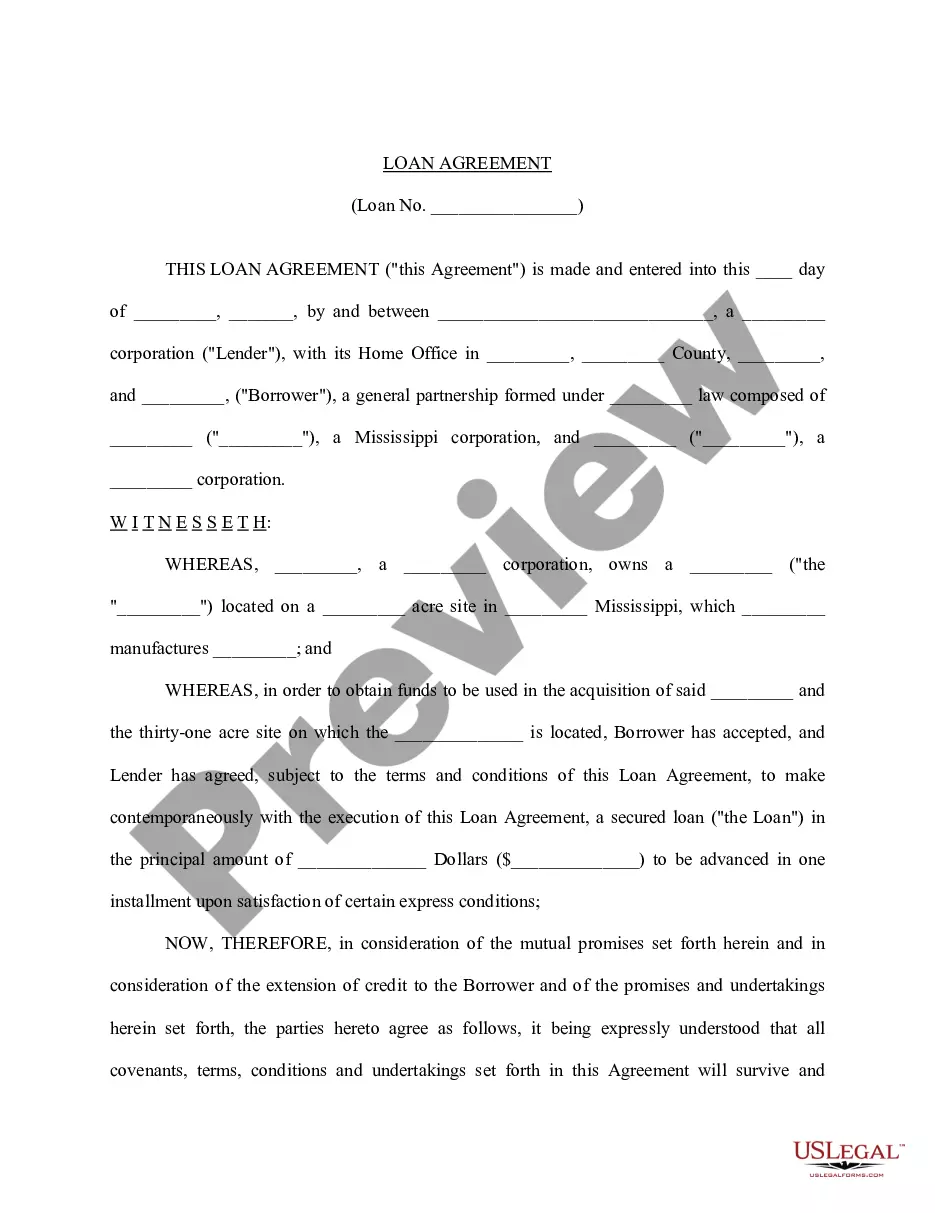

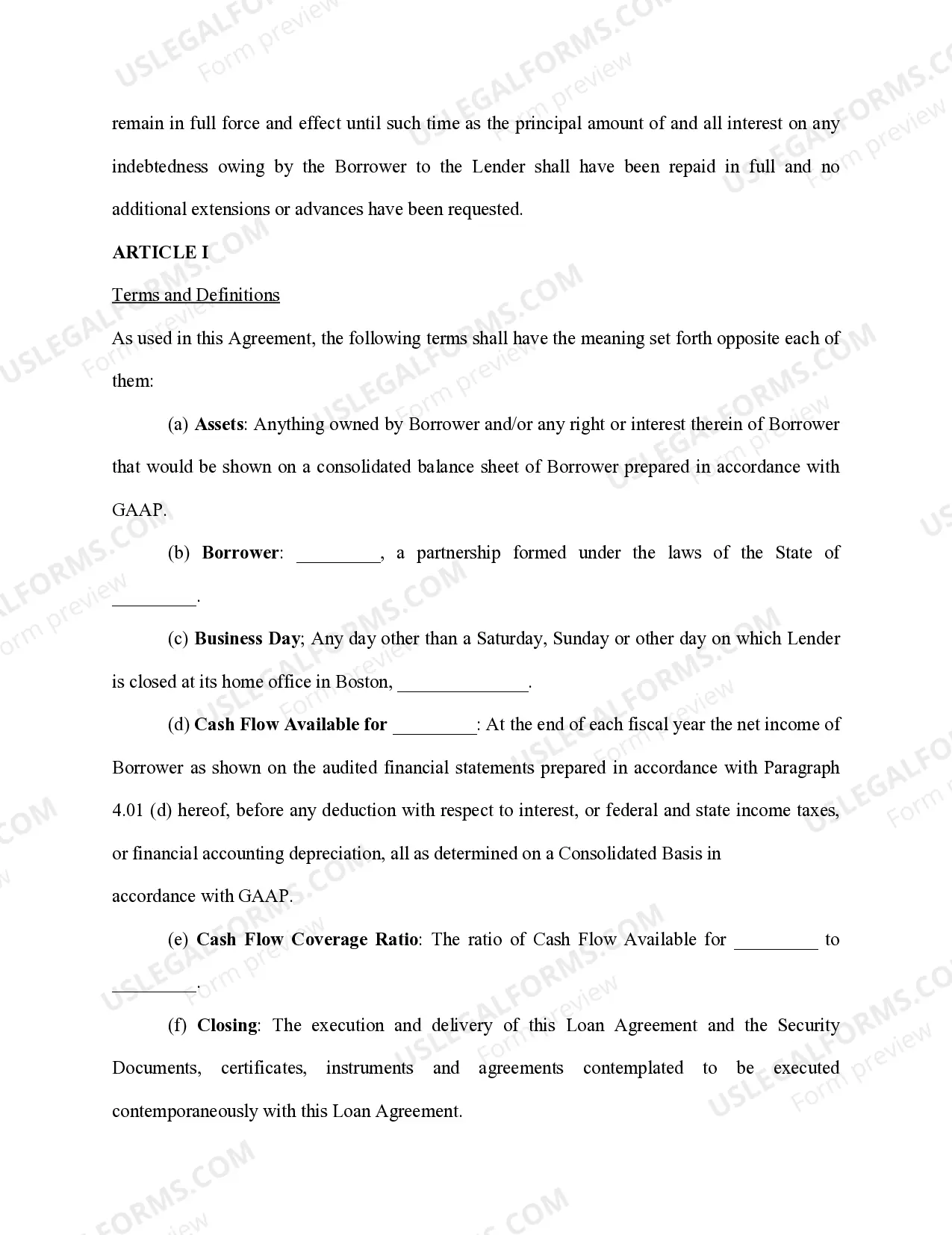

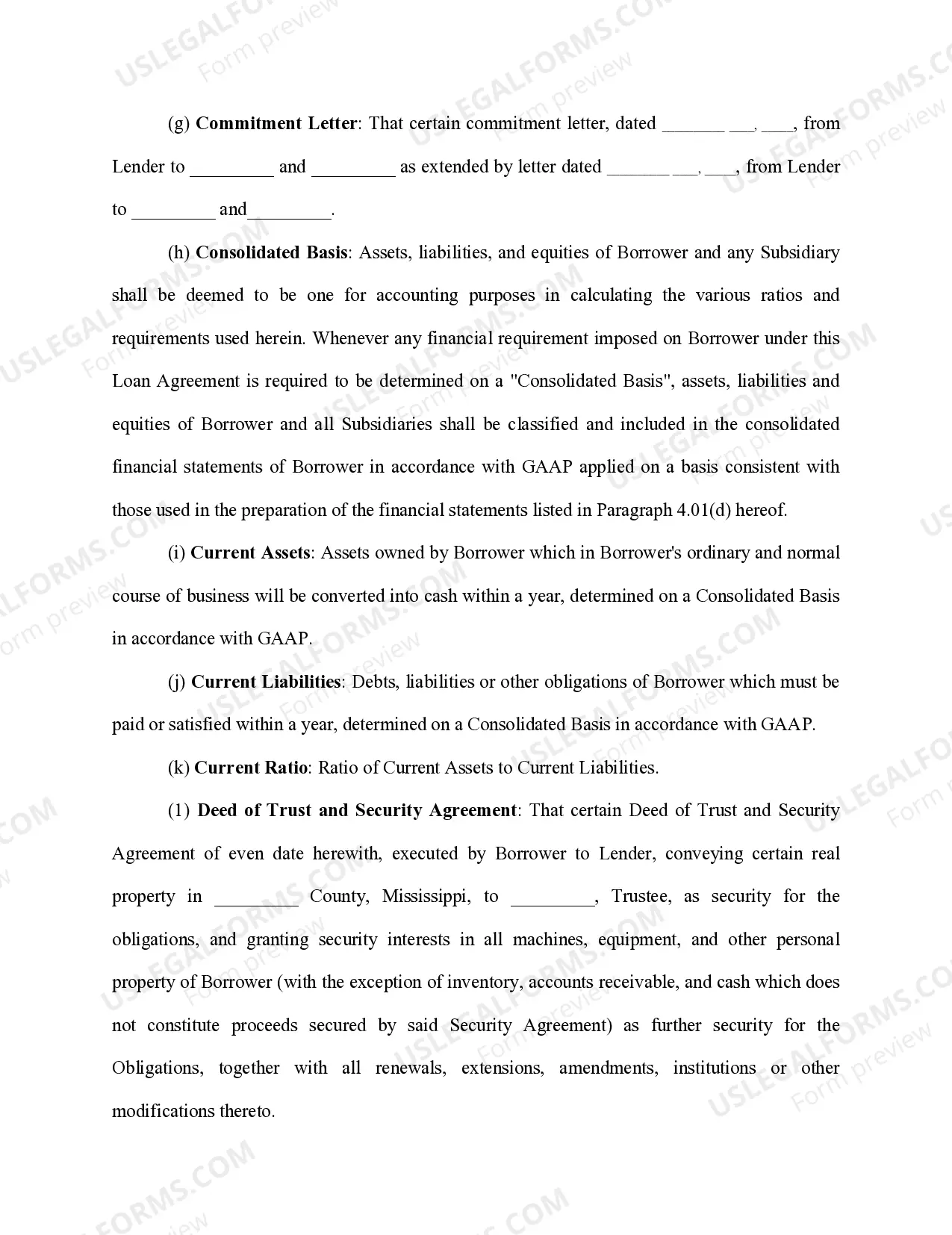

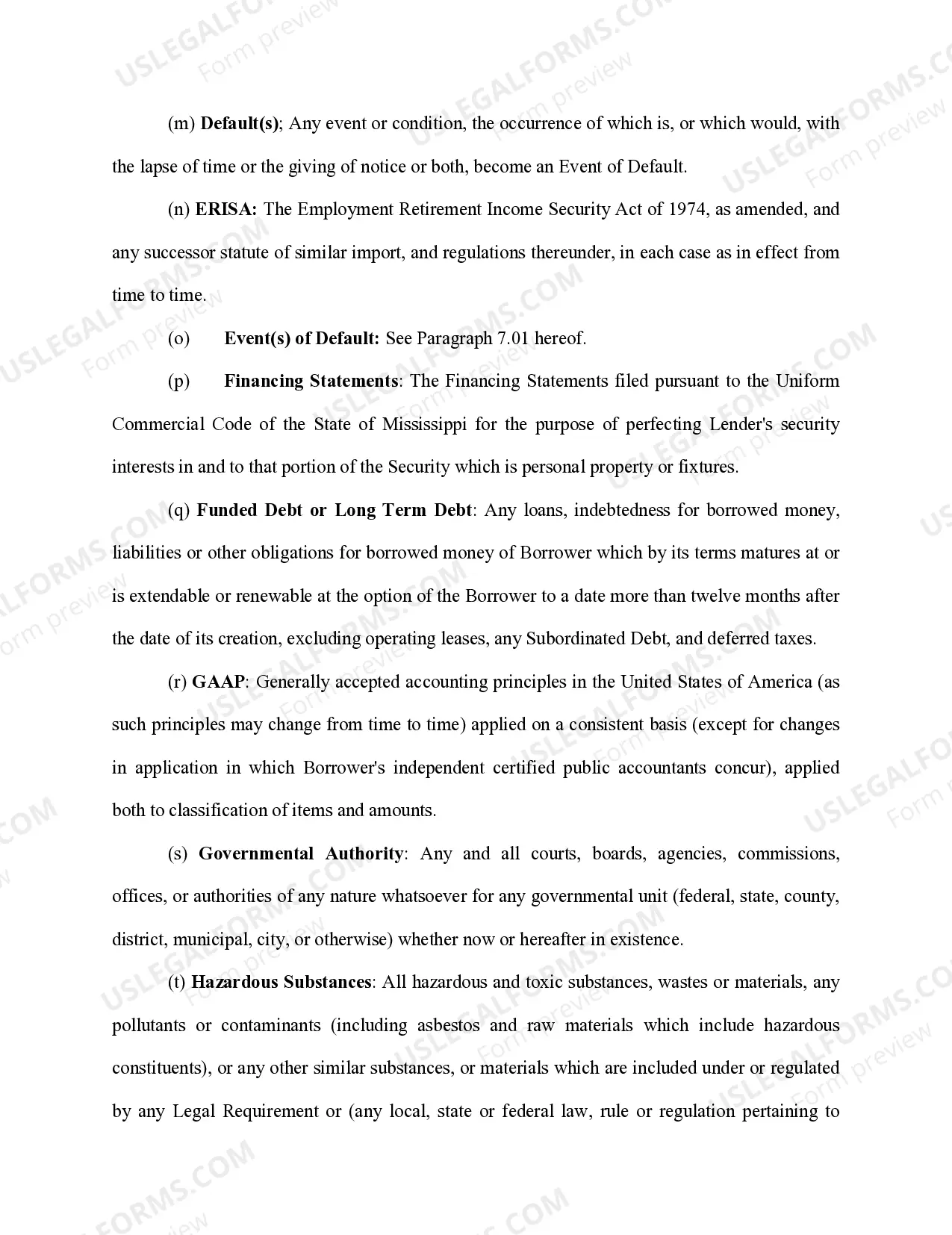

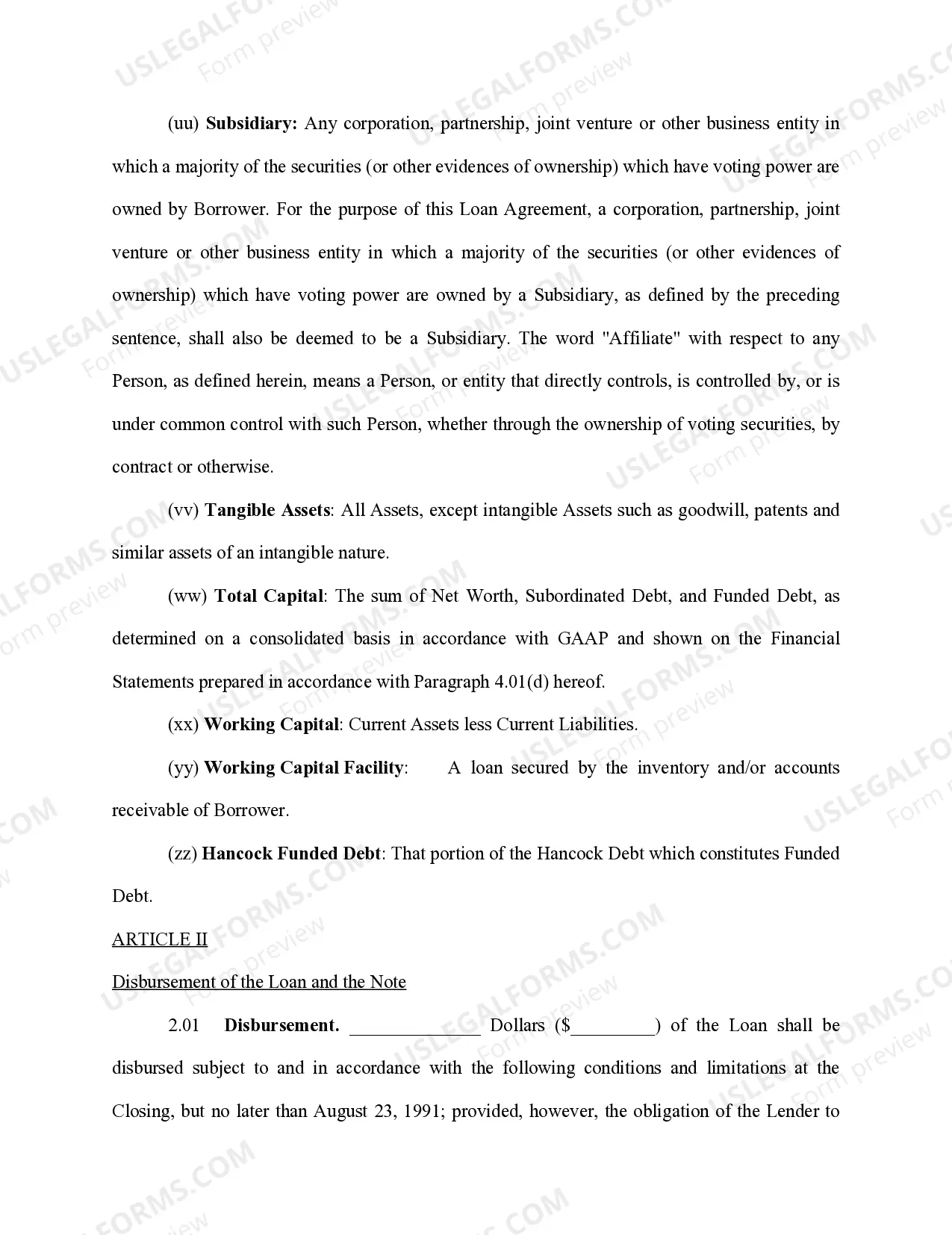

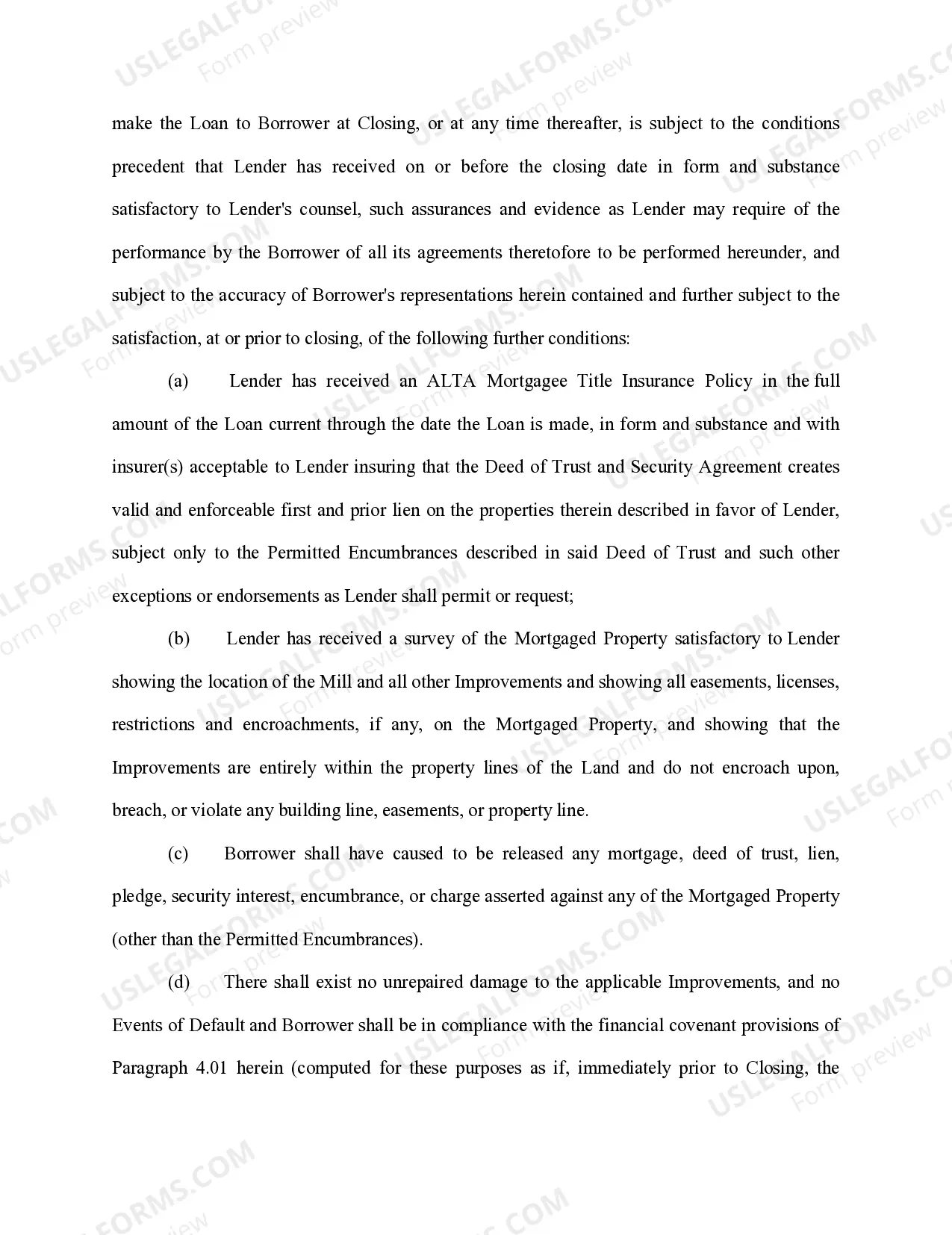

Contra Costa California Loan Agreement for Friends is a legal document that outlines the terms and conditions of a loan between individuals who have a friendly or personal relationship. This agreement ensures that both parties involved are protected by clearly stating the terms of the loan, including repayment terms, interest rate (if applicable), and consequences for defaulting on the loan. In Contra Costa, California, there are two main types of Loan Agreements for Friends: 1. Secured Loan Agreement: This type of loan agreement involves collateral being provided by the borrower to secure the loan. Collateral can be any valuable asset, such as real estate, vehicles, or other high-value possessions. The collateral acts as security for the lender in case the borrower fails to repay the loan. 2. Unsecured Loan Agreement: Unlike a secured loan agreement, an unsecured loan agreement does not require any collateral from the borrower. This means that the lender relies solely on the borrower's promise to repay the loan based on the agreed terms. However, in unsecured agreements, lenders often charge higher interest rates to compensate for the increased risk. The Contra Costa California Loan Agreement for Friends typically includes the following key elements: 1. Loan Amount: Clearly states the initial amount being borrowed. 2. Interest Rate: If applicable, it outlines the interest rate charged on the loan, usually presented as an annual percentage rate (APR). This helps to determine the cost of borrowing over time. 3. Repayment Terms: Specifies the terms for repayment, including the frequency, amount, and duration of repayments. It may also detail the method of repayment, such as cash, check, or direct deposit. 4. Late Payment Penalties: Outlines the penalties or fees imposed on the borrower for late or missed payments. This section provides clarity on the consequences of failing to adhere to the agreed repayment schedule. 5. Default Conditions: Specifies the conditions under which the loan will be considered in default, such as multiple missed payments or failure to meet other agreed-upon terms. It may also outline potential legal actions that may be taken in case of default. 6. Signatures: Both parties to the agreement, i.e., the lender and the borrower, must sign the document to indicate their acceptance and agreement to the terms outlined. Contra Costa California Loan Agreement for Friends is designed to protect the interests of both parties involved in a personal loan transaction. It is crucial to consult with a legal professional or use a reputable online template to ensure the agreement is compliant with California laws and properly addresses the specific details of the loan.

Contra Costa California Loan Agreement for Friends

Description

How to fill out Contra Costa California Loan Agreement For Friends?

Whether you intend to start your company, enter into a contract, apply for your ID renewal, or resolve family-related legal issues, you must prepare specific paperwork meeting your local laws and regulations. Finding the right papers may take a lot of time and effort unless you use the US Legal Forms library.

The service provides users with more than 85,000 expertly drafted and verified legal templates for any individual or business occasion. All files are collected by state and area of use, so picking a copy like Contra Costa Loan Agreement for Friends is fast and easy.

The US Legal Forms website users only need to log in to their account and click the Download button next to the required form. If you are new to the service, it will take you several additional steps to obtain the Contra Costa Loan Agreement for Friends. Adhere to the instructions below:

- Make sure the sample fulfills your individual needs and state law regulations.

- Read the form description and check the Preview if available on the page.

- Utilize the search tab specifying your state above to locate another template.

- Click Buy Now to get the file when you find the right one.

- Select the subscription plan that suits you most to continue.

- Log in to your account and pay the service with a credit card or PayPal.

- Download the Contra Costa Loan Agreement for Friends in the file format you require.

- Print the copy or complete it and sign it electronically via an online editor to save time.

Documents provided by our website are multi-usable. Having an active subscription, you are able to access all of your previously purchased paperwork at any time in the My Forms tab of your profile. Stop wasting time on a endless search for up-to-date formal documents. Sign up for the US Legal Forms platform and keep your paperwork in order with the most extensive online form collection!