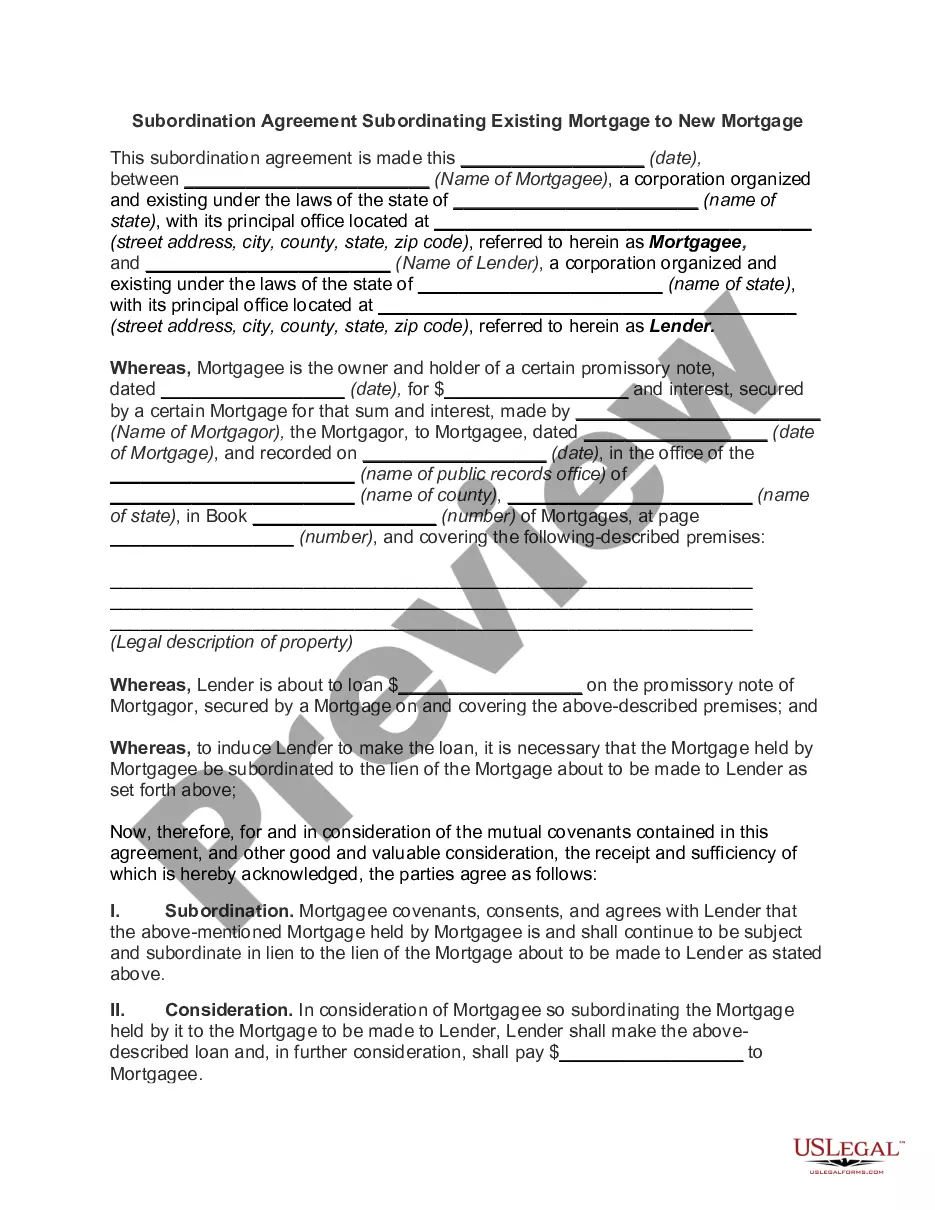

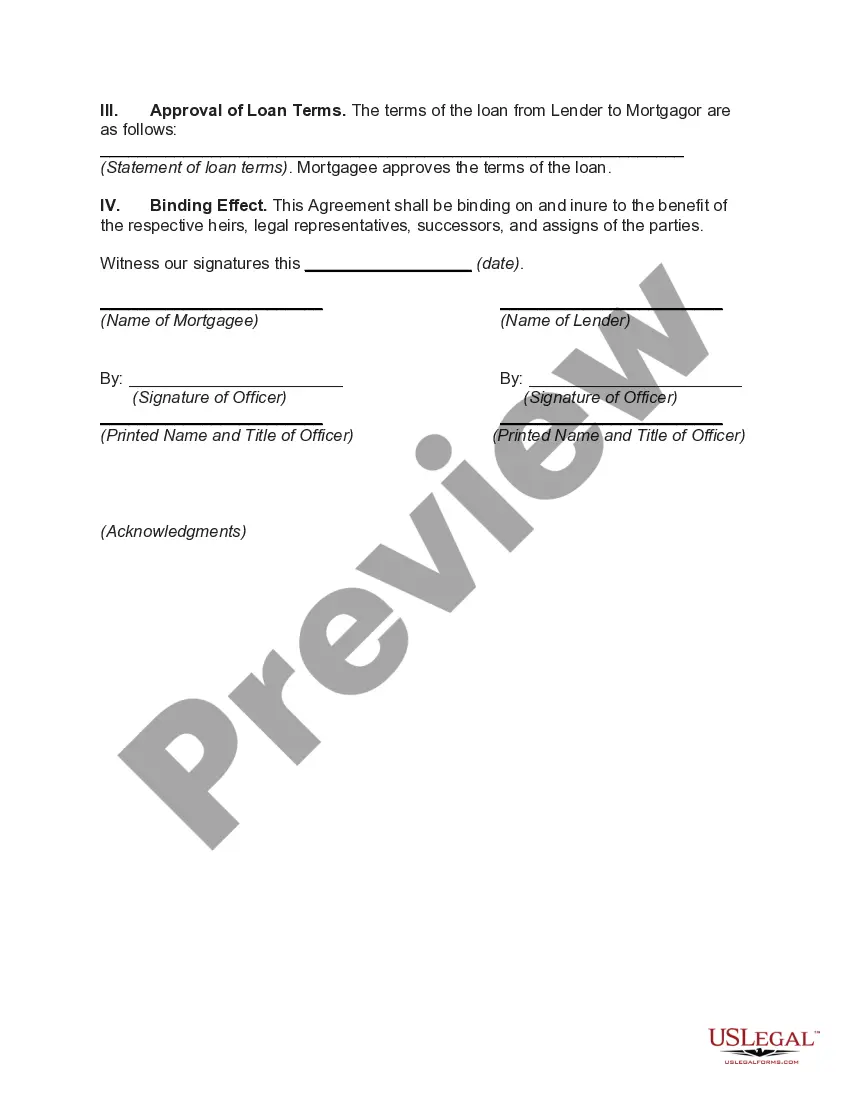

Los Angeles California Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a legal document used in real estate transactions to prioritize the new mortgage over an existing mortgage. This agreement ensures that the new mortgage takes precedence in case of foreclosure or any other legal action. In Los Angeles, California, there are different types of subordination agreements that can be used depending on the specific circumstances: 1. Commercial Subordination Agreement: This type of agreement is used when the property involved is used for commercial purposes, such as retail spaces, office buildings, or industrial properties. It allows the borrower to obtain financing for improvements, expansions, or debt consolidation without disturbing the existing mortgage. 2. Residential Subordination Agreement: This agreement is utilized in residential real estate transactions. Homeowners often consider a subordination agreement when refinancing their mortgage or seeking a home equity line of credit. It prevents the existing mortgage from being paid off entirely, ensuring that the new lender is the first in line to collect in case of default. 3. Construction Subordination Agreement: In instances where a property is being developed or renovated, a construction subordination agreement is used. This agreement enables the lender financing the construction to have a priority lien, ensuring they are repaid first if the property ends up in foreclosure. It is important to consult with a professional real estate attorney when drafting a subordination agreement, as specific legal language and requirements may vary depending on the jurisdiction. This agreement should outline the terms of subordination, including the priority of liens, conditions for release, and any necessary consents from existing lenders. Overall, a Los Angeles California Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a crucial legal tool that protects the interests of both lenders and borrowers in real estate transactions. By prioritizing the new mortgage, it facilitates the flow of capital and financing opportunities while ensuring a smooth and transparent process in the event of default or foreclosure.

Los Angeles California Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Los Angeles California Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

How much time does it typically take you to draw up a legal document? Given that every state has its laws and regulations for every life scenario, locating a Los Angeles Subordination Agreement Subordinating Existing Mortgage to New Mortgage suiting all regional requirements can be stressful, and ordering it from a professional lawyer is often expensive. Numerous web services offer the most common state-specific documents for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most comprehensive web collection of templates, gathered by states and areas of use. Aside from the Los Angeles Subordination Agreement Subordinating Existing Mortgage to New Mortgage, here you can find any specific document to run your business or personal deeds, complying with your regional requirements. Professionals verify all samples for their validity, so you can be sure to prepare your documentation correctly.

Using the service is pretty easy. If you already have an account on the platform and your subscription is valid, you only need to log in, opt for the needed sample, and download it. You can get the document in your profile anytime in the future. Otherwise, if you are new to the website, there will be a few more steps to complete before you get your Los Angeles Subordination Agreement Subordinating Existing Mortgage to New Mortgage:

- Examine the content of the page you’re on.

- Read the description of the sample or Preview it (if available).

- Search for another document using the related option in the header.

- Click Buy Now once you’re certain in the chosen document.

- Select the subscription plan that suits you most.

- Sign up for an account on the platform or log in to proceed to payment options.

- Pay via PalPal or with your credit card.

- Change the file format if necessary.

- Click Download to save the Los Angeles Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

- Print the doc or use any preferred online editor to fill it out electronically.

No matter how many times you need to use the acquired template, you can find all the samples you’ve ever downloaded in your profile by opening the My Forms tab. Give it a try!

Form popularity

FAQ

A second mortgage will become a subordinate loan. If you repay the primary loan within the term of the second mortgage, then the second mortgage can take its place as the primary loan. As a second mortgage, the lender will be taking on more risk.

The existing second loan moves up to become the first loan. The lender of the first mortgage refinancing will now require that a subordination agreement be signed by the second mortgage lender to reposition it in top priority for debt repayment.

Subordination clauses are most commonly found in mortgage refinancing agreements. Consider a homeowner with a primary mortgage and a second mortgage. If the homeowner refinances his primary mortgage, this in effect means canceling the first mortgage and reissuing a new one.

Yes, it is possible to get a second loan modification though statistically it's obvious that you are less likely to get a second modification if you've had a first, and a third if you were lucky enough to get a second. It is possible though.

What is a Subordinate Mortgage? Subordinate mortgages are loans that have a lower priority status than any other recorded liens (or debts) against a property. When you get the loan you need to purchase your home, this loan is typically recorded as the first repayment priority on your deed after closing.

So, the purpose of a subordination agreement is to adjust the new loan's priority so that in the event of a foreclosure, that lien gets paid off first. In a subordination agreement, a prior lienholder agrees that its lien will be subordinate (junior) to a subsequently recorded lien.

There are many examples of subordinate financing, but some of the most common include: Home Equity Loan. Home equity loans are a type of second mortgage and are taken out against the equity that you have built up in the home.Home Equity Line of Credit (HELOC).Other Second Mortgages.

A second mortgage will become a subordinate loan. If you repay the primary loan within the term of the second mortgage, then the second mortgage can take its place as the primary loan.

The most common type of subordinate lien is a second mortgage. When you get a second mortgage loan, the lender records the lien, representing its claim on the collateral: your real estate. Because your first mortgage provider has the first claim on the property, the second mortgage is considered a subordinate lien.