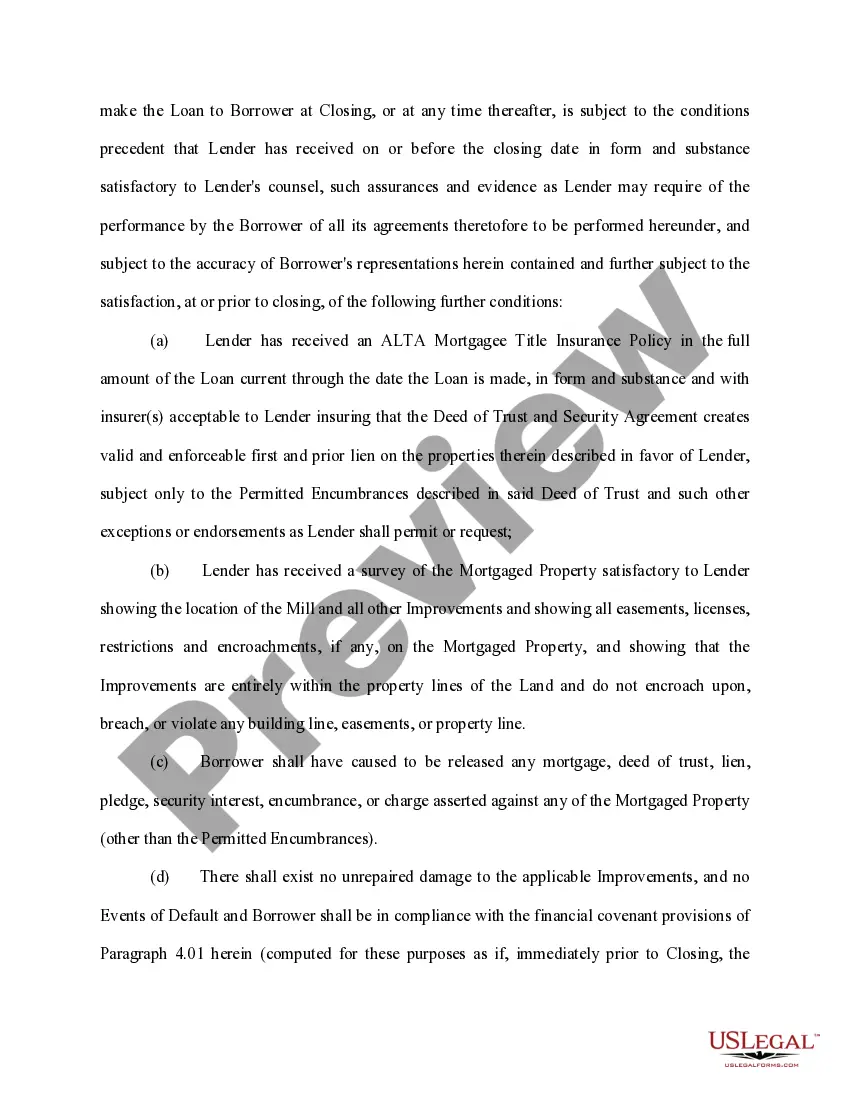

A Loan Agreement for Vehicle in San Jose, California is a legally binding contract between a lender and a borrower, outlining the terms and conditions of a loan provided for the purchase of a vehicle. This agreement ensures that both parties understand their rights, obligations, and responsibilities throughout the loan process, protecting their interests and avoiding misunderstandings. The San Jose Loan Agreement for Vehicle typically includes important details such as the names and addresses of the lender (often a financial institution) and borrower, the description of the vehicle being financed, the loan amount, interest rate, repayment schedule, and any additional fees or charges. It may also cover insurance requirements, default provisions, and penalty clauses in case of non-payment or breach of contract. In San Jose, California, there are various types of Loan Agreements for Vehicles, each catering to specific needs or circumstances: 1. New Car Loan Agreement: This type of loan agreement is used when purchasing a brand-new vehicle from a dealer. It may have fixed or variable interest rates depending on the lender's terms. 2. Used Car Loan Agreement: When buying a pre-owned vehicle, a used car loan agreement is executed. Similar to a new car loan, the interest rates for used vehicles can be fixed or variable, depending on several factors, including the vehicle's age and condition. 3. Lease Agreement: Sometimes referred to as a vehicle lease agreement, this type of loan arrangement allows the borrower to use a vehicle for a specific period, typically 2-4 years, in exchange for fixed monthly payments. At the end of the lease term, the borrower may have the option to purchase the vehicle or return it to the lessor. 4. Refinance Agreement: In cases where the borrower wants to replace their existing loan with a new one with different terms, a refinancing agreement comes into play. It allows the borrower to obtain better interest rates, change the loan duration, or modify other terms to suit their changing financial situation. Regardless of the Loan Agreement for Vehicle in San Jose, California, it is crucial for both the lender and borrower to carefully review the terms and conditions, seek legal advice if necessary, and ensure that they fully comprehend their obligations before signing the contract. This protects them from any potential disputes or issues that may arise during the loan tenure, providing them with a clear understanding of their rights and responsibilities.

San Jose California Loan Agreement for Vehicle

Description

How to fill out San Jose California Loan Agreement For Vehicle?

Creating paperwork, like San Jose Loan Agreement for Vehicle, to manage your legal matters is a difficult and time-consumming process. Many circumstances require an attorney’s involvement, which also makes this task expensive. Nevertheless, you can consider your legal matters into your own hands and handle them yourself. US Legal Forms is here to save the day. Our website features over 85,000 legal forms crafted for different scenarios and life situations. We ensure each form is compliant with the regulations of each state, so you don’t have to be concerned about potential legal pitfalls associated with compliance.

If you're already aware of our services and have a subscription with US, you know how straightforward it is to get the San Jose Loan Agreement for Vehicle template. Go ahead and log in to your account, download the template, and customize it to your requirements. Have you lost your form? Don’t worry. You can find it in the My Forms tab in your account - on desktop or mobile.

The onboarding process of new users is just as easy! Here’s what you need to do before getting San Jose Loan Agreement for Vehicle:

- Ensure that your template is specific to your state/county since the rules for writing legal paperwork may differ from one state another.

- Find out more about the form by previewing it or reading a quick description. If the San Jose Loan Agreement for Vehicle isn’t something you were hoping to find, then take advantage of the search bar in the header to find another one.

- Log in or create an account to begin utilizing our service and get the form.

- Everything looks great on your side? Hit the Buy now button and choose the subscription plan.

- Select the payment gateway and type in your payment details.

- Your template is all set. You can try and download it.

It’s an easy task to find and buy the appropriate template with US Legal Forms. Thousands of organizations and individuals are already taking advantage of our extensive library. Sign up for it now if you want to check what other perks you can get with US Legal Forms!