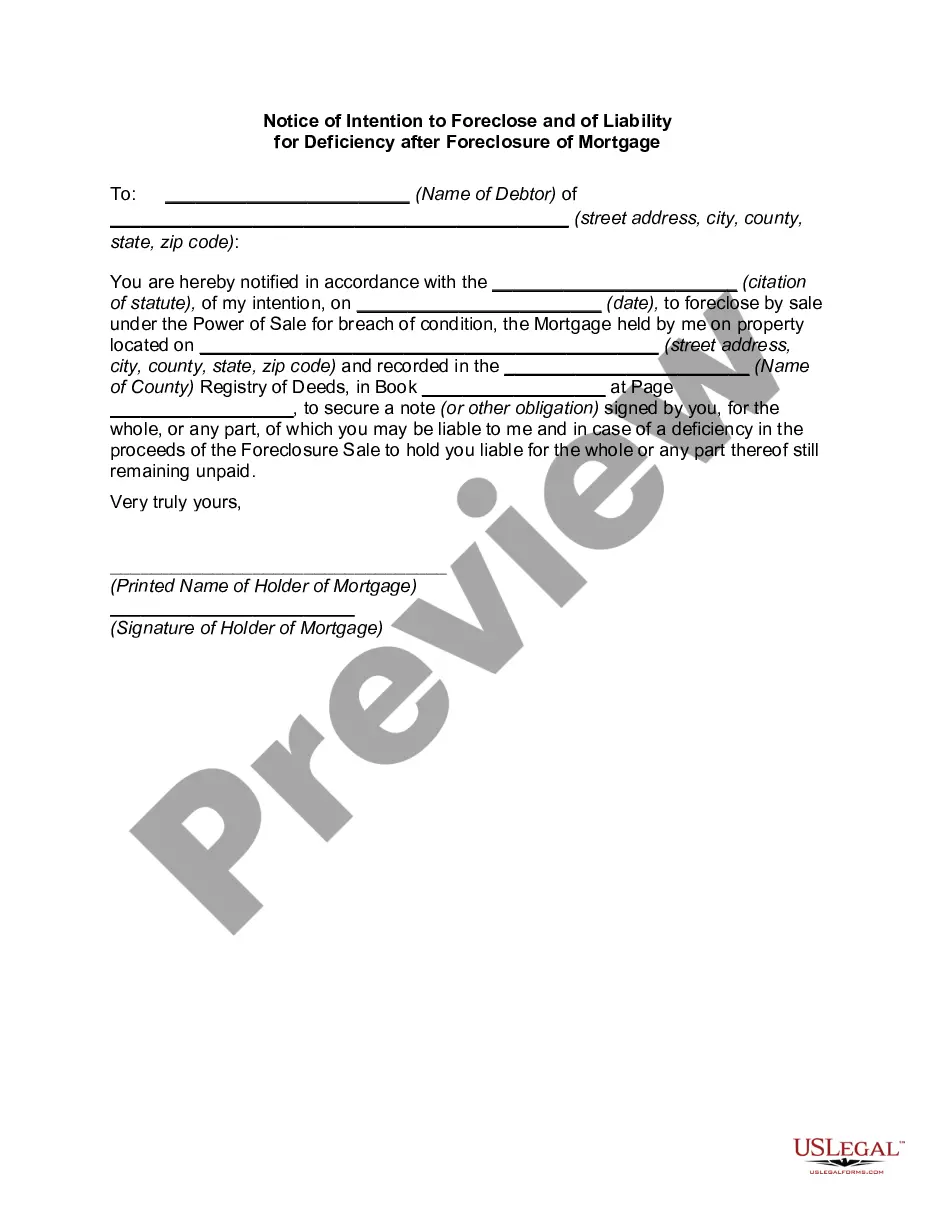

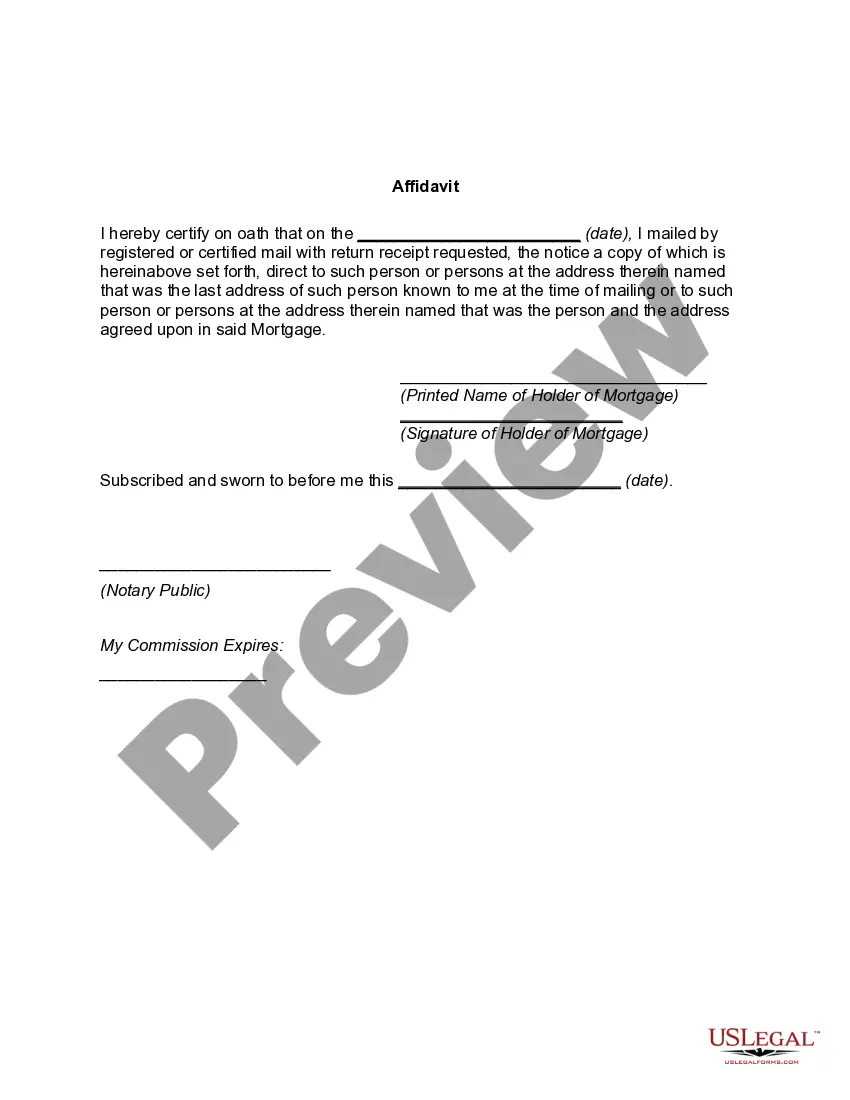

Salt Lake City, Utah: Understanding the Notice of Intention to Foreclose and Liability for Deficiency after Mortgage Foreclosure In Salt Lake City, Utah, homeowners facing financial difficulties may encounter a Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage. This legal notice serves as a formal communication from the lender to the borrower, indicating their intent to initiate foreclosure proceedings due to mortgage default. The Notice of Intention to Foreclose is a critical document provided to the homeowner, outlining the lender's intention to foreclose on the property if the outstanding mortgage payments are not resolved within a specific timeframe. It is essential for borrowers to comprehend the implications of this notice, as failure to act or respond appropriately may lead to foreclosure and potential liability for a deficiency after the property is sold. Different types or variations of the Notice of Intention to Foreclose may exist in Salt Lake City, Utah, depending on the specific circumstances of each case. These variations may include: 1. Strict Foreclosure: A notice indicating the lender's intent to obtain legal ownership rights to the property without a public auction or sale. This may occur when the mortgage agreement permits strict foreclosure or when there is equity in the property. 2. Judicial Foreclosure: This type of notice is relevant when the lender initiates a foreclosure lawsuit, involving the court's intervention to determine the delinquent homeowner's rights and obligations. Judicial foreclosure is a formal legal process ensuring the borrower's due process rights are protected. 3. Non-Judicial Foreclosure: In cases where the mortgage agreement includes a power of sale provision, the lender may proceed with non-judicial foreclosure. This type of notice allows the lender to sell the property through a trustee or designated representative, without court involvement. Non-judicial foreclosure offers a faster and more streamlined process for lenders while still adhering to necessary legal requirements. Alongside the Notice of Intention to Foreclose, borrowers should be aware of potential liability for deficiency after the foreclosure of their mortgage. If the foreclosure sale proceeds do not cover the full outstanding mortgage balance, the lender may pursue the homeowner for the remaining deficiency amount. To protect their interests, borrowers may be required to respond to the Notice of Intention to Foreclose and explore their options, such as loan modifications, repayment plans, or seeking legal advice. Prompt action and open communication with the lender can often help homeowners avoid foreclosure and mitigate the risk of deficiency liability. In conclusion, receiving a Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage in Salt Lake City, Utah, is a significant event for homeowners facing financial difficulties. Understanding the different types of foreclosure notices and the potential liability for deficiencies can help borrowers navigate the process, seek assistance, and work towards finding a viable solution to retain their property.

Salt Lake Utah Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage

Description

How to fill out Salt Lake Utah Notice Of Intention To Foreclose And Of Liability For Deficiency After Foreclosure Of Mortgage?

How much time does it usually take you to draw up a legal document? Because every state has its laws and regulations for every life scenario, locating a Salt Lake Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage meeting all local requirements can be tiring, and ordering it from a professional attorney is often expensive. Numerous online services offer the most popular state-specific templates for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most extensive online catalog of templates, grouped by states and areas of use. In addition to the Salt Lake Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage, here you can get any specific document to run your business or individual deeds, complying with your regional requirements. Experts verify all samples for their actuality, so you can be sure to prepare your documentation properly.

Using the service is pretty straightforward. If you already have an account on the platform and your subscription is valid, you only need to log in, pick the needed sample, and download it. You can retain the file in your profile at any time in the future. Otherwise, if you are new to the website, there will be some extra actions to complete before you get your Salt Lake Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage:

- Check the content of the page you’re on.

- Read the description of the sample or Preview it (if available).

- Look for another document utilizing the corresponding option in the header.

- Click Buy Now when you’re certain in the selected file.

- Select the subscription plan that suits you most.

- Register for an account on the platform or log in to proceed to payment options.

- Make a payment via PalPal or with your credit card.

- Change the file format if necessary.

- Click Download to save the Salt Lake Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage.

- Print the doc or use any preferred online editor to complete it electronically.

No matter how many times you need to use the purchased template, you can locate all the files you’ve ever downloaded in your profile by opening the My Forms tab. Try it out!