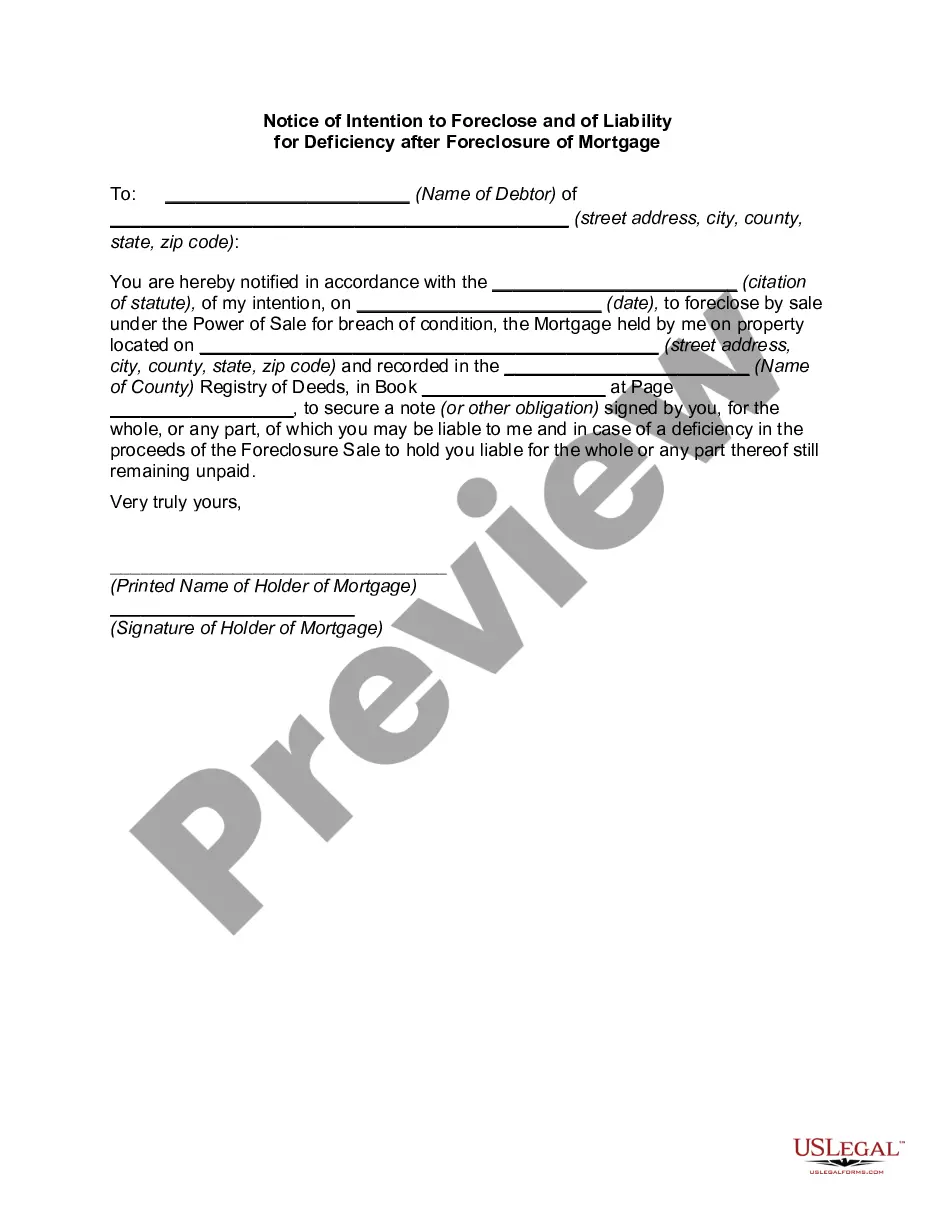

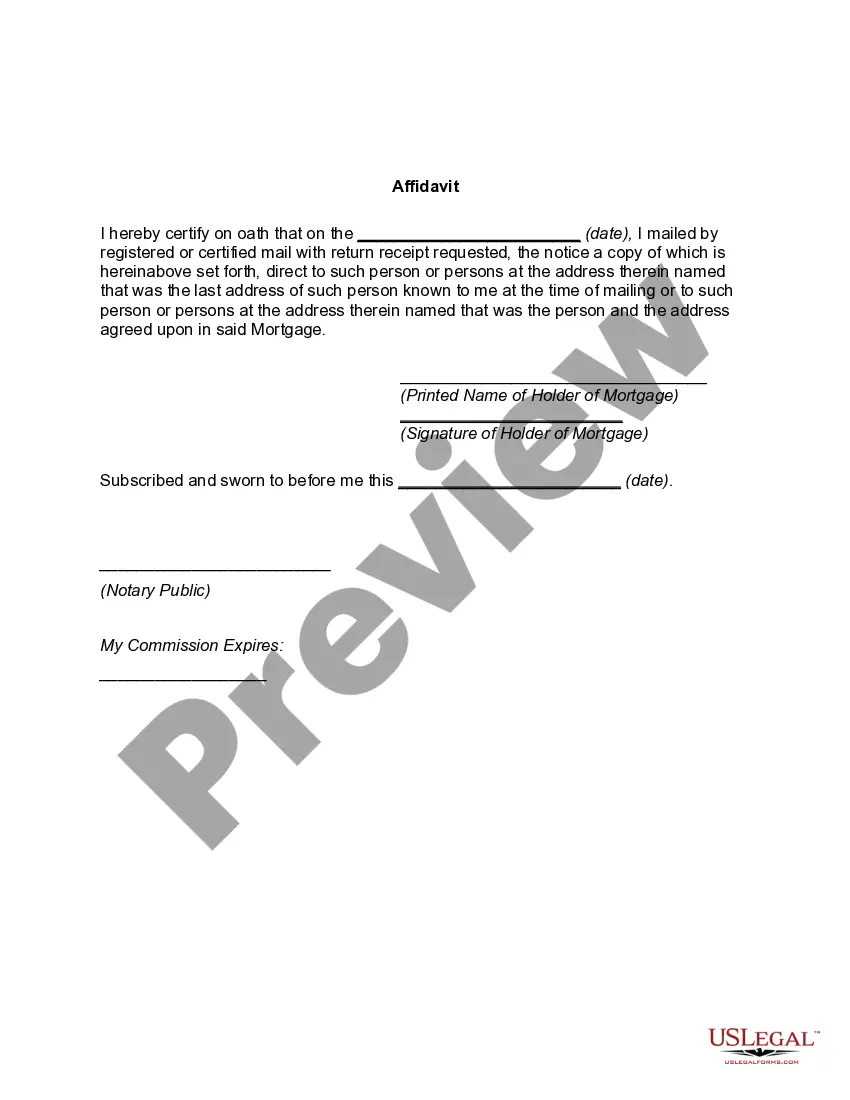

Hennepin County, Minnesota, is home to a range of legal processes related to foreclosure of mortgage properties. One important document in this regard is the "Hennepin Minnesota Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage." This notice serves as a crucial communication to borrowers, informing them of the lender's intention to foreclose on their mortgage due to non-payment or other defaults. It is essential for borrowers to understand the implications and potential liabilities associated with a foreclosure action. The Hennepin Minnesota Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage is designed to provide transparency and clarity to both the borrower and the lender. By formalizing the intention to initiate foreclosure proceedings, this document enables borrowers to take necessary actions, such as seeking legal advice or exploring alternative options to avoid foreclosure. When a borrower receives this notice, they should carefully review it to comprehend the information it contains. The notice typically outlines the legal basis for the foreclosure, including the details of missed payments, breach of contract, or any other relevant grounds. It will mention the lender's intention to sell the property through a foreclosure sale to recoup the outstanding loan amount. Moreover, the notice should specify the borrower's rights and potential liabilities after the foreclosure. In Hennepin County, Minnesota, there are different types of liabilities that a borrower may face, depending on various circumstances. These can include a deficiency judgment, which is a court order obligating the borrower to pay the difference between the sale price of the foreclosed property and the outstanding loan balance. Another possibility is a non-recourse loan, where certain types of mortgages may limit the lender's ability to pursue the borrower for any deficiency. Understanding the intricacies of the Hennepin Minnesota Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage is of utmost importance for borrowers to plan their course of action wisely. Seeking legal counsel is strongly advised to navigate through the complexities of foreclosure proceedings in Hennepin County. By reviewing the notice promptly and comprehensively, borrowers can evaluate their options, negotiate with lenders, explore loan modifications, or explore alternatives such as short sales or deed-in-lieu of foreclosure arrangements. In summary, the Hennepin Minnesota Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage is a critical document that brings borrowers face-to-face with the potential consequences of non-payment or default on their mortgage. By fully understanding the notice, borrowers can make informed decisions to protect their rights, explore alternatives, or negotiate with lenders. Seeking professional advice is essential to fully comprehend the implications and make the best choices moving forward during this challenging situation.

Hennepin Minnesota Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage

Description

How to fill out Hennepin Minnesota Notice Of Intention To Foreclose And Of Liability For Deficiency After Foreclosure Of Mortgage?

If you need to find a trustworthy legal paperwork supplier to obtain the Hennepin Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage, consider US Legal Forms. Whether you need to launch your LLC business or manage your belongings distribution, we got you covered. You don't need to be well-versed in in law to find and download the needed template.

- You can browse from more than 85,000 forms categorized by state/county and case.

- The self-explanatory interface, variety of learning materials, and dedicated support team make it easy to find and complete various paperwork.

- US Legal Forms is a reliable service providing legal forms to millions of customers since 1997.

You can simply type to look for or browse Hennepin Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage, either by a keyword or by the state/county the form is intended for. After locating required template, you can log in and download it or retain it in the My Forms tab.

Don't have an account? It's easy to get started! Simply find the Hennepin Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage template and check the form's preview and short introductory information (if available). If you're comfortable with the template’s legalese, go ahead and click Buy now. Register an account and choose a subscription plan. The template will be immediately ready for download once the payment is processed. Now you can complete the form.

Taking care of your legal matters doesn’t have to be expensive or time-consuming. US Legal Forms is here to demonstrate it. Our extensive collection of legal forms makes these tasks less expensive and more affordable. Set up your first business, organize your advance care planning, create a real estate agreement, or complete the Hennepin Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage - all from the convenience of your sofa.

Join US Legal Forms now!

Form popularity

FAQ

In a recourse state, the homeowner remains responsible for any remaining debt through a deficiency judgment. Minnesota is generally considered to be a non-recourse state, although in certain situations mortgage-holders (or other creditors) may seek a deficiency judgment.

The deed in lieu alternative to foreclosure offers several advantages to both the borrower and the lender: 2. The borrower obtains immediate release from most or all of the personal indebtedness associated with the defaulted loan. 3.

The property is no greater than 2.5 acres in size; and. The lender is seeking a deficiency judgment specifically for a loan that was used to purchase the foreclosed upon property....Which States Have Anti-Deficiency Laws? Alaska; Arizona; California; Connecticut; Idaho; Minnesota; North Carolina; North Dakota;

A deed in lieu of foreclosure can release you from your mortgage responsibilities and allow you to avoid a foreclosure on your credit report. When you hand over the deed, the lender releases its lien on the property. This allows the lender to recoup some of the losses without forcing you into foreclosure.

Disadvantages to Lender A lender should also hesitate before accepting a lieu deed where there are outstanding subordinate liens or judgments against the property. In such a situation, the lender will have to foreclose its mortgage, with the attendant expense and time involved to obtain clear title.

§ 580c states that no deficiency judgment shall lie in any event on any loan, refinance, or other credit transaction which is used to refinance a purchase money loan, or subsequent refinances to a purchase money loan, except to the extent that the lender advances new principal which is not applied to the balance on the

Most states allow deficiency judgments. Only Alaska, California, Minnesota, Montana, Oregon and Washington forbid deficiency judgments in most cases. Other states only allow deficiency judgments in certain instances. In Arizona, lenders can't purchase deficiencies for one- or two-family homes on 2.5 acres or less.

Deficiency Judgments Are Permitted in Judicial Foreclosures in Minnesota. If a lender forecloses judicially, then a deficiency judgment is possible.

When a borrower loses their home to foreclosure and still owes their lender money after the sale, the remaining debt is usually referred to as a deficiency. Lenders can sue to recover this amount.

Sometimes, lenders can't sell foreclosed homes at a price high enough to cover all the debt that borrowers still owe on their mortgage loans. When that happens, the lender takes a loss on the sale. That loss is known as a deficiency.