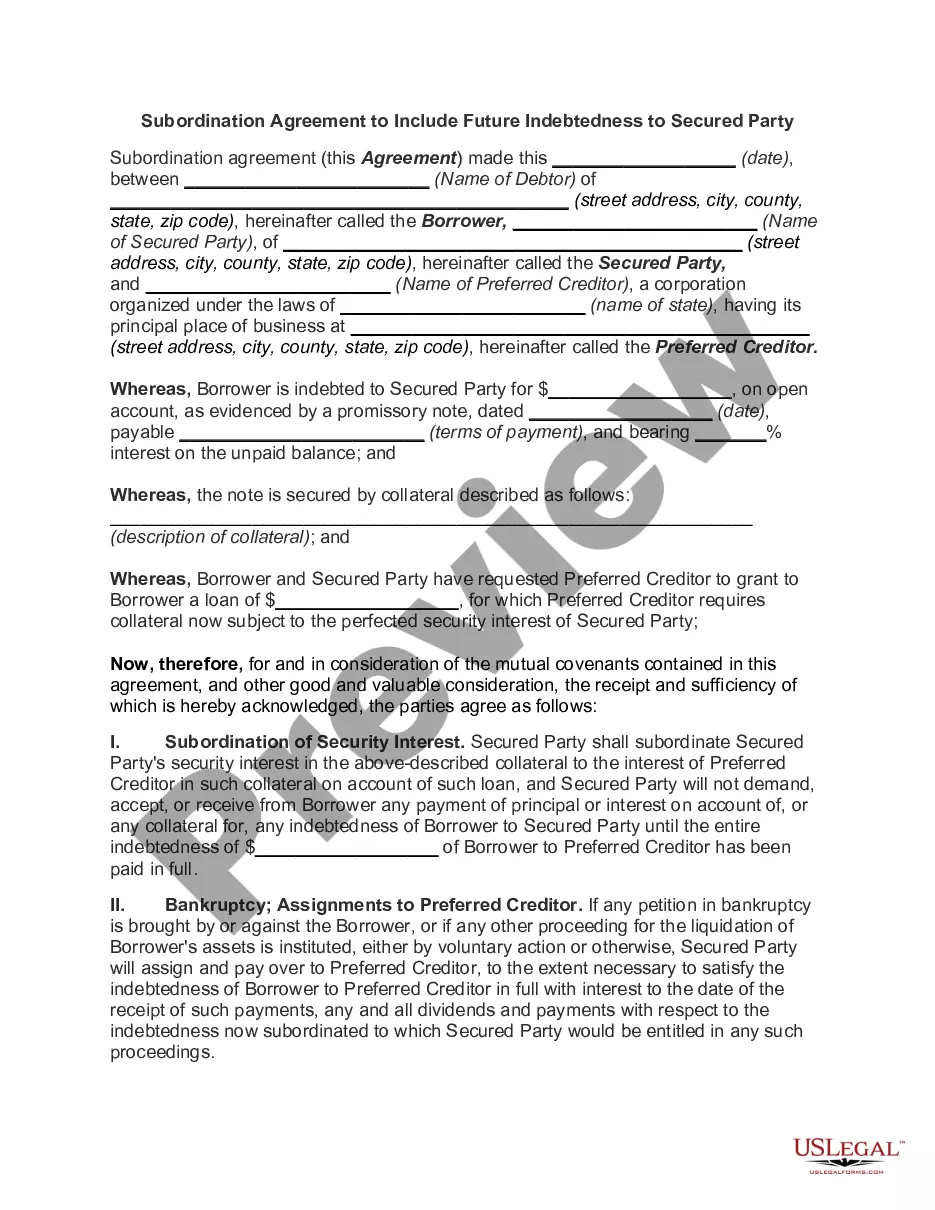

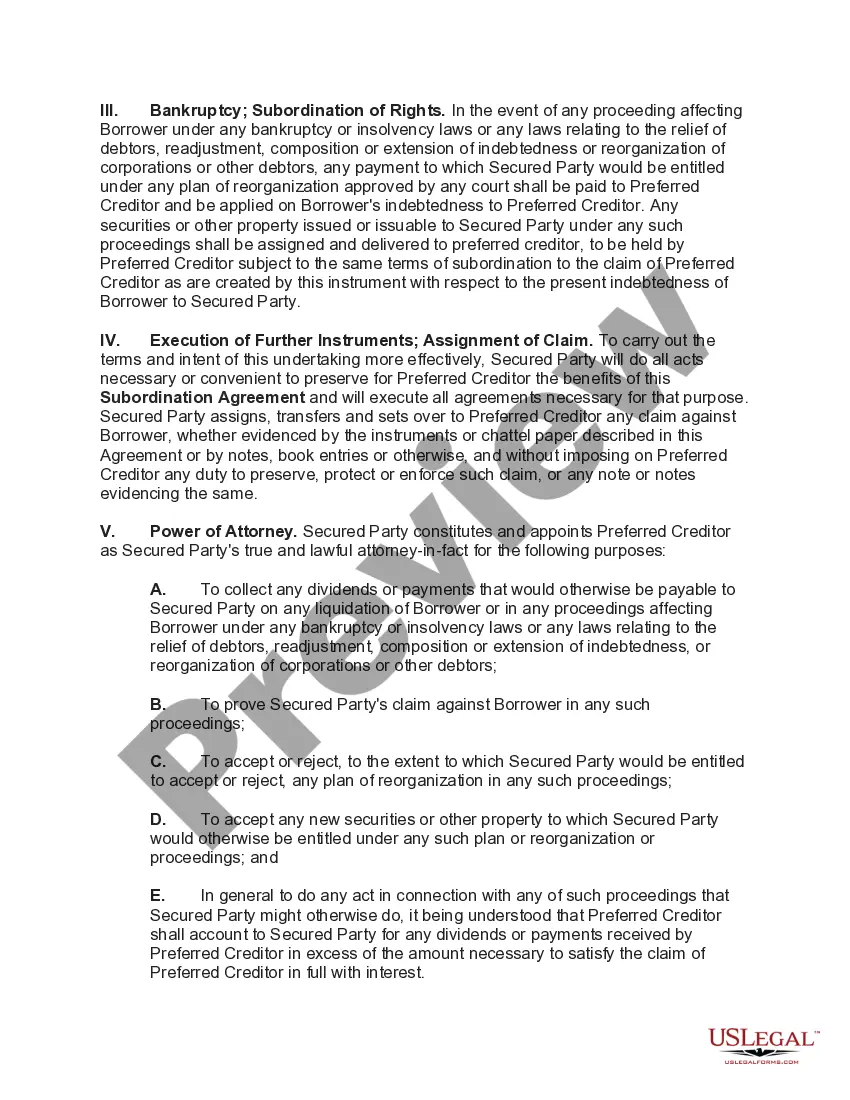

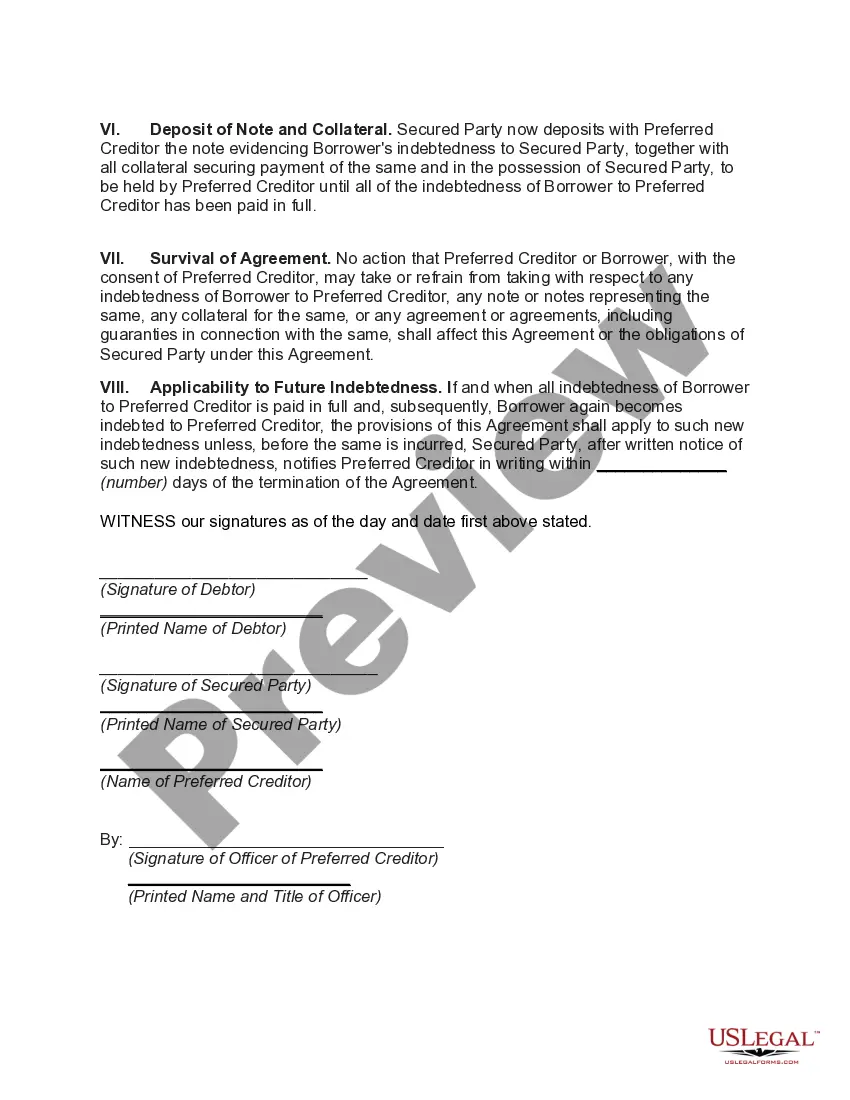

Fairfax Virginia Subordination Agreement to Include Future Indebtedness to Secured Party is a legal document that outlines the rights and obligations between multiple parties involved in a financial transaction. This agreement is commonly used in Fairfax, Virginia, to specify the priority of repayment in case of default or bankruptcy. A Subordination Agreement pertains to the subordination of one creditor's claim to another. In this case, it refers to the subordinated lender agreeing to allow a primary or senior lender to have a higher priority claim over certain assets or collaterals if the borrower defaults on their debt obligations. The purpose of this agreement is to protect the interests of the secured party, usually a lender or financial institution, by ensuring that their claim takes precedence over future indebtedness to other parties. By signing this agreement, the subordinated lender recognizes and accepts a subordinate position with respect to any future loans or credit facilities obtained by the borrower. There are various types of Fairfax Virginia Subordination Agreements to Include Future Indebtedness to Secured Party, which can be categorized based on their nature or specific clauses. These types may include: 1. General Subordination Agreement: This is the most common type of Fairfax Virginia Subordination Agreement. It allows the senior creditor to have priority over any future loans or debts obtained by the borrower. It explicitly states that the subordinated creditor agrees to subordinate their claim to any future indebtedness to the secured party. 2. Specific-Debt Subordination Agreement: This type of agreement focuses on subordinating a particular debt or loan. It may arise when the borrower is seeking additional financing while keeping one specific loan separate from the subordination agreement. 3. Partial Subordination Agreement: In some cases, a subordinated creditor might not agree to fully subordinate all indebtedness. Instead, they may agree to partially subordinate a specific portion of the debt, while maintaining priority over the remainder. 4. Deed of Subordination: This is a type of Fairfax Virginia Subordination Agreement that deals with real estate transactions. It allows the senior lien holder to maintain the first priority claim on a property, even if additional financing or liens are placed on it. In conclusion, Fairfax Virginia Subordination Agreement to Include Future Indebtedness to Secured Party is an essential legal document that ensures the senior creditor's priority in case of default or bankruptcy. By subordinating their claim, the subordinated lender allows the secured party to have a higher priority in the repayment chain. Understanding the various types of subordination agreements can help parties involved protect their interests and ensure a smooth flow of financial transactions.

Fairfax Virginia Subordination Agreement to Include Future Indebtedness to Secured Party

Description

How to fill out Fairfax Virginia Subordination Agreement To Include Future Indebtedness To Secured Party?

A document routine always goes along with any legal activity you make. Staring a business, applying or accepting a job offer, transferring property, and many other life scenarios require you prepare formal paperwork that differs from state to state. That's why having it all accumulated in one place is so valuable.

US Legal Forms is the largest online collection of up-to-date federal and state-specific legal templates. On this platform, you can easily locate and download a document for any personal or business purpose utilized in your county, including the Fairfax Subordination Agreement to Include Future Indebtedness to Secured Party.

Locating samples on the platform is extremely straightforward. If you already have a subscription to our library, log in to your account, find the sample using the search bar, and click Download to save it on your device. After that, the Fairfax Subordination Agreement to Include Future Indebtedness to Secured Party will be available for further use in the My Forms tab of your profile.

If you are dealing with US Legal Forms for the first time, adhere to this quick guideline to obtain the Fairfax Subordination Agreement to Include Future Indebtedness to Secured Party:

- Ensure you have opened the right page with your regional form.

- Utilize the Preview mode (if available) and browse through the sample.

- Read the description (if any) to ensure the template corresponds to your requirements.

- Search for another document using the search tab if the sample doesn't fit you.

- Click Buy Now once you find the required template.

- Select the suitable subscription plan, then sign in or register for an account.

- Choose the preferred payment method (with credit card or PayPal) to continue.

- Opt for file format and save the Fairfax Subordination Agreement to Include Future Indebtedness to Secured Party on your device.

- Use it as needed: print it or fill it out electronically, sign it, and send where requested.

This is the simplest and most trustworthy way to obtain legal documents. All the samples available in our library are professionally drafted and checked for correspondence to local laws and regulations. Prepare your paperwork and run your legal affairs effectively with the US Legal Forms!