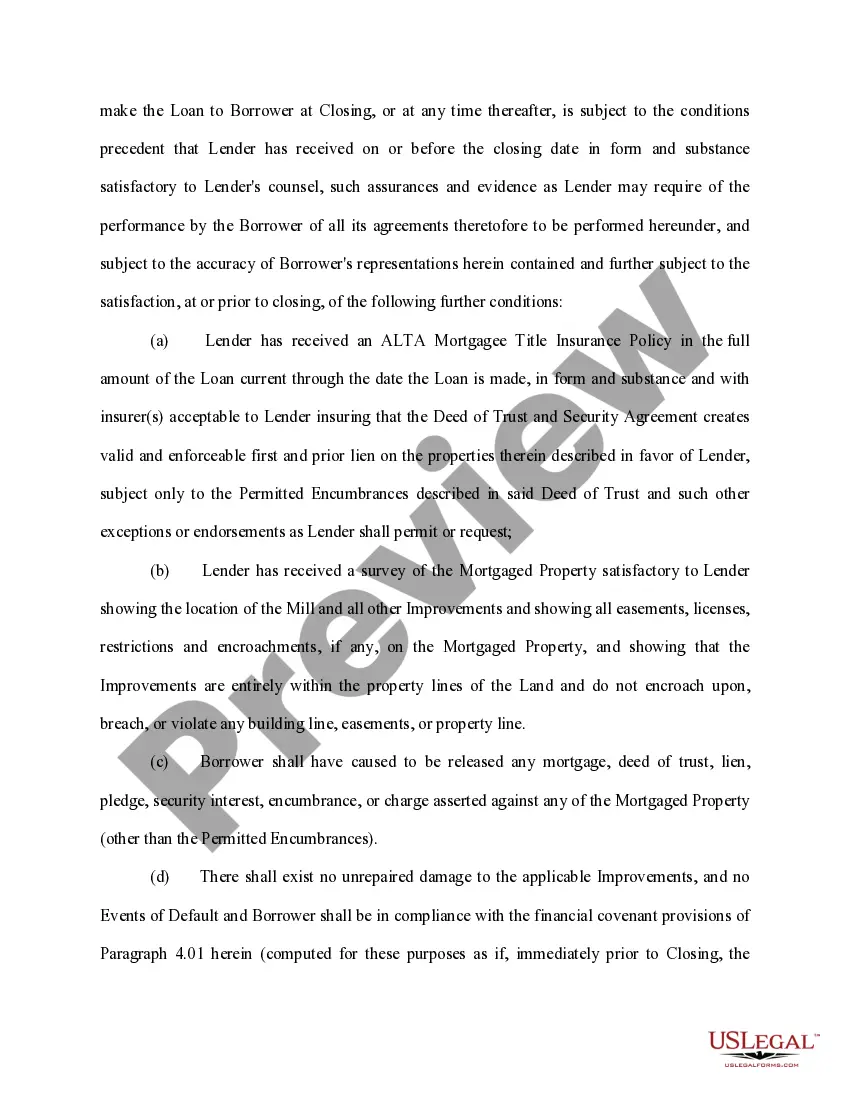

The Clark Nevada Loan Agreement for Vehicle is a legal document that outlines the terms and conditions for borrowing money for purchasing a vehicle in the Clark County, Nevada region. This agreement serves as a binding contract between the borrower and the lender, providing clarity and protection for both parties involved in the transaction. The loan agreement includes several essential components such as: 1. Parties involved: It clearly identifies the borrower, the individual or entity seeking the loan, and the lender, the entity or person providing the funds. 2. Loan amount and interest rate: The agreement specifies the exact amount of money being borrowed and the agreed-upon interest rate that the borrower must pay on the loan, determining the total repayment amount. 3. Repayment terms: This section outlines how the borrower is required to repay the loan. It typically includes details about the payment frequency, due dates, and any late payment penalties that may apply. 4. Collateral: The loan agreement may require the borrower to provide collateral in the form of the vehicle itself. This means that if the borrower fails to fulfill the repayment terms, the lender has the right to seize the vehicle as compensation. 5. Default and consequences: In case of default, when the borrower fails to fulfill their obligations, the agreement defines the actions that the lender can take. This may involve repossession of the vehicle, legal action, or additional fees and charges. Different types of loan agreements for vehicles in Clark Nevada may vary based on specific factors or parties involved. Some common variations include: 1. Private Party Loan Agreement: This type of loan agreement occurs when the borrower borrows money directly from an individual, such as a family member or friend, rather than a financial institution or dealership. 2. Dealer Financing Loan Agreement: In this case, the loan agreement is entered into with a dealership or car financing company. The loan may be secured through the dealership itself or by an external financial institution. 3. Lease Agreement with Option to Purchase: This type of agreement allows the borrower to lease a vehicle with the option to buy it at the end of the lease term. The agreement establishes the terms for leasing as well as the repurchase option. It is crucial for both borrowers and lenders to carefully read and understand the terms of the Clark Nevada Loan Agreement for Vehicle before signing it. Seeking legal advice to ensure compliance with state laws and protection of rights is highly recommended.

Clark Nevada Loan Agreement for Vehicle

Description

How to fill out Clark Nevada Loan Agreement For Vehicle?

How much time does it usually take you to draft a legal document? Considering that every state has its laws and regulations for every life scenario, finding a Clark Loan Agreement for Vehicle suiting all local requirements can be exhausting, and ordering it from a professional attorney is often expensive. Many online services offer the most common state-specific templates for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most comprehensive online collection of templates, collected by states and areas of use. Apart from the Clark Loan Agreement for Vehicle, here you can get any specific document to run your business or personal affairs, complying with your regional requirements. Specialists check all samples for their validity, so you can be certain to prepare your documentation properly.

Using the service is pretty simple. If you already have an account on the platform and your subscription is valid, you only need to log in, pick the required sample, and download it. You can pick the file in your profile at any time later on. Otherwise, if you are new to the website, there will be a few more actions to complete before you get your Clark Loan Agreement for Vehicle:

- Check the content of the page you’re on.

- Read the description of the sample or Preview it (if available).

- Search for another document utilizing the corresponding option in the header.

- Click Buy Now when you’re certain in the chosen file.

- Choose the subscription plan that suits you most.

- Register for an account on the platform or log in to proceed to payment options.

- Pay via PalPal or with your credit card.

- Switch the file format if needed.

- Click Download to save the Clark Loan Agreement for Vehicle.

- Print the doc or use any preferred online editor to complete it electronically.

No matter how many times you need to use the acquired document, you can find all the files you’ve ever saved in your profile by opening the My Forms tab. Try it out!