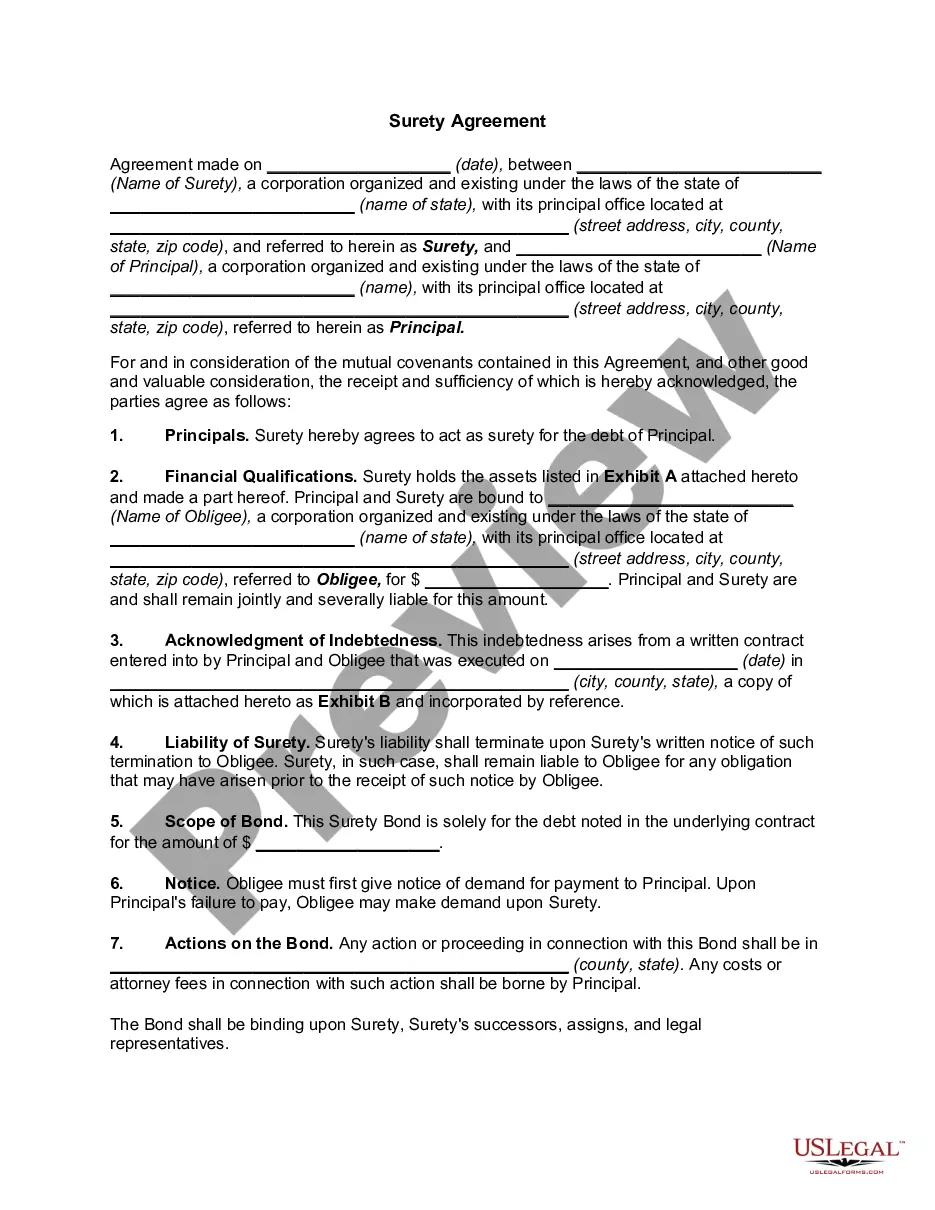

A Fairfax Virginia Surety Agreement is a legal document that serves as a financial guarantee between three parties: the principal, the obliged, and the surety. It is commonly used in various industries, including construction, real estate, and business contracts. This agreement ensures that the principal fulfills their obligations, such as completing a project or adhering to the terms of a contract, by providing a guarantee from the surety in case of non-performance or default. Fairfax Virginia Surety Agreements come in several types, each tailored to specific situations and industries: 1. Contract Surety Agreement: This type is widely used in construction projects. It guarantees that the principal (typically the contractor) will fulfill the contract obligations, including completion of work, payment to subcontractors, and meeting quality standards. 2. Performance Surety Agreement: Designed for contracts where the principal has agreed to perform certain obligations, such as delivering goods or services. The surety ensures that the principal performs as promised, providing compensation in case of failure. 3. Payment Surety Agreement: Mainly used in the construction industry, this agreement guarantees that subcontractors and suppliers will be paid by the principal. If the principal fails to pay, the surety steps in and covers the outstanding amounts. 4. Maintenance Surety Agreement: Often included as part of a construction contract, this type ensures that the principal will rectify any defects or issues during a specified maintenance period after project completion. 5. Court Surety Agreement: This agreement is related to court proceedings, such as bail bonds. The surety guarantees the appearance of the principal in court and covers any financial obligations if the principal fails to appear. A Fairfax Virginia Surety Agreement provides protection and assurance to the obliged (usually the project owner or counterparty), reducing the risks associated with non-performance or default. The surety company evaluates the financial capacity and track record of the principal before agreeing to issue the bond. In case of a bond claim, the surety steps in to compensate the obliged, and the principal becomes liable to reimburse the surety for the amount paid. In summary, a Fairfax Virginia Surety Agreement is a legal contract that guarantees the performance and financial obligations of the principal in various industries. Its different types cater to specific situations, such as construction projects, contract performance, payment obligations, maintenance periods, or court proceedings. By providing financial security, these agreements promote trust and mitigate risks for all parties involved in a transaction or project.

Fairfax Virginia Surety Agreement

Description

How to fill out Fairfax Virginia Surety Agreement?

How much time does it normally take you to create a legal document? Since every state has its laws and regulations for every life situation, locating a Fairfax Surety Agreement suiting all regional requirements can be tiring, and ordering it from a professional lawyer is often expensive. Many online services offer the most popular state-specific templates for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most comprehensive online catalog of templates, collected by states and areas of use. Aside from the Fairfax Surety Agreement, here you can get any specific document to run your business or individual deeds, complying with your regional requirements. Specialists verify all samples for their actuality, so you can be sure to prepare your documentation correctly.

Using the service is remarkably straightforward. If you already have an account on the platform and your subscription is valid, you only need to log in, choose the required form, and download it. You can pick the document in your profile at any time in the future. Otherwise, if you are new to the website, there will be a few more steps to complete before you obtain your Fairfax Surety Agreement:

- Examine the content of the page you’re on.

- Read the description of the template or Preview it (if available).

- Search for another document utilizing the corresponding option in the header.

- Click Buy Now once you’re certain in the selected document.

- Select the subscription plan that suits you most.

- Register for an account on the platform or log in to proceed to payment options.

- Make a payment via PalPal or with your credit card.

- Switch the file format if necessary.

- Click Download to save the Fairfax Surety Agreement.

- Print the doc or use any preferred online editor to fill it out electronically.

No matter how many times you need to use the acquired document, you can find all the files you’ve ever saved in your profile by opening the My Forms tab. Give it a try!