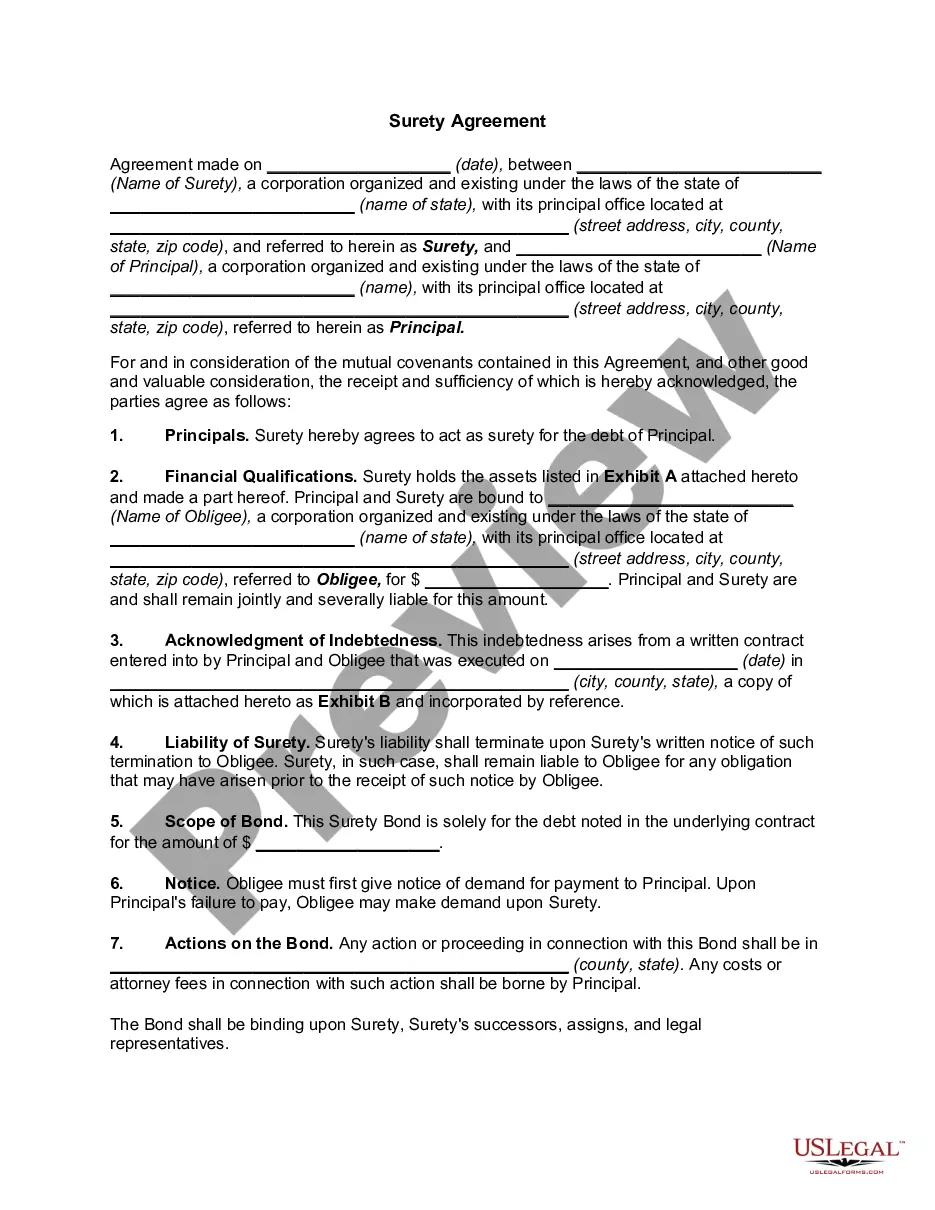

Orange California Surety Agreement is a legally binding contract that specifies the responsibilities, obligations, and liabilities between three parties: the principal, the surety, and the obliged. This agreement is commonly used in Orange County, California, to ensure the completion of construction projects or fulfill certain obligations. Surety agreements are crucial for projects, as they provide financial protection to the obliged if the principal fails to meet the agreed-upon terms. The principal is typically the contractor or the party responsible for fulfilling the contract, while the obliged is the project owner or the party that requires the work to be done. There are different types of Orange California Surety Agreements, each serving a specific purpose: 1. Bid Bond Agreement: This type of agreement guarantees that the principal will enter into a contract if awarded the project. It ensures that the bidder is serious and financially capable of undertaking the project. 2. Performance Bond Agreement: This agreement ensures that the principal will complete the project according to the contract's specifications and within the agreed-upon timeframe. If the principal fails to meet these obligations, the surety will compensate the obliged for any financial loss. 3. Payment Bond Agreement: This type of surety agreement ensures that subcontractors, suppliers, and laborers involved in the project will receive timely payment for their services. If the principal fails to pay these parties, the surety will cover the outstanding debts. 4. Maintenance Bond Agreement: This agreement guarantees the quality of work performed by the principal for a specified period after project completion. It ensures that any defects or issues arising from the completed project will be rectified by the principal at their expense. Orange California Surety Agreements play a vital role in mitigating financial risks and ensuring the successful completion of construction projects or contractual obligations in Orange County, California. They provide assurance to the obliged that they will be protected in case of default or non-performance by the principal. It is advisable for all parties involved in construction projects or contractual agreements to carefully evaluate and negotiate the terms and conditions of the specific surety agreement to protect their interests.

Orange California Surety Agreement

Description

How to fill out Orange California Surety Agreement?

Drafting paperwork for the business or individual demands is always a huge responsibility. When creating an agreement, a public service request, or a power of attorney, it's crucial to consider all federal and state laws and regulations of the particular area. However, small counties and even cities also have legislative provisions that you need to consider. All these aspects make it tense and time-consuming to generate Orange Surety Agreement without professional assistance.

It's easy to avoid spending money on attorneys drafting your documentation and create a legally valid Orange Surety Agreement by yourself, using the US Legal Forms web library. It is the biggest online collection of state-specific legal documents that are professionally cheched, so you can be sure of their validity when picking a sample for your county. Earlier subscribed users only need to log in to their accounts to download the needed form.

If you still don't have a subscription, follow the step-by-step guide below to obtain the Orange Surety Agreement:

- Look through the page you've opened and check if it has the document you need.

- To accomplish this, use the form description and preview if these options are presented.

- To find the one that satisfies your requirements, utilize the search tab in the page header.

- Recheck that the template complies with juridical standards and click Buy Now.

- Opt for the subscription plan, then log in or create an account with the US Legal Forms.

- Use your credit card or PayPal account to pay for your subscription.

- Download the chosen file in the preferred format, print it, or complete it electronically.

The exceptional thing about the US Legal Forms library is that all the documentation you've ever obtained never gets lost - you can access it in your profile within the My Forms tab at any time. Join the platform and quickly get verified legal templates for any situation with just a few clicks!