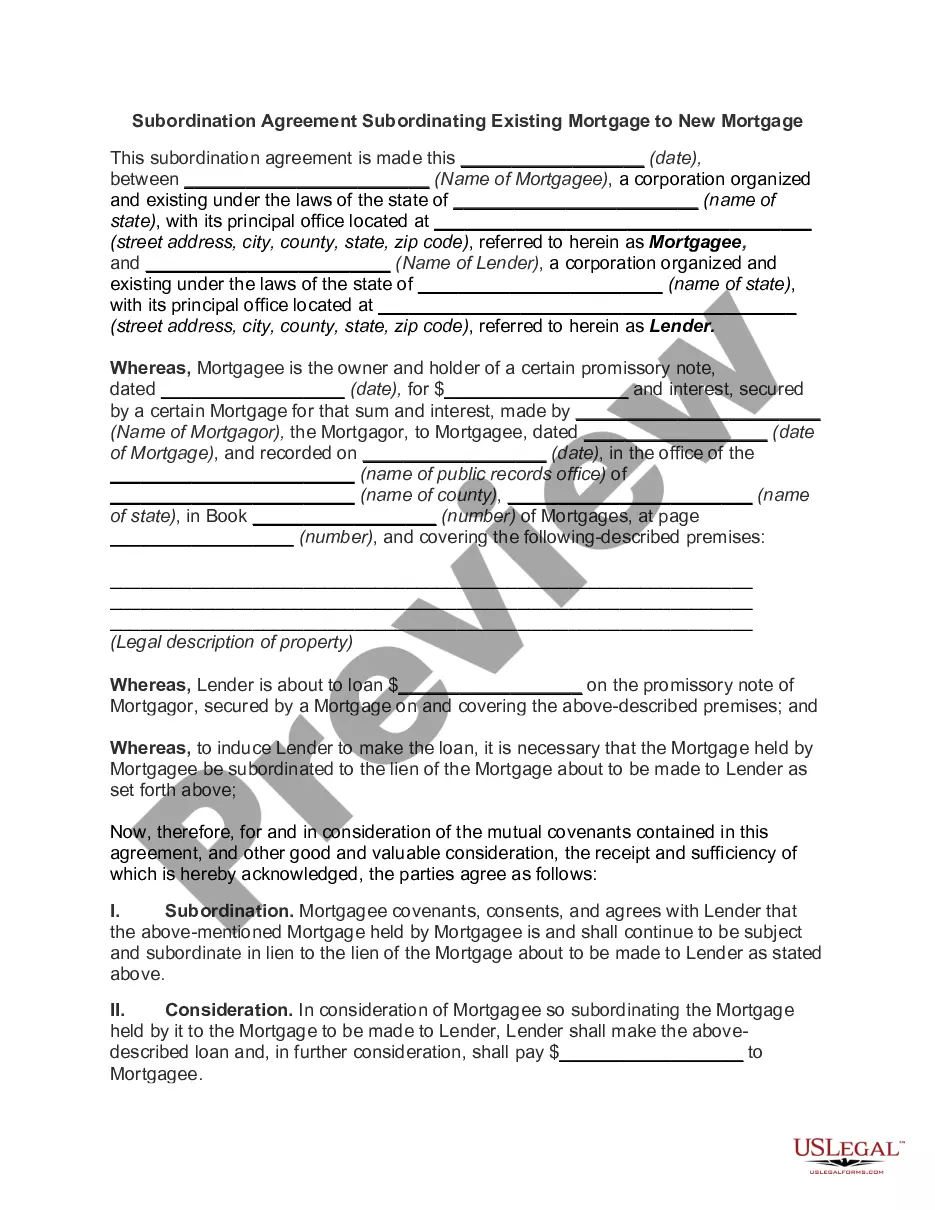

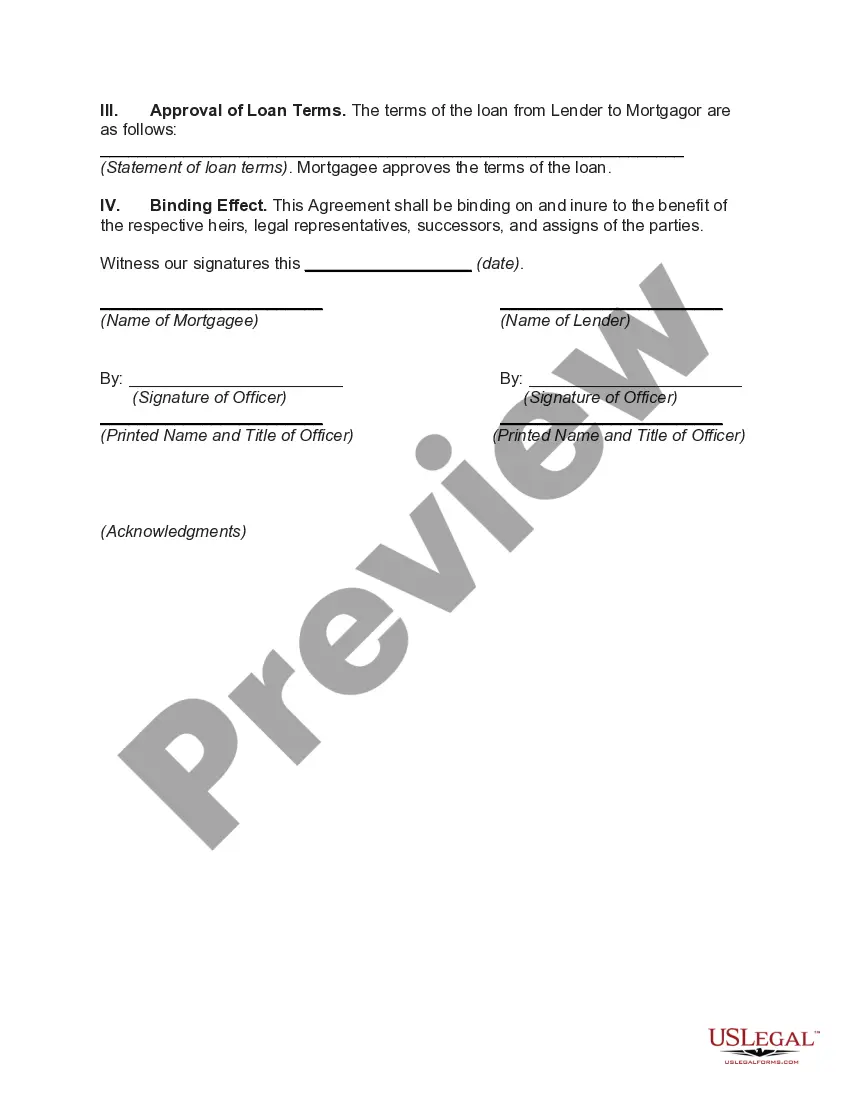

A Contra Costa California Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a legal document that helps prioritize the lien position of mortgages on a property. In simple terms, it is an agreement entered into by the parties involved to establish the order in which their respective mortgages will be paid off in the event of foreclosure or sale of the property. When borrowers wish to refinance their existing mortgages or take out additional loans, lenders require a subordination agreement to protect their interests. By subordinating the existing mortgage to the new mortgage, the lender of the new loan secures a higher priority position, ensuring that in a foreclosure or sale, the new mortgage will be paid off before the existing one. Contra Costa County, California, which is located just east of San Francisco, has various types of Subordination Agreements available for homeowners and lenders: 1. First Mortgage Subordination Agreement: This type of agreement is used when a property owner wants to refinance their existing mortgage with a new loan while maintaining the current lien position of the original mortgage. 2. Second Mortgage Subordination Agreement: If a homeowner wishes to take out a second mortgage or home equity loan, this agreement allows the new lender to establish priority over the existing first mortgage. 3. Construction Loan Subordination Agreement: This type of agreement is commonly used when a homeowner wants to obtain a construction loan while having an existing mortgage. It ensures that the construction lender will have priority over the existing mortgage, safeguarding their investment in case of foreclosure. 4. Home Equity Line of Credit (HELOT) Subordination Agreement: When a homeowner has a HELOT and wants to refinance their primary mortgage, this agreement is necessary to determine the priority of the new mortgage in relation to the existing HELOT. The Contra Costa California Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a crucial legal instrument that safeguards the interests of lenders and borrowers. It provides clarity and establishes the order of lien priority, protecting the rights of all parties involved in various mortgage situations within the county.

Contra Costa California Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Contra Costa California Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Do you need to quickly create a legally-binding Contra Costa Subordination Agreement Subordinating Existing Mortgage to New Mortgage or probably any other document to handle your personal or corporate affairs? You can select one of the two options: hire a professional to write a legal document for you or create it completely on your own. Luckily, there's another solution - US Legal Forms. It will help you receive neatly written legal documents without paying sky-high prices for legal services.

US Legal Forms offers a rich collection of over 85,000 state-compliant document templates, including Contra Costa Subordination Agreement Subordinating Existing Mortgage to New Mortgage and form packages. We offer templates for a myriad of use cases: from divorce paperwork to real estate document templates. We've been out there for over 25 years and got a rock-solid reputation among our clients. Here's how you can become one of them and get the necessary document without extra hassles.

- To start with, carefully verify if the Contra Costa Subordination Agreement Subordinating Existing Mortgage to New Mortgage is tailored to your state's or county's laws.

- If the form has a desciption, make sure to verify what it's intended for.

- Start the searching process again if the template isn’t what you were seeking by using the search bar in the header.

- Select the plan that is best suited for your needs and proceed to the payment.

- Select the file format you would like to get your form in and download it.

- Print it out, complete it, and sign on the dotted line.

If you've already registered an account, you can easily log in to it, locate the Contra Costa Subordination Agreement Subordinating Existing Mortgage to New Mortgage template, and download it. To re-download the form, simply head to the My Forms tab.

It's stressless to find and download legal forms if you use our services. Moreover, the templates we offer are reviewed by industry experts, which gives you greater peace of mind when dealing with legal affairs. Try US Legal Forms now and see for yourself!