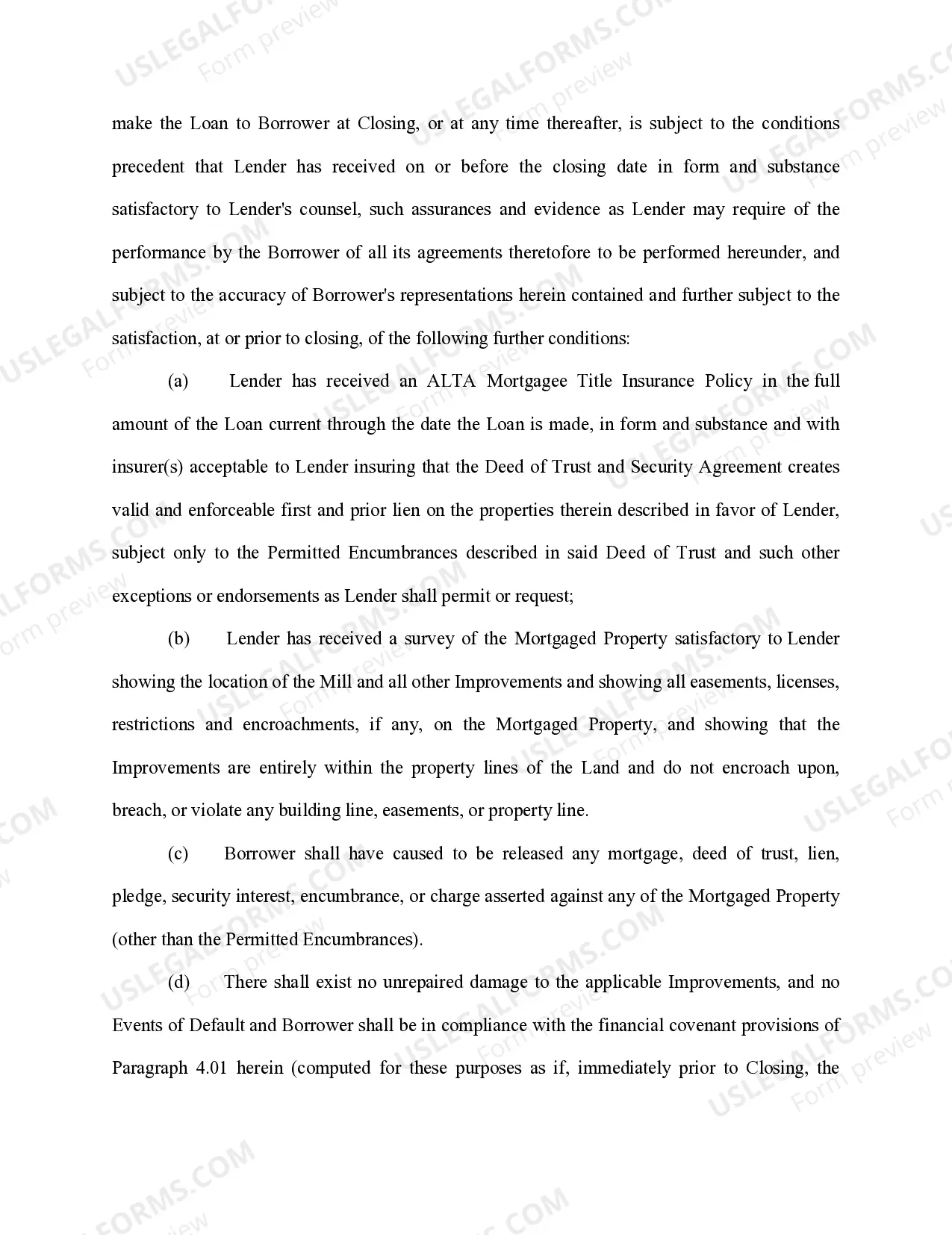

A Wake North Carolina Loan Agreement for Personal Loan is a legally binding document that outlines the terms and conditions between a lender and a borrower for a personal loan in the Wake County area of North Carolina. This agreement serves to protect both parties involved and ensures that all parties are aware of their rights and responsibilities. The Wake North Carolina Loan Agreement for Personal Loan typically includes essential details such as the loan amount, interest rate, repayment schedule, late payment fees, and any additional charges or penalties that may apply. It also includes clauses related to default, loan termination, and the consequences of non-payment. Both the borrower and the lender must thoroughly review and understand all the terms before signing this agreement. Different types of Wake North Carolina Loan Agreements for Personal Loans can vary based on factors such as loan amounts, interest rates, repayment plans, and collateral requirements. Here are some of the common loan types: 1. Secured Personal Loan: This loan requires the borrower to pledge collateral, such as a car or property, as a form of security. If the borrower defaults on the loan, the lender can seize the collateral to recover their losses. 2. Unsecured Personal Loan: Unlike secured loans, unsecured personal loans do not require collateral. They typically have higher interest rates as they pose a higher risk to the lender. 3. Fixed-Rate Personal Loan: In this type of loan agreement, the interest rate remains fixed throughout the loan term, offering predictable monthly payments. 4. Variable-Rate Personal Loan: With a variable-rate loan agreement, the interest rate can change over time based on market conditions. This can result in fluctuating monthly payments. 5. Payday Loan Agreement: Payday loans are short-term loans typically due on the borrower's next payday. They are designed to provide quick cash to cover immediate financial needs but often come with high interest rates and fees. 6. Debt Consolidation Loan Agreement: This type of agreement allows borrowers to combine multiple existing debts into a single loan, usually with a lower interest rate. It helps simplify repayment, reduce monthly payments, and potentially save on interest charges. Regardless of the type of Wake North Carolina Loan Agreement for Personal Loan, it is crucial for both parties to carefully review and understand all the terms and conditions stated in the agreement. Seeking legal advice or consulting a financial professional can also help ensure a smooth borrowing experience.

Wake North Carolina Loan Agreement for Personal Loan

Description

How to fill out Wake North Carolina Loan Agreement For Personal Loan?

How much time does it normally take you to draft a legal document? Because every state has its laws and regulations for every life situation, locating a Wake Loan Agreement for Personal Loan meeting all regional requirements can be stressful, and ordering it from a professional attorney is often costly. Numerous online services offer the most common state-specific templates for download, but using the US Legal Forms library is most beneficial.

US Legal Forms is the most extensive online collection of templates, gathered by states and areas of use. In addition to the Wake Loan Agreement for Personal Loan, here you can get any specific form to run your business or individual affairs, complying with your regional requirements. Experts verify all samples for their validity, so you can be sure to prepare your paperwork correctly.

Using the service is fairly easy. If you already have an account on the platform and your subscription is valid, you only need to log in, select the required form, and download it. You can get the document in your profile at any moment later on. Otherwise, if you are new to the platform, there will be a few more steps to complete before you obtain your Wake Loan Agreement for Personal Loan:

- Examine the content of the page you’re on.

- Read the description of the sample or Preview it (if available).

- Search for another form using the related option in the header.

- Click Buy Now once you’re certain in the selected document.

- Decide on the subscription plan that suits you most.

- Sign up for an account on the platform or log in to proceed to payment options.

- Pay via PalPal or with your credit card.

- Switch the file format if necessary.

- Click Download to save the Wake Loan Agreement for Personal Loan.

- Print the doc or use any preferred online editor to fill it out electronically.

No matter how many times you need to use the purchased template, you can find all the samples you’ve ever downloaded in your profile by opening the My Forms tab. Give it a try!