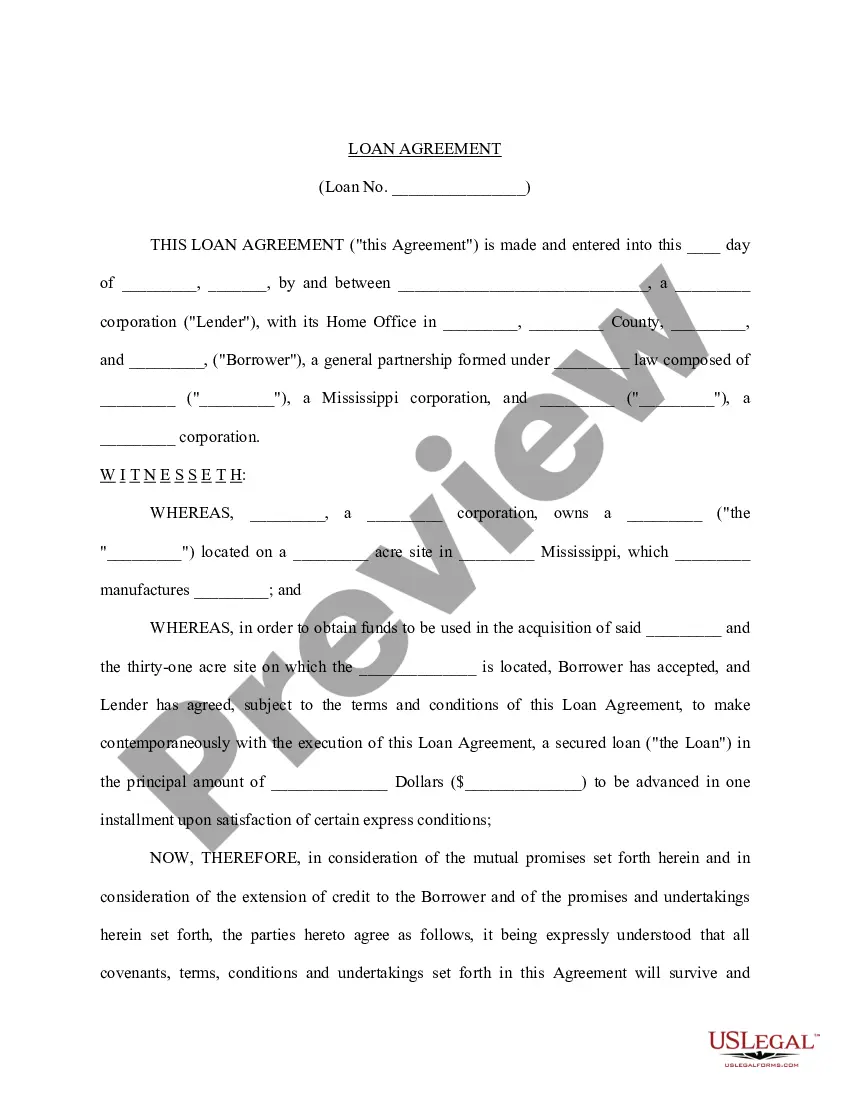

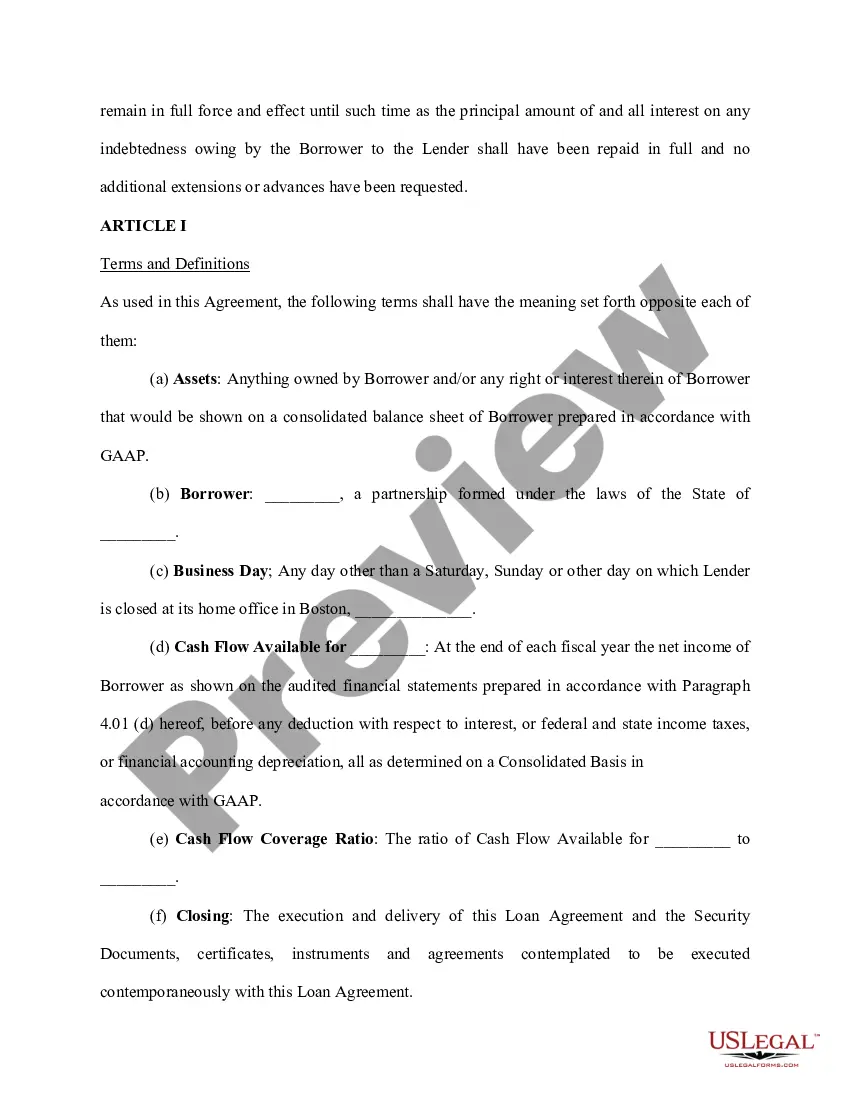

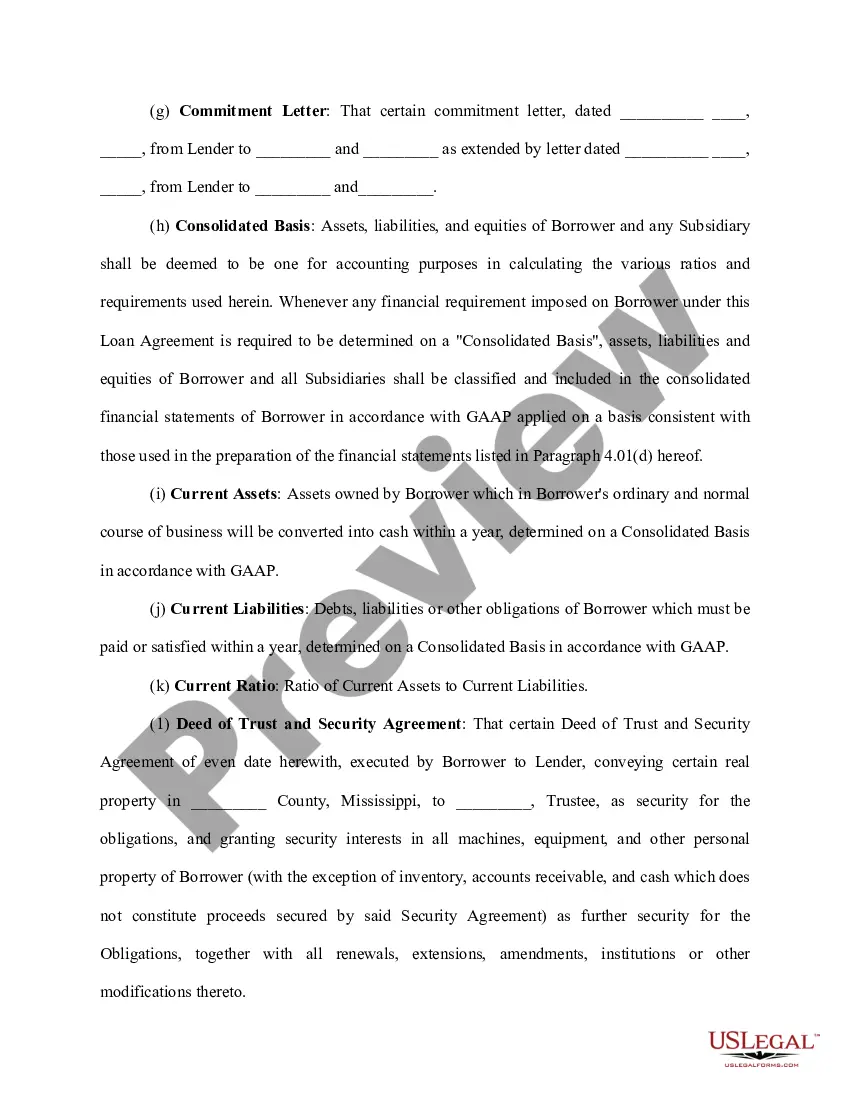

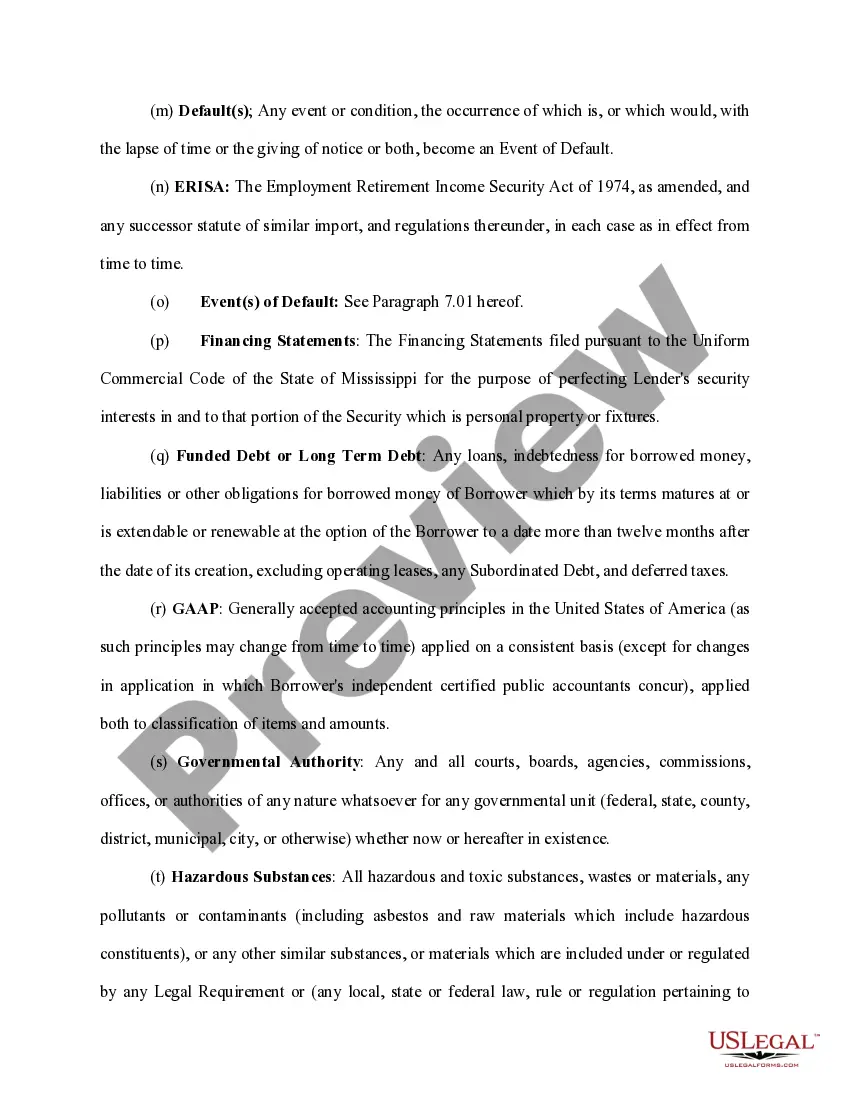

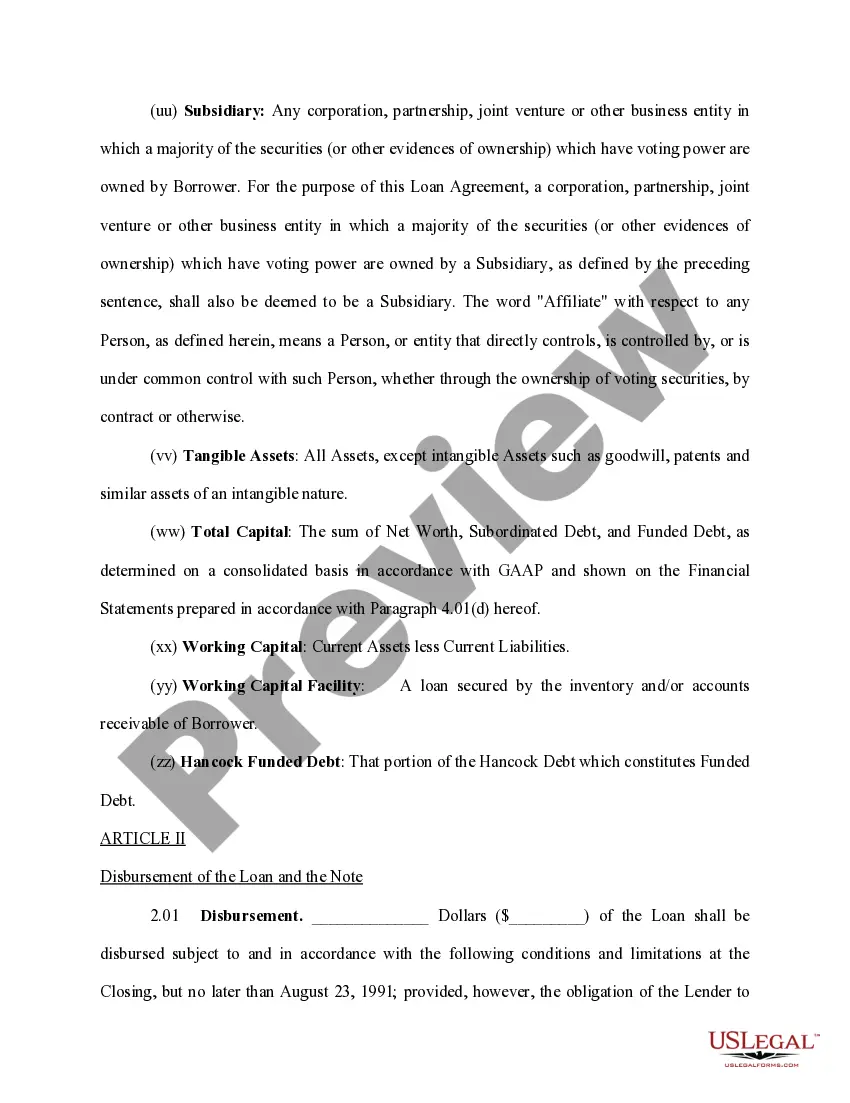

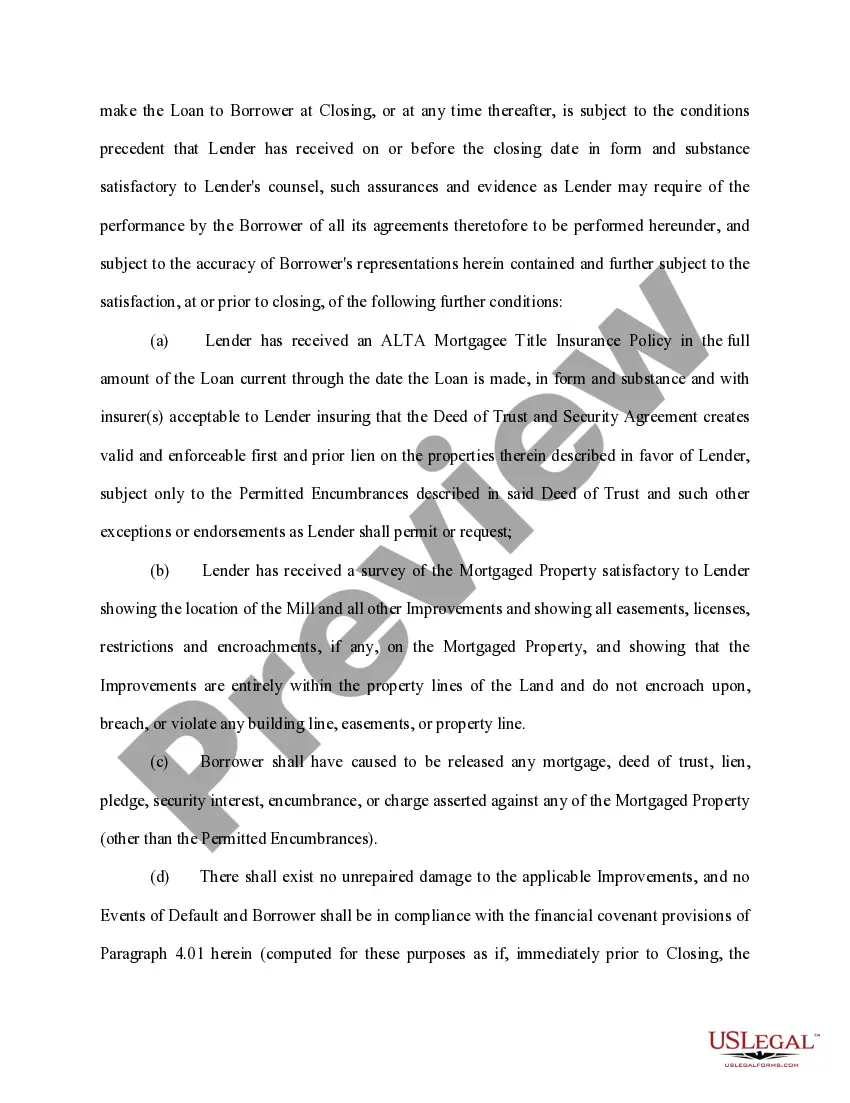

Alameda California Loan Agreement for Car is a legally binding document created between a lender and a borrower for financing the purchase of a vehicle in Alameda, California. This agreement outlines the terms and conditions of the loan, including repayment terms, interest rates, and rights and responsibilities of both parties involved. The Loan Agreement for Car in Alameda, California specifies the loan amount, which is typically calculated by deducting the down payment from the total purchase price of the vehicle. The agreement may also include provisions for additional charges like taxes, insurance, and any other fees related to the loan. The loan agreement will define the repayment schedule, which usually includes the principal amount borrowed and the interest accrued over the loan term. Common payment terms comprise monthly installments, but they can also be weekly or bi-weekly, depending on the agreement. The interest rate stated in the agreement is determined by various factors, such as credit score, loan term, and market conditions. Regarding the types of Alameda California Loan Agreements for Car, several options cater to different circumstances: 1. New Car Loan Agreement: This type of agreement is specifically tailored for borrowers purchasing a brand-new vehicle from a dealership or manufacturer. 2. Used Car Loan Agreement: Used Car Loan Agreement is designed for borrowers looking to finance the purchase of a pre-owned vehicle. The terms of this agreement generally differ as compared to the new car loan agreement. 3. Refinancing Car Loan Agreement: This type of agreement allows borrowers to replace their existing car loan with a new loan that offers more favorable terms, such as lower interest rates or extended loan duration. 4. Lease Agreement: Although not technically a loan, a car lease agreement provides customers with the option to "rent" a vehicle for a specific period while making monthly payments. At the end of the lease term, the lessee may have the option to purchase the vehicle. It is crucial for both the lender and the borrower to fully understand the terms and conditions stated in the Alameda California Loan Agreement for Car before signing. This agreement ensures transparency, protects the rights of both parties, and provides a clear framework for loan repayment.

Alameda California Loan Agreement for Car

Description

How to fill out Alameda California Loan Agreement For Car?

Drafting documents for the business or individual needs is always a huge responsibility. When creating a contract, a public service request, or a power of attorney, it's crucial to take into account all federal and state laws and regulations of the particular area. However, small counties and even cities also have legislative procedures that you need to consider. All these details make it tense and time-consuming to create Alameda Loan Agreement for Car without professional help.

It's possible to avoid spending money on attorneys drafting your paperwork and create a legally valid Alameda Loan Agreement for Car by yourself, using the US Legal Forms online library. It is the biggest online collection of state-specific legal documents that are professionally verified, so you can be certain of their validity when choosing a sample for your county. Previously subscribed users only need to log in to their accounts to save the necessary form.

If you still don't have a subscription, follow the step-by-step guide below to obtain the Alameda Loan Agreement for Car:

- Examine the page you've opened and check if it has the sample you require.

- To do so, use the form description and preview if these options are available.

- To find the one that meets your requirements, utilize the search tab in the page header.

- Double-check that the sample complies with juridical criteria and click Buy Now.

- Pick the subscription plan, then sign in or create an account with the US Legal Forms.

- Utilize your credit card or PayPal account to pay for your subscription.

- Download the selected file in the preferred format, print it, or complete it electronically.

The great thing about the US Legal Forms library is that all the paperwork you've ever acquired never gets lost - you can access it in your profile within the My Forms tab at any moment. Join the platform and quickly obtain verified legal templates for any use case with just a few clicks!