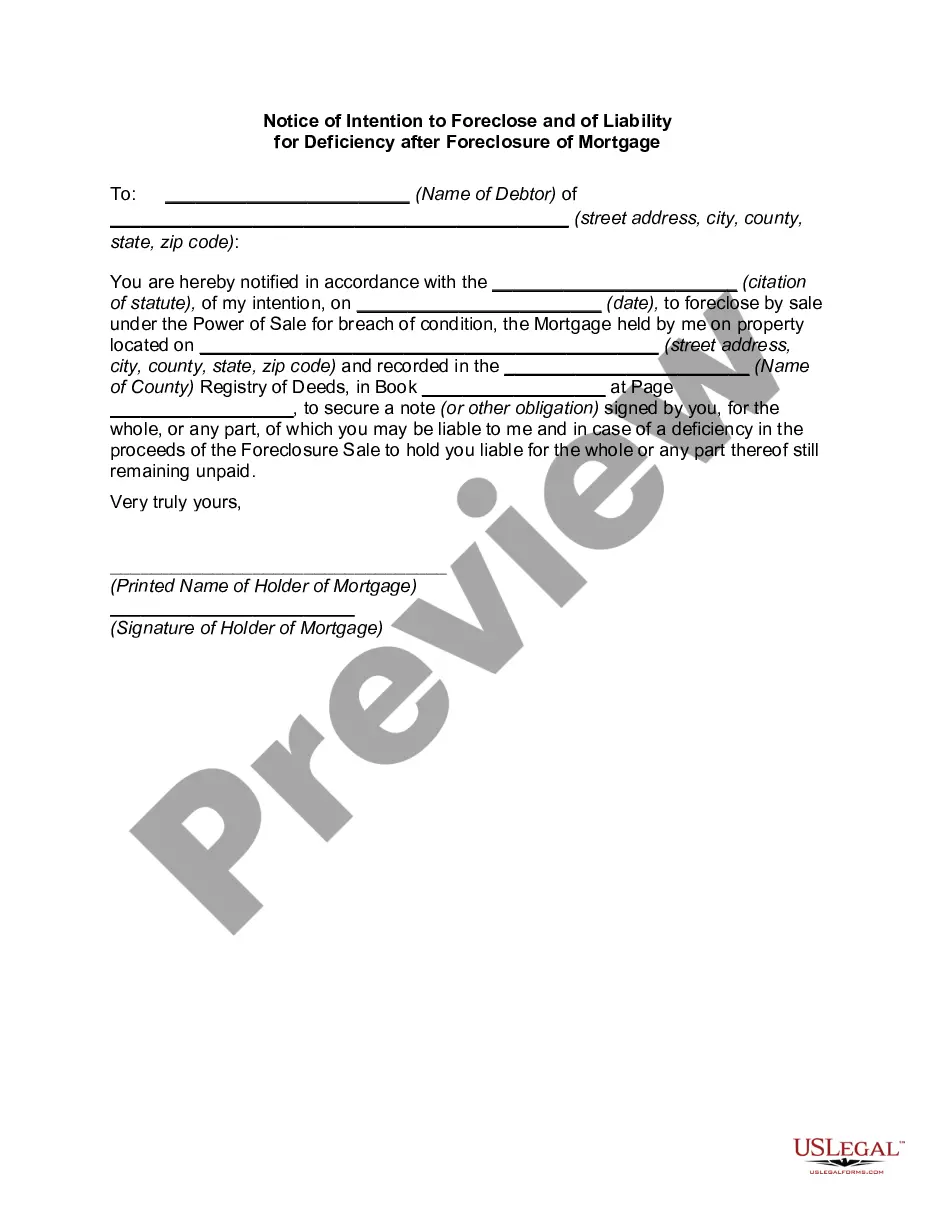

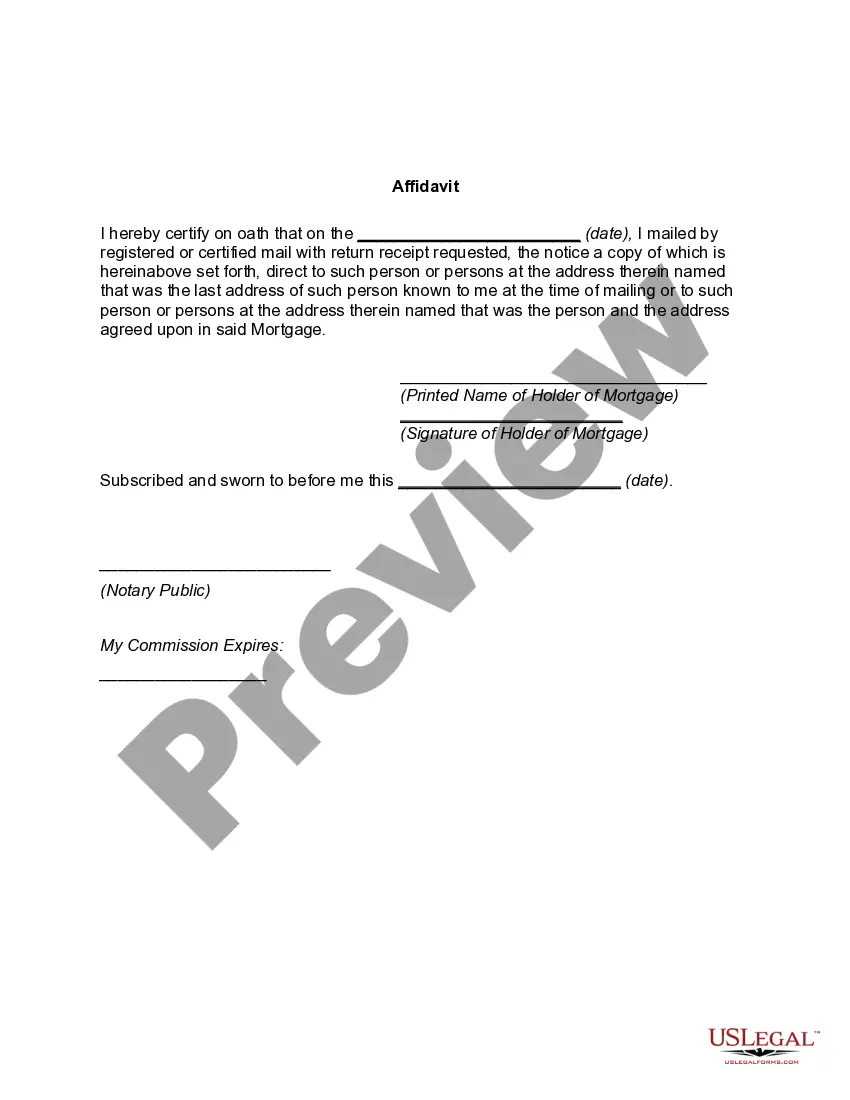

Clark County, located in Nevada, has specific laws and regulations regarding foreclosure procedures and liability for deficiency after the foreclosure of a mortgage. One crucial document involved in the foreclosure process is the Clark Nevada Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage. The Notice of Intention to Foreclose is a legal document issued by a mortgage lender or trustee, notifying the borrower of their intent to foreclose on the property due to non-payment or default on the mortgage. This notice serves as a formal warning to the borrower that legal action will be taken if the outstanding payments are not settled promptly. It outlines the lender's rights, the borrower's responsibilities, and provides information on how to avoid foreclosure. In Clark Nevada, there might be different types of Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage, including: 1. Standard Notice of Intention to Foreclose: This is the most common type of notice issued when the borrower falls behind on mortgage payments. It specifies the amount owed, the deadline for payment, and the consequences if the debt remains unpaid. 2. Short Sale Notice of Intention to Foreclose: In some cases, the lender might agree to a short sale, allowing the borrower to sell the property for less than what is owed on the mortgage. This type of notice provides information on how to proceed with a short sale and the potential ramifications for both the borrower and lender. 3. Notice of Intention to Foreclose and of Liability for Deficiency: This notice occurs when the lender intends to foreclose on the property and seeks to hold the borrower liable for any deficiency after the foreclosure sale. It outlines the borrower's potential responsibilities post-foreclosure, including the possibility of a deficiency judgment against them. The liability for deficiency after foreclosure of a mortgage refers to the borrower's obligation to repay any remaining debt or deficiency left after the foreclosure sale if the proceeds from the sale do not cover the outstanding mortgage balance. The lender may pursue legal action to obtain a judgment in order to recover the remaining debt. Understanding the Clark Nevada Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage is crucial for borrowers facing the risk of foreclosure. Seeking legal advice and exploring alternatives to foreclosure, such as loan modifications or short sales, is highly recommended in such situations. It is important to carefully review any notices received and take appropriate action to protect one's rights and interests.

Clark Nevada Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage

Description

How to fill out Clark Nevada Notice Of Intention To Foreclose And Of Liability For Deficiency After Foreclosure Of Mortgage?

Laws and regulations in every area differ throughout the country. If you're not a lawyer, it's easy to get lost in a variety of norms when it comes to drafting legal paperwork. To avoid high priced legal assistance when preparing the Clark Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage, you need a verified template legitimate for your region. That's when using the US Legal Forms platform is so helpful.

US Legal Forms is a trusted by millions web collection of more than 85,000 state-specific legal forms. It's a great solution for professionals and individuals looking for do-it-yourself templates for various life and business scenarios. All the documents can be used many times: once you pick a sample, it remains available in your profile for further use. Thus, when you have an account with a valid subscription, you can simply log in and re-download the Clark Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage from the My Forms tab.

For new users, it's necessary to make several more steps to get the Clark Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage:

- Analyze the page content to make sure you found the correct sample.

- Use the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your requirements.

- Click on the Buy Now button to get the template when you find the appropriate one.

- Opt for one of the subscription plans and log in or create an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Select the format you want to save the file in and click Download.

- Complete and sign the template on paper after printing it or do it all electronically.

That's the simplest and most affordable way to get up-to-date templates for any legal reasons. Locate them all in clicks and keep your paperwork in order with the US Legal Forms!

Form popularity

FAQ

Key Takeaways. A deficiency judgment is a court ruling allowing a lender to collect additional funds from a debtor when the sale of their secured property falls short of paying off the full debt. Many states prohibit deficiency judgments after a home foreclosure.

When a borrower loses their home to foreclosure and still owes their lender money after the sale, the remaining debt is usually referred to as a deficiency. Lenders can sue to recover this amount.

Who is Responsible for the Deficiency Balance? The original borrower is responsible for paying the deficiency balance. However, some lenders may forgive or write off that balance if it's clear the borrower has no assets to pay. In those cases, any amount greater than $600 counts as taxable income.

Written by Attorney John Coble. If your home is foreclosed on, the lender will sell it and you'll have to find a new place to live. If the sale proceeds don't cover what you owed on your mortgage, the lender may go after you for the difference. This is called a deficiency.

To obtain a deficiency judgment against the borrower after the foreclosure sale, the mortgage lender has to file a motion for deficiency. The lender will allege the property's market value on the sale date and the deficiency amount. The homeowner can defend the motion and can contest the lender's valuation.

The deficiency is $50,000. In some states, the lender can seek a personal judgment against the debtor to recover the deficiency. Generally, once the lender gets a deficiency judgment, the lender may collect this amountin our example, $50,000from the borrower.

Second Mortgages Although a primary mortgage lender's ability to come after an individual following a foreclosure depends directly on the type of loan the borrower had and the laws in her state of residence, second mortgage lenders can almost always file a lawsuit after foreclosure.

The statute of limitations for getting a deficiency judgment for residential properties with no more than four dwelling units is one year. The limitations period starts on the day after the clerk of court issues the certificate of title to the person or entity that bought the home at the foreclosure sale. (Fla. Stat.

Sometimes, lenders can't sell foreclosed homes at a price high enough to cover all the debt that borrowers still owe on their mortgage loans. When that happens, the lender takes a loss on the sale. That loss is known as a deficiency.

When a borrower loses their home to foreclosure and still owes their lender money after the sale, the remaining debt is usually referred to as a deficiency. Lenders can sue to recover this amount.