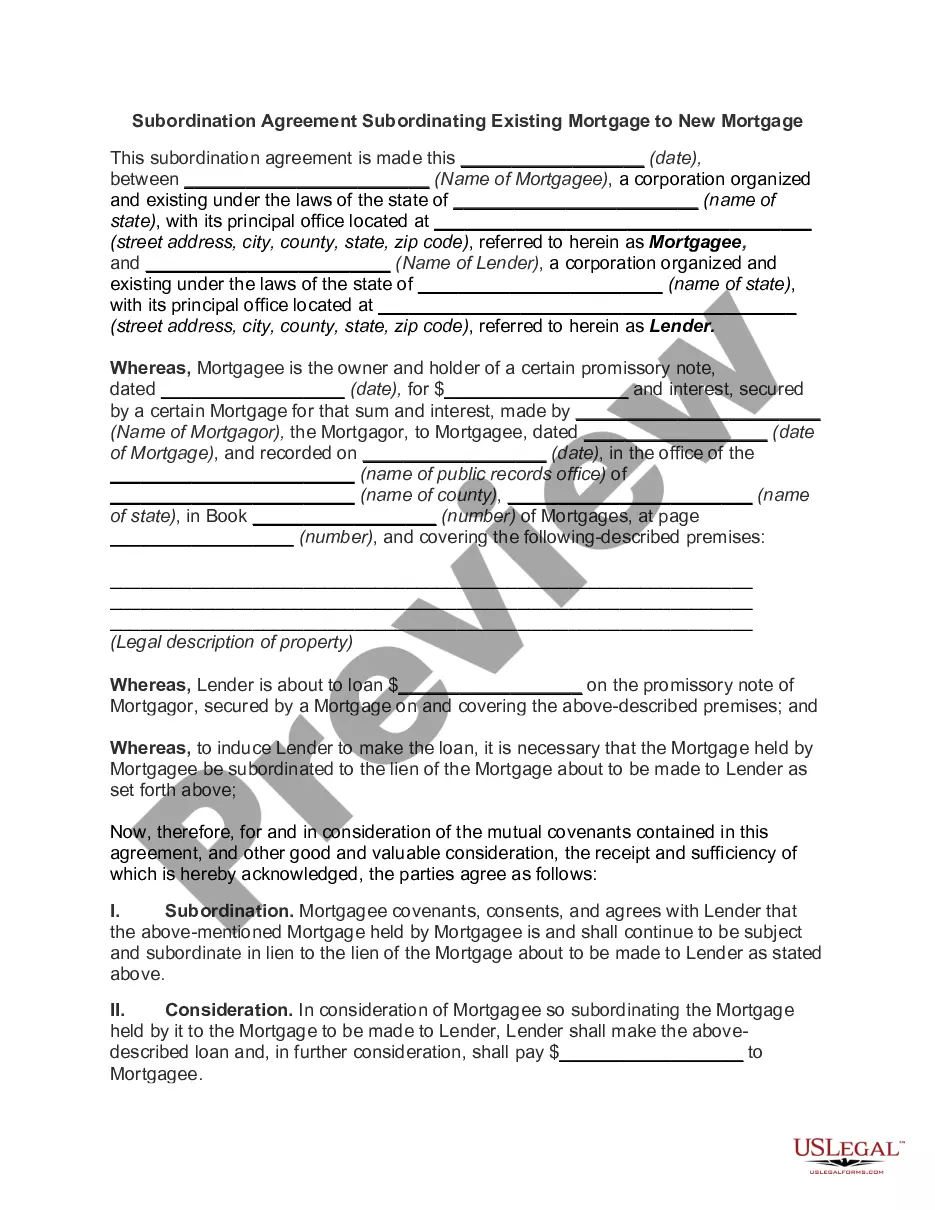

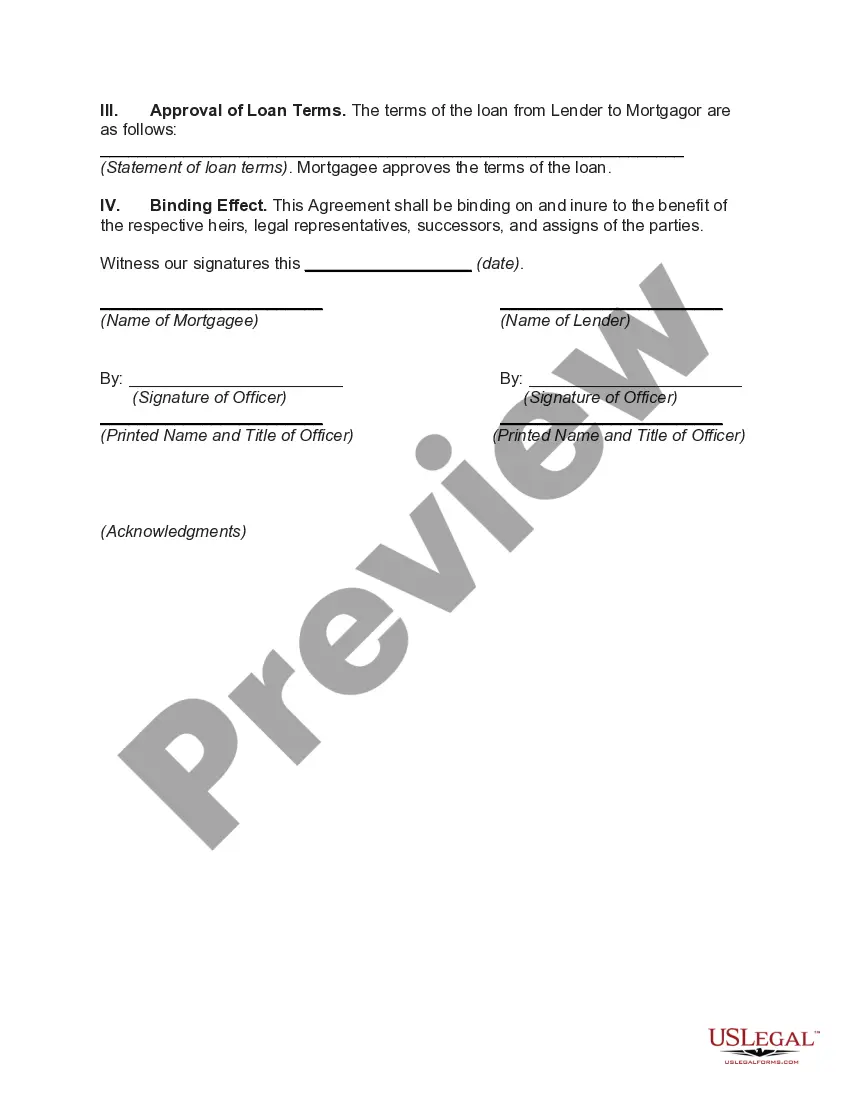

A Philadelphia Pennsylvania Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a legal document that outlines the terms and conditions under which an existing mortgage will be subordinated to a new mortgage. This agreement is commonly used in real estate transactions when there is a need to prioritize the lien on a property. A subordination agreement enables the lender of the new mortgage to assume a higher priority position in the event of default or foreclosure. In other words, if the borrower defaults on the loans, the lender with the higher priority will be paid first from the proceeds of the foreclosure sale. There are a few different types of Philadelphia Pennsylvania Subordination Agreement Subordinating Existing Mortgage to New Mortgage. These include: 1. Commercial Subordination Agreement: This type of agreement is specifically designed for commercial properties in Philadelphia. It allows the existing mortgage to be subordinated to a new mortgage in a commercial real estate transaction. 2. Residential Subordination Agreement: As the name suggests, a residential subordination agreement is applicable to residential properties in Philadelphia. It allows the existing mortgage to be subordinated to a new mortgage in a residential real estate transaction. 3. Second Mortgage Subordination Agreement: In cases where a homeowner has a second mortgage on their property and wishes to take out a new loan, a second mortgage subordination agreement may be required. This agreement ensures that the new mortgage lender has priority over the existing second mortgage. 4. Intercreditor Agreement: In some cases, multiple lenders may have a mortgage interest in the same property. An intercreditor agreement is used to establish the rights and priorities of the lenders in such scenarios. It ensures a fair distribution of proceeds from the sale or foreclosure of the property. In conclusion, a Philadelphia Pennsylvania Subordination Agreement Subordinating Existing Mortgage to New Mortgage is an essential legal document used in real estate transactions. It allows for the determination of the priority of mortgage liens on a property and protects the interests of lenders. These agreements may vary based on the type of property and the specific needs of the parties involved.

Philadelphia Pennsylvania Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Philadelphia Pennsylvania Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Preparing legal documentation can be difficult. In addition, if you decide to ask an attorney to write a commercial contract, papers for proprietorship transfer, pre-marital agreement, divorce papers, or the Philadelphia Subordination Agreement Subordinating Existing Mortgage to New Mortgage, it may cost you a fortune. So what is the best way to save time and money and draw up legitimate forms in total compliance with your state and local laws? US Legal Forms is a perfect solution, whether you're looking for templates for your personal or business needs.

US Legal Forms is biggest online catalog of state-specific legal documents, providing users with the up-to-date and professionally checked templates for any scenario gathered all in one place. Therefore, if you need the recent version of the Philadelphia Subordination Agreement Subordinating Existing Mortgage to New Mortgage, you can easily locate it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and pick the sample using the Download button. If you haven't subscribed yet, here's how you can get the Philadelphia Subordination Agreement Subordinating Existing Mortgage to New Mortgage:

- Look through the page and verify there is a sample for your region.

- Examine the form description and use the Preview option, if available, to make sure it's the template you need.

- Don't worry if the form doesn't satisfy your requirements - search for the correct one in the header.

- Click Buy Now when you find the required sample and choose the best suitable subscription.

- Log in or sign up for an account to pay for your subscription.

- Make a payment with a credit card or through PayPal.

- Choose the document format for your Philadelphia Subordination Agreement Subordinating Existing Mortgage to New Mortgage and save it.

Once finished, you can print it out and complete it on paper or import the template to an online editor for a faster and more practical fill-out. US Legal Forms allows you to use all the documents ever obtained many times - you can find your templates in the My Forms tab in your profile. Give it a try now!

Form popularity

FAQ

The lender might require a subordination agreement to protect its interests should the borrower place additional liens against the property, such as if she were to take out a second mortgage. The "junior" or second debt is referred to as a subordinated debt.

Purpose of a Subordination Agreement A subordination agreement is generally used when there are two mortgages and the mortgagor needs to refinance the first mortgage. It acknowledges that one party's interest or claim is superior to another in case the borrower's assets need to be liquidated to repay debts.

A second mortgage will become a subordinate loan. If you repay the primary loan within the term of the second mortgage, then the second mortgage can take its place as the primary loan.

The most common type of subordinate lien is a second mortgage. When you get a second mortgage loan, the lender records the lien, representing its claim on the collateral: your real estate. Because your first mortgage provider has the first claim on the property, the second mortgage is considered a subordinate lien.

A subordinated loan is debt that's only paid off after all primary loans are paid off, if there's any money left. It's also known as subordinated debt, junior debt or a junior security, while primary loans are also known as senior or unsubordinated debt.

Still, there are situations in which your first mortgage may be placed in a subordinate position, whether by your request (and your lender's agreement) or by law. Any mortgages that are recorded after your first purchase loan are usually subordinate loans.

When you take out a mortgage loan, the lender will likely include a subordination clause. Within this clause, the lender essentially states that their lien will take precedence over any other liens placed on the house. A subordination clause serves to protect the lender in case you default.

Subordination is the process of ranking home loans (mortgage, HELOC or home equity loan) by order of importance. When you have a home equity line of credit, for example, you actually have two loans your mortgage and HELOC. Both are secured by the collateral in your home at the same time.

You can transfer a mortgage to another person if the terms of your mortgage say that it is assumable. If you have an assumable mortgage, the new borrower can pay a flat fee to take over the existing mortgage and become responsible for payment. But they'll still typically need to qualify for the loan with your lender.

Subordinate Mortgage Loan Modification If the amount you're paying doesn't match the amount on your credit report, you'll need to provide a subordination agreement with the modified loan or a copy of the modification agreement that shows your payment amount.