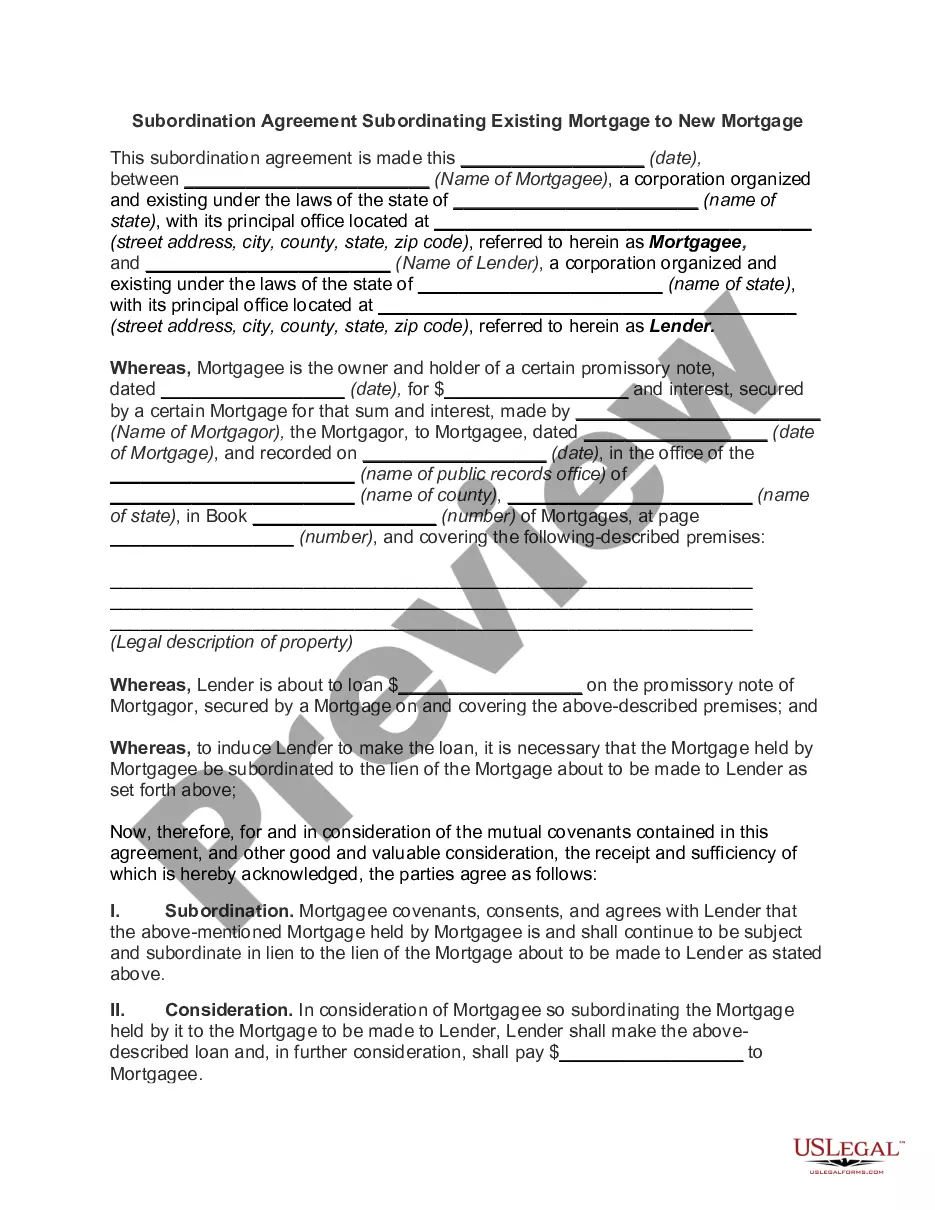

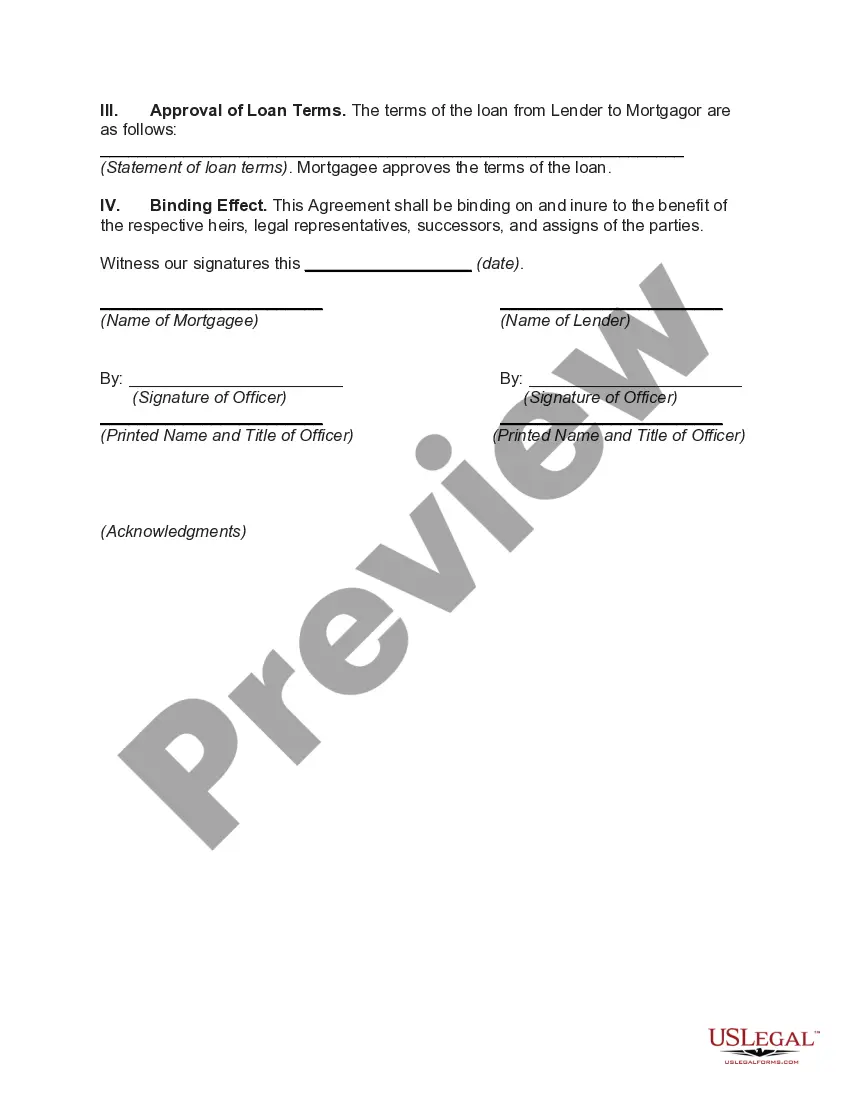

A San Bernardino California subordination agreement is a legal document that allows a property owner to prioritize or "subordinate" a new mortgage over their existing mortgage. This agreement is typically used during refinancing or when obtaining a second mortgage or home equity line of credit. By subordinating the existing mortgage, the property owner agrees to place the new mortgage in a superior position, meaning it will take priority over the original mortgage in terms of repayment and foreclosure rights. This is necessary because lenders often require first lien position on the property, giving them the highest claim in case of default. There are a few different types of San Bernardino California subordination agreements that may be used, namely: 1. First Lien Subordination Agreement: This type of agreement is entered when a property owner has an existing mortgage and wants to take on a new first mortgage. The original lender must agree to subordinate their lien, allowing the new lender to hold the first lien position. 2. Second Lien Subordination Agreement: In situations where the property owner has an existing first mortgage and wants to obtain a second mortgage, a second lien subordination agreement is used. The original lender agrees to subordinate their position to the new lender, who will hold the second lien. 3. Home Equity Line of Credit (HELOT) Subordination Agreement: When a property owner wants to open a HELOT but already has an existing mortgage, a HELOT subordination agreement is required. This agreement allows the HELOT lender to hold a subordinate lien position behind the existing mortgage. These San Bernardino California subordination agreements ensure that all relevant parties are aware of the new mortgage's priority and that the property owner can move forward with obtaining additional funding. It is essential to consult with an experienced real estate attorney or mortgage professional to ensure the legality and effectiveness of the subordination agreement.

San Bernardino California Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out San Bernardino California Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Laws and regulations in every area differ from state to state. If you're not a lawyer, it's easy to get lost in a variety of norms when it comes to drafting legal paperwork. To avoid costly legal assistance when preparing the San Bernardino Subordination Agreement Subordinating Existing Mortgage to New Mortgage, you need a verified template valid for your county. That's when using the US Legal Forms platform is so advantageous.

US Legal Forms is a trusted by millions online collection of more than 85,000 state-specific legal forms. It's an excellent solution for specialists and individuals searching for do-it-yourself templates for various life and business situations. All the forms can be used multiple times: once you obtain a sample, it remains available in your profile for subsequent use. Thus, if you have an account with a valid subscription, you can just log in and re-download the San Bernardino Subordination Agreement Subordinating Existing Mortgage to New Mortgage from the My Forms tab.

For new users, it's necessary to make several more steps to obtain the San Bernardino Subordination Agreement Subordinating Existing Mortgage to New Mortgage:

- Analyze the page content to make sure you found the right sample.

- Take advantage of the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your requirements.

- Use the Buy Now button to obtain the document once you find the appropriate one.

- Choose one of the subscription plans and log in or create an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Fill out and sign the document in writing after printing it or do it all electronically.

That's the easiest and most cost-effective way to get up-to-date templates for any legal reasons. Find them all in clicks and keep your paperwork in order with the US Legal Forms!

Form popularity

FAQ

Legal Concept of First in Time, First in Right Mortgage liens generally follow the ""first in time, first in right" rule. As described above, this general rule says that whichever lien is recorded first in the land records has higher priority than later recorded liens.

Despite its technical-sounding name, the subordination agreement has one simple purpose. It assigns your new mortgage to first lien position, making it possible to refinance with a home equity loan or line of credit. Signing your agreement is a positive step forward in your refinancing journey.

A second mortgage will become a subordinate loan. If you repay the primary loan within the term of the second mortgage, then the second mortgage can take its place as the primary loan.

A second mortgage is a lien taken out against a property that already has a home loan on it. A lien is a right to possess and seize property under specific circumstances. In other words, your lender has the right to take control of your home if you default on your loan.

The most common type of subordinate lien is a second mortgage. When you get a second mortgage loan, the lender records the lien, representing its claim on the collateral: your real estate. Because your first mortgage provider has the first claim on the property, the second mortgage is considered a subordinate lien.

When you take out a mortgage loan, the lender will likely include a subordination clause. Within this clause, the lender essentially states that their lien will take precedence over any other liens placed on the house. A subordination clause serves to protect the lender in case you default.

When you take out a mortgage loan, the lender will likely include a subordination clause. Within this clause, the lender essentially states that their lien will take precedence over any other liens placed on the house. A subordination clause serves to protect the lender in case you default.

There are many examples of subordinate financing, but some of the most common include: Home Equity Loan. Home equity loans are a type of second mortgage and are taken out against the equity that you have built up in the home.Home Equity Line of Credit (HELOC).Other Second Mortgages.

What is a Subordinate Mortgage? Subordinate mortgages are loans that have a lower priority status than any other recorded liens (or debts) against a property. When you get the loan you need to purchase your home, this loan is typically recorded as the first repayment priority on your deed after closing.

The lender might require a subordination agreement to protect its interests should the borrower place additional liens against the property, such as if she were to take out a second mortgage. The "junior" or second debt is referred to as a subordinated debt.