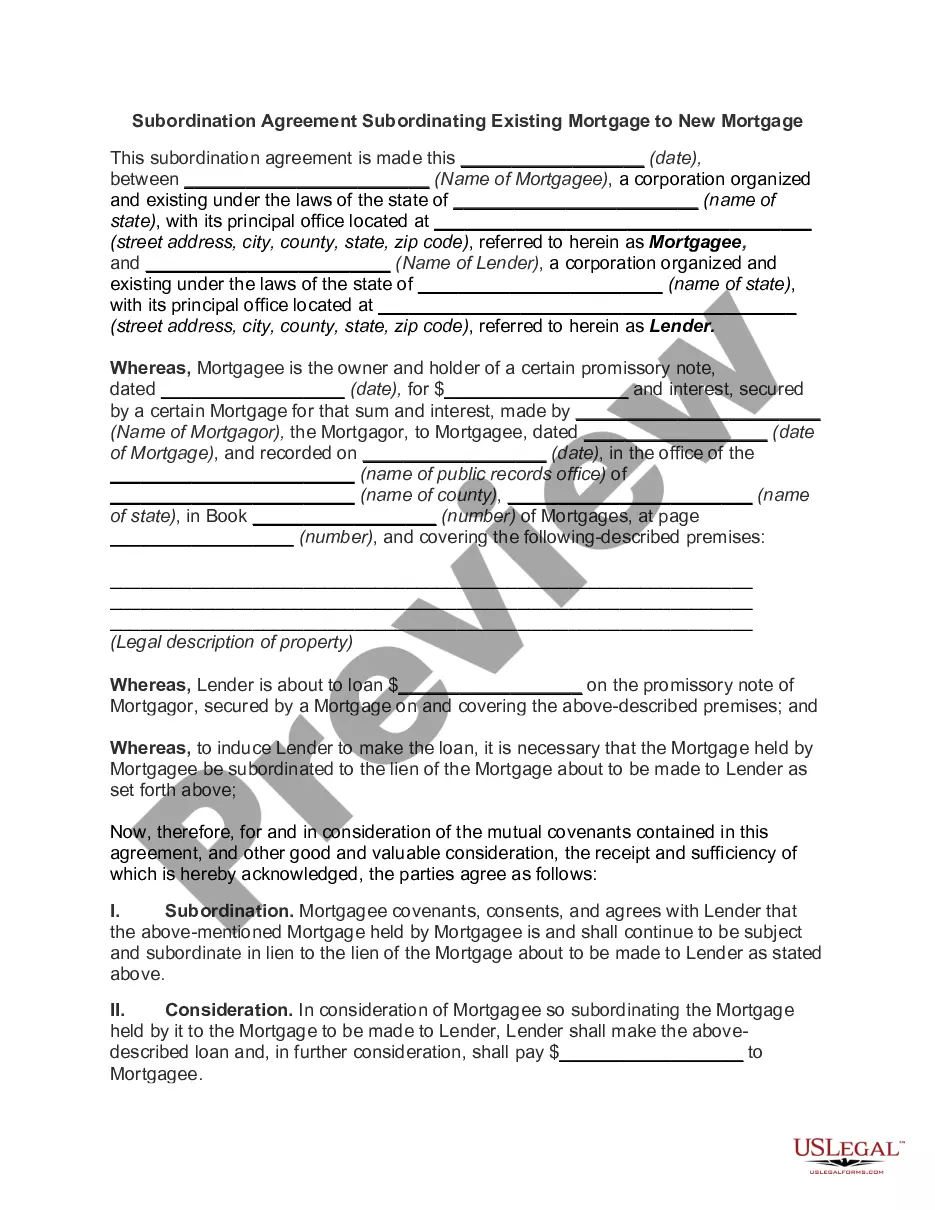

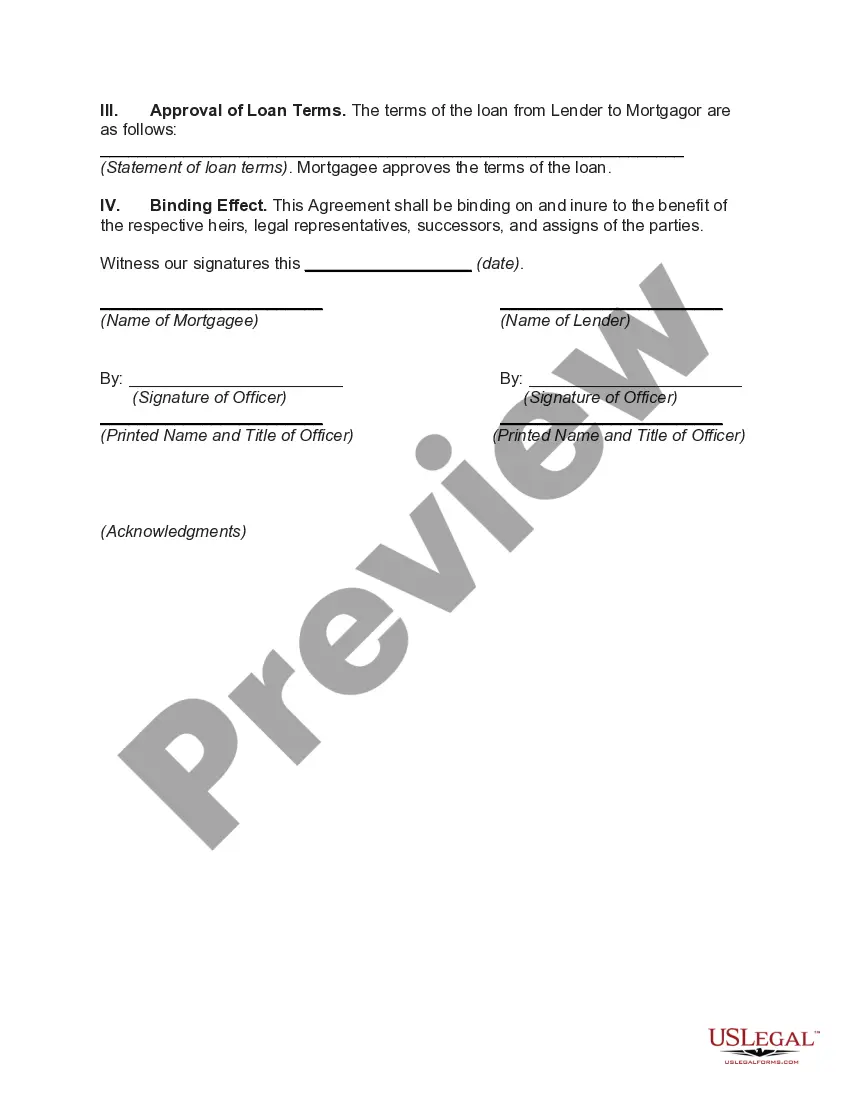

A Travis Texas Subordination Agreement Subordinating Existing Mortgage to New Mortgage is a legally binding document that outlines the process of reorganizing the priority of mortgage loans on a property. This agreement is commonly used when a borrower wishes to obtain a new mortgage while still having an existing mortgage in place. By subordinating the existing mortgage to the new one, the lender of the new mortgage gains priority in terms of repayment if the property is sold or foreclosed upon. In Travis County, Texas, there are a few different types of subordination agreements pertaining to mortgage loans: 1. First Lien Subordination Agreement: This type of agreement is typically used when the borrower wants to refinance their existing mortgage loan with a new lender but wants to maintain the first lien position of the original mortgage. By signing this agreement, the borrower allows the new lender to take priority over the existing mortgage while still keeping the original mortgage intact. 2. Second Lien Subordination Agreement: In some cases, a homeowner may want to take out a second mortgage, also known as a home equity loan, but needs to subordinate this new loan to the first mortgage. By signing a second lien subordination agreement, the borrower allows the new lender to take a subordinate position to the existing mortgage, ensuring that the first mortgage remains the primary lien. 3. Intercreditor Agreement: This type of subordination agreement is often used when there are multiple mortgages or liens on a property. An intercreditor agreement establishes the priority of repayment among the creditors and typically outlines the conditions under which the subordination takes effect. This agreement is crucial when there is a need to ensure a clear hierarchy of payments in the event of financial distress or default. Overall, a Travis Texas Subordination Agreement Subordinating Existing Mortgage to New Mortgage serves as a means to reorganize the priority of mortgage loans on a property, enabling borrowers to access new financing opportunities while maintaining the integrity of existing mortgages. It legally protects the interests of lenders and borrowers and clarifies the order of repayment in various scenarios.

Travis Texas Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Travis Texas Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

Drafting documents for the business or personal demands is always a big responsibility. When creating an agreement, a public service request, or a power of attorney, it's important to take into account all federal and state regulations of the specific area. Nevertheless, small counties and even cities also have legislative provisions that you need to consider. All these details make it stressful and time-consuming to draft Travis Subordination Agreement Subordinating Existing Mortgage to New Mortgage without professional assistance.

It's possible to avoid wasting money on attorneys drafting your paperwork and create a legally valid Travis Subordination Agreement Subordinating Existing Mortgage to New Mortgage by yourself, using the US Legal Forms online library. It is the most extensive online catalog of state-specific legal templates that are professionally verified, so you can be certain of their validity when picking a sample for your county. Earlier subscribed users only need to log in to their accounts to download the required document.

If you still don't have a subscription, follow the step-by-step guideline below to obtain the Travis Subordination Agreement Subordinating Existing Mortgage to New Mortgage:

- Look through the page you've opened and check if it has the sample you require.

- To do so, use the form description and preview if these options are available.

- To locate the one that fits your requirements, use the search tab in the page header.

- Double-check that the template complies with juridical standards and click Buy Now.

- Opt for the subscription plan, then sign in or register for an account with the US Legal Forms.

- Utilize your credit card or PayPal account to pay for your subscription.

- Download the selected document in the preferred format, print it, or complete it electronically.

The exceptional thing about the US Legal Forms library is that all the paperwork you've ever acquired never gets lost - you can access it in your profile within the My Forms tab at any time. Join the platform and quickly obtain verified legal forms for any use case with just a few clicks!