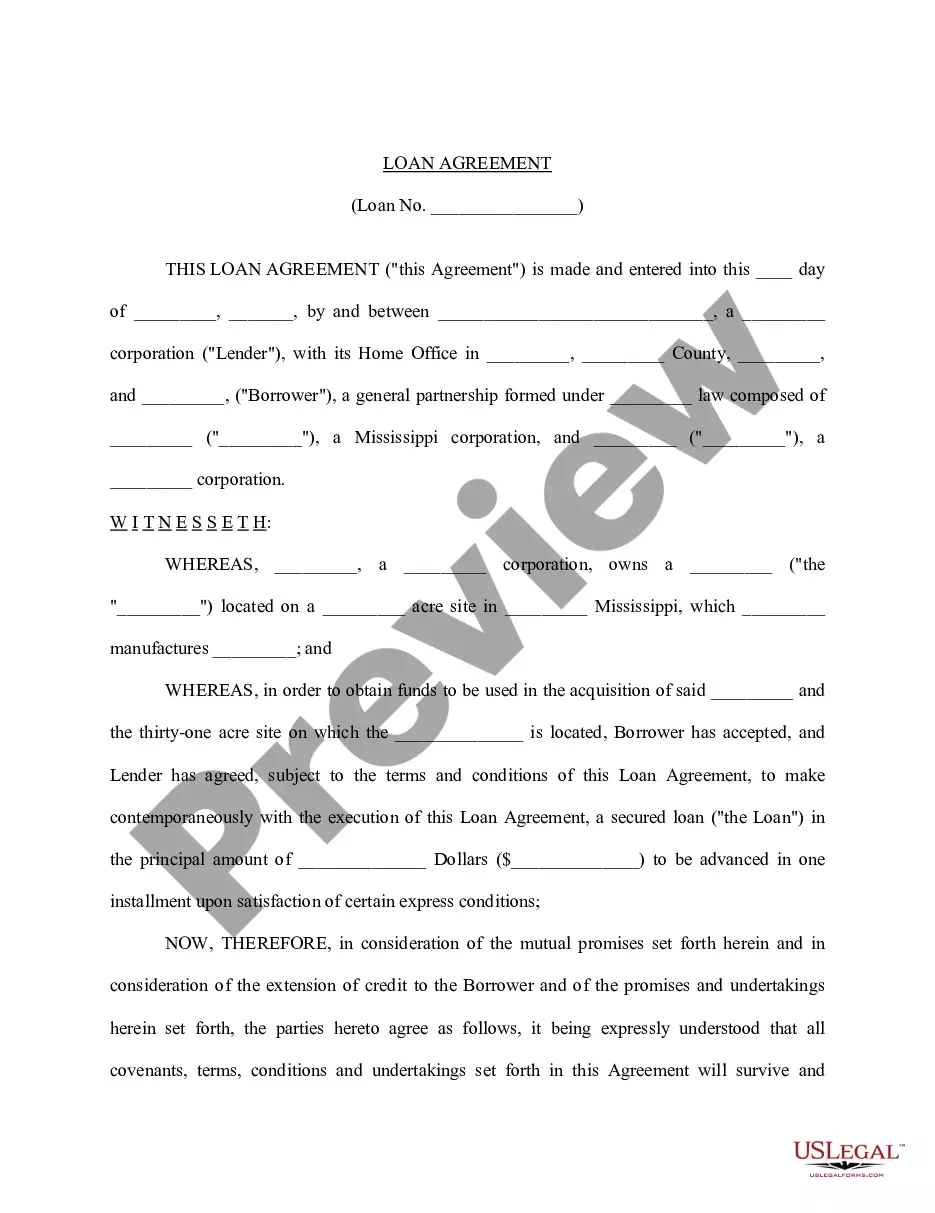

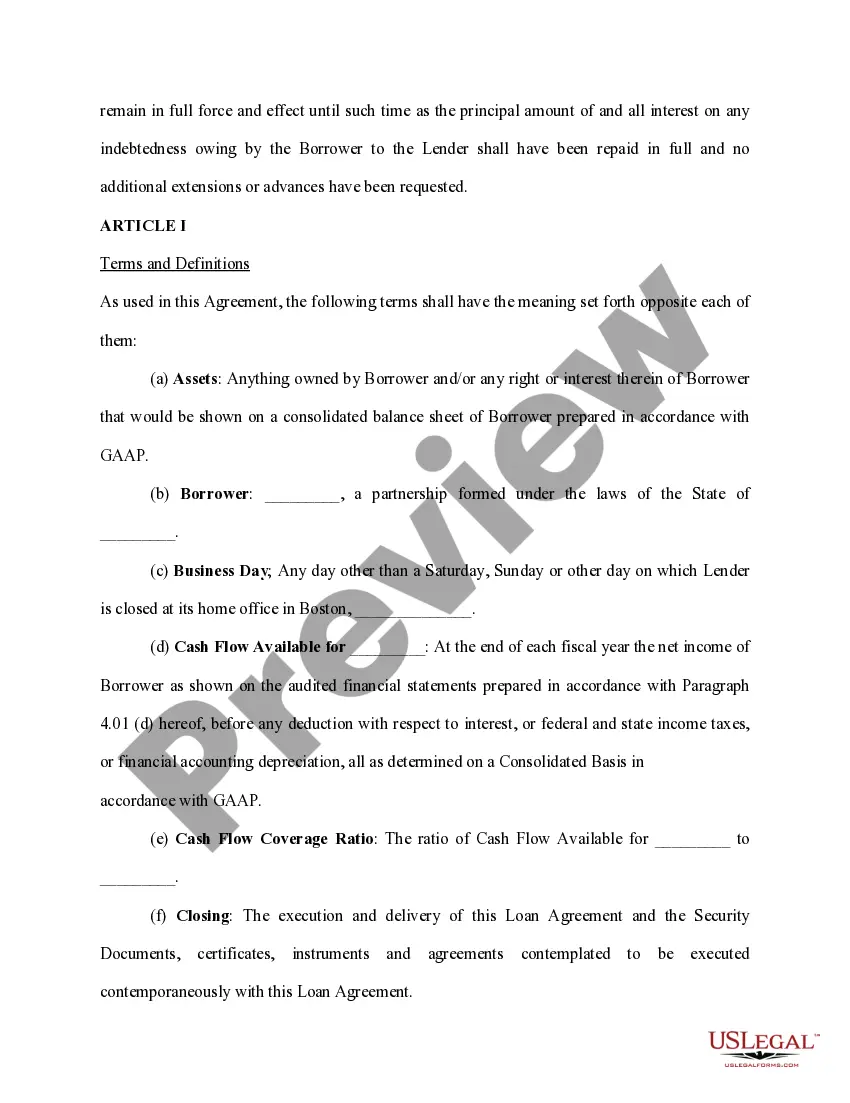

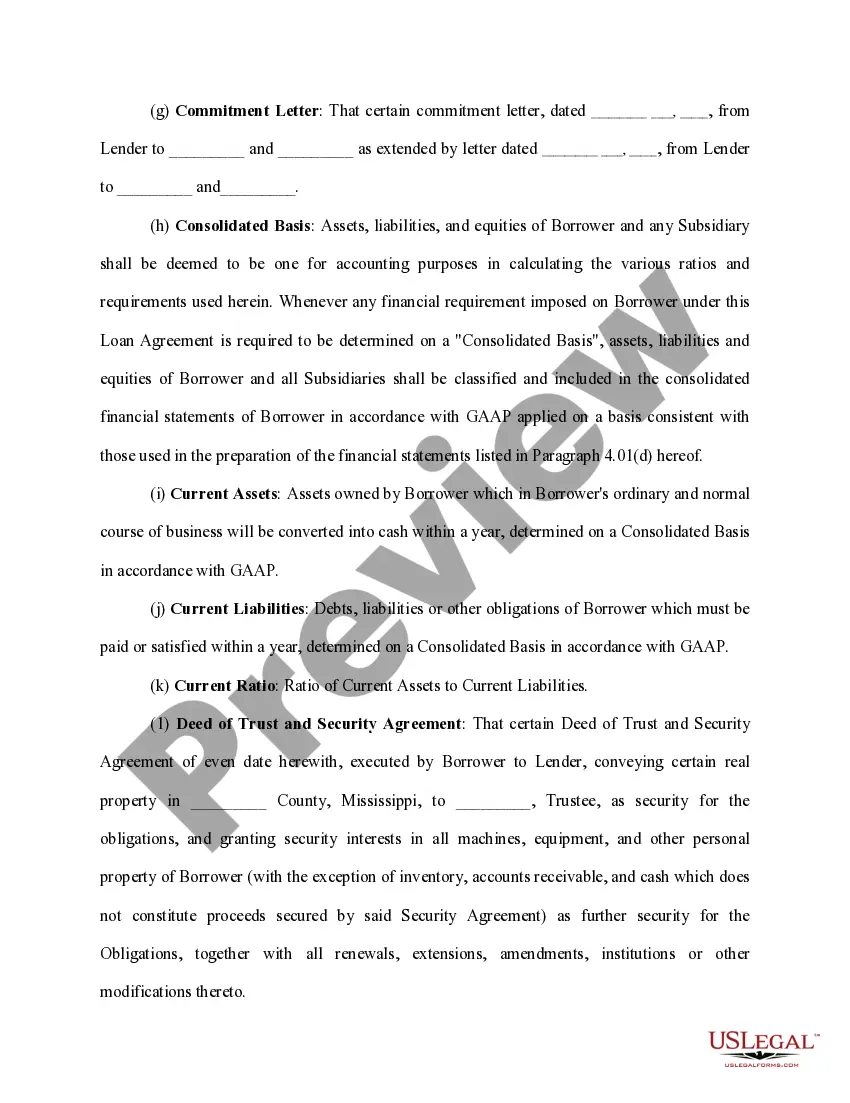

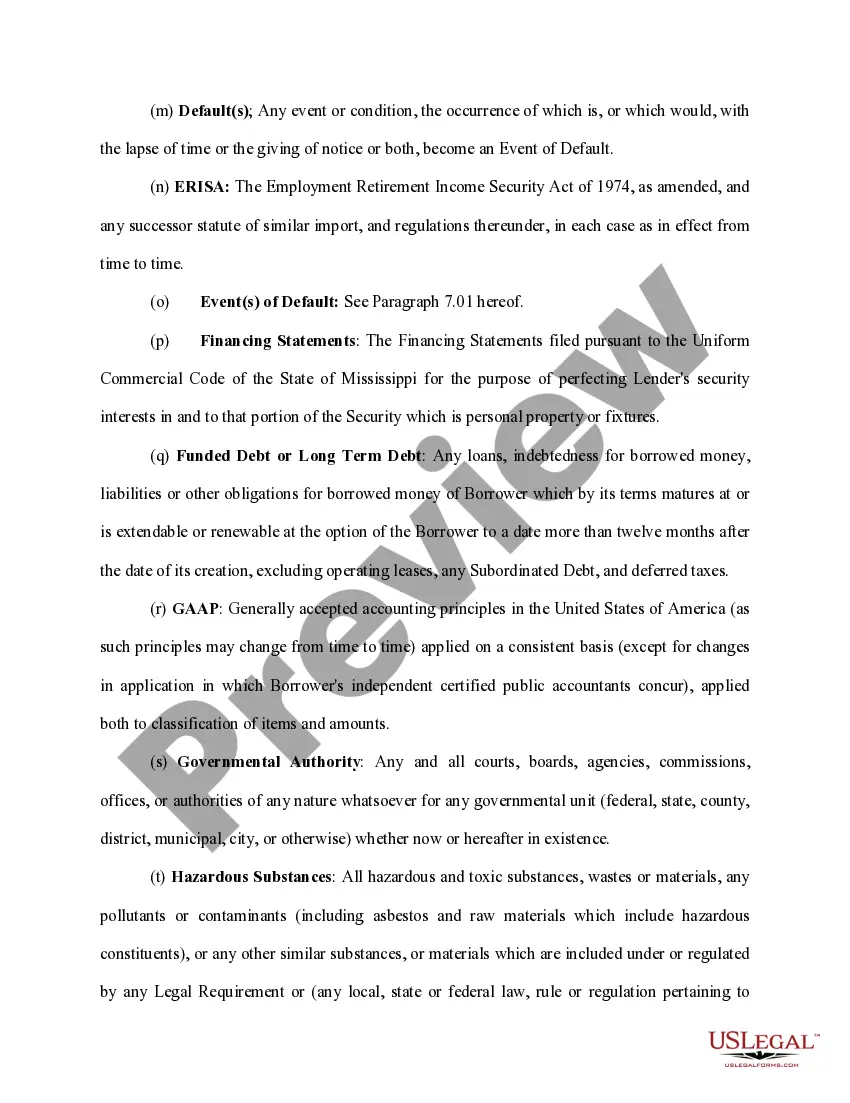

A Wake North Carolina Loan Agreement for Property is a legally binding contract between a lender and a borrower regarding the lending of funds for the purchase or refinancing of a property in Wake County, North Carolina. This agreement outlines the terms and conditions of the loan, including repayment terms, interest rates, and any additional clauses or provisions specific to the transaction. Keywords: Wake North Carolina, Loan Agreement, Property, lender, borrower, funds, purchase, refinancing, terms and conditions, repayment terms, interest rates, transaction. Different types of Wake North Carolina Loan Agreements for Property may include: 1. Residential Property Loan Agreement: This type of agreement is commonly used for financing the purchase or refinancing of residential properties, such as houses, condominiums, or townhouses. 2. Commercial Property Loan Agreement: This agreement is tailored for financing commercial properties, including office buildings, retail spaces, warehouses, or industrial properties. 3. Investment Property Loan Agreement: This type of agreement is specifically designed for loans related to investment properties, such as rental homes, vacation properties, or apartment buildings. 4. Construction Loan Agreement: This agreement is used when financing the construction of a property in Wake County, North Carolina. It includes specific provisions related to disbursement of funds based on construction milestones and completion. 5. Land Loan Agreement: This agreement is utilized for loans related to purchasing or developing vacant land in Wake County, North Carolina. It may include provisions regarding land use, zoning restrictions, and environmental considerations. Each type of Wake North Carolina Loan Agreement for Property may have its own unique terms and conditions, depending on the nature of the property and the intended use of the funds. It is crucial for both parties, the lender, and the borrower, to carefully review and understand all clauses and provisions outlined in the loan agreement before signing to ensure a mutually beneficial and legally compliant arrangement.

Wake North Carolina Loan Agreement for Property

Description

How to fill out Wake North Carolina Loan Agreement For Property?

Preparing papers for the business or individual demands is always a huge responsibility. When drawing up a contract, a public service request, or a power of attorney, it's essential to take into account all federal and state regulations of the particular region. However, small counties and even cities also have legislative provisions that you need to consider. All these details make it stressful and time-consuming to create Wake Loan Agreement for Property without professional help.

It's easy to avoid spending money on attorneys drafting your documentation and create a legally valid Wake Loan Agreement for Property by yourself, using the US Legal Forms online library. It is the greatest online collection of state-specific legal documents that are professionally cheched, so you can be certain of their validity when selecting a sample for your county. Earlier subscribed users only need to log in to their accounts to download the needed document.

In case you still don't have a subscription, follow the step-by-step guideline below to get the Wake Loan Agreement for Property:

- Look through the page you've opened and verify if it has the sample you need.

- To do so, use the form description and preview if these options are available.

- To find the one that meets your requirements, utilize the search tab in the page header.

- Double-check that the sample complies with juridical criteria and click Buy Now.

- Pick the subscription plan, then sign in or register for an account with the US Legal Forms.

- Use your credit card or PayPal account to pay for your subscription.

- Download the chosen document in the preferred format, print it, or fill it out electronically.

The great thing about the US Legal Forms library is that all the documentation you've ever acquired never gets lost - you can get it in your profile within the My Forms tab at any time. Join the platform and quickly obtain verified legal forms for any use case with just a couple of clicks!

Form popularity

FAQ

Forbearance is when your mortgage servicer, that's the company that sends your mortgage statement and manages your loan, or lender allows you to pause or reduce your payments for a limited period of time. Forbearance does not erase what you owe. You'll have to repay any missed or reduced payments in the future.

Intercompany loans are loans made from one business unit of a company to another, usually for one of the following reasons: To shift cash to a business unit that would otherwise experience a cash shortfall. To shift cash into a business unit (usually corporate) where the funds are aggregated for investment purposes.

A forbearance agreement provides short-term relief for borrowers. With a forbearance, the lender agrees to reduce or suspend mortgage payments for a while. During the forbearance period, the servicer (on behalf of the lender) won't initiate a foreclosure.

Will forbearance hurt my credit? Loan forbearance should not have any impact on your credit. Your lender may report your forbearance, but so long as you fulfill your part of the agreement, no missed payments will be recorded and your score will be unaffected by your choice to participate in a forbearance.

A/B loans are created by International Financial Institutions to support foreign direct investments in emerging markets. FMO uses A/B loan structures to mobilize banks and institutional investors as co-financiers. Under this structure, FMO provides the A portion of the loan from its own resources.

Forbearance lets you skip some or all of your monthly mortgage payments for as much as a year. But forbearance should be a last resort, something to avoid if at all possible. While it can be a lifeline in the short-term, forbearance will undoubtedly lead to credit issues for many down the road.

The biggest disadvantages include: You'll still owe the payments due: Forbearance doesn't erase your obligation to pay your mortgage loan. You have to pay more money later to make up for missed payments.

Most homeowners can temporarily pause or reduce their mortgage payments if they're struggling financially. Forbearance is when your mortgage servicer or lender allows you to pause or reduce your mortgage payments for a limited time while you build back your finances.

Once your forbearance ends, you'll have to make arrangements to repay what you owe (all of the missed payments during forbearance). The options for repayment vary by the loan type, as shown below. Although you can pay what you owe in one lump sum, none of the loans require a lump sum payment once forbearance ends.