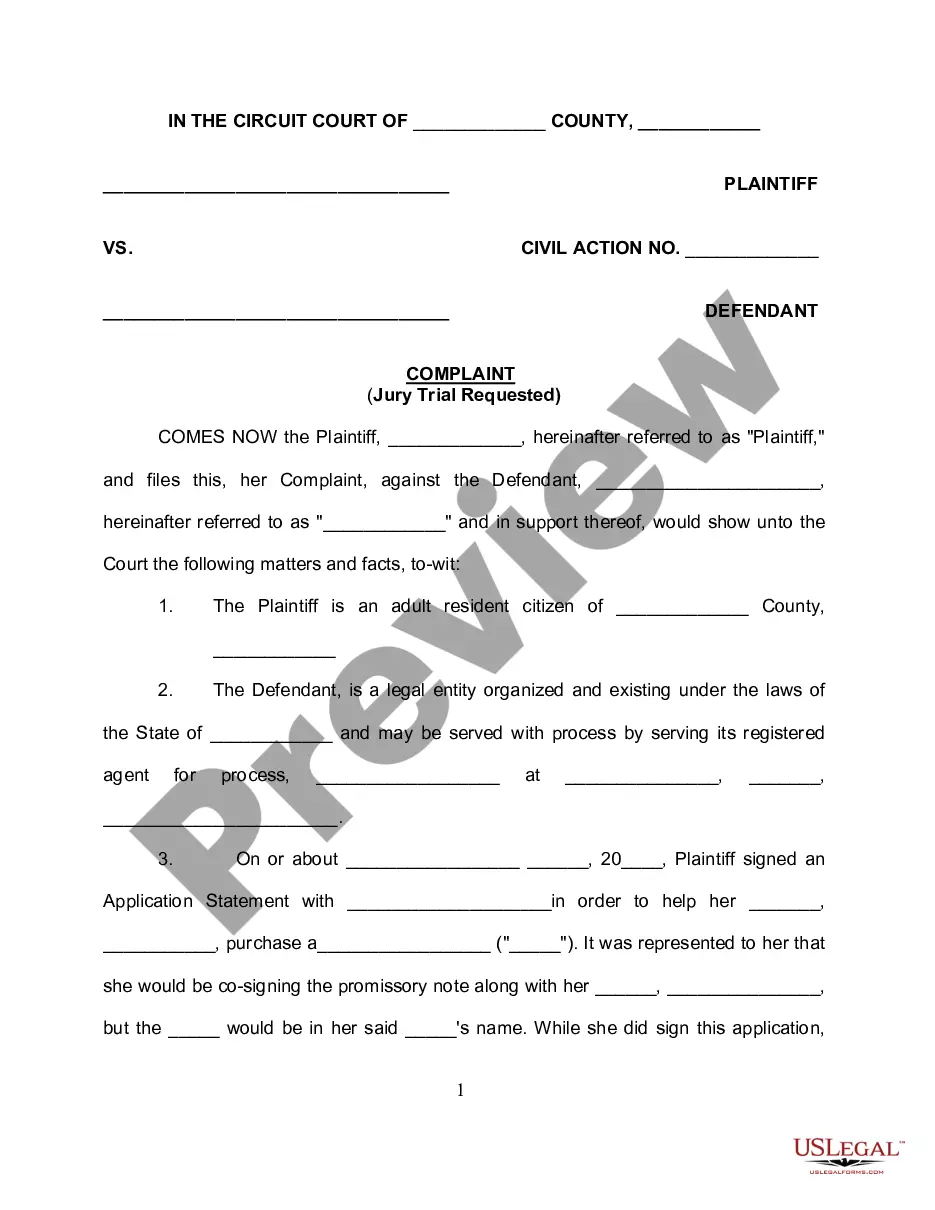

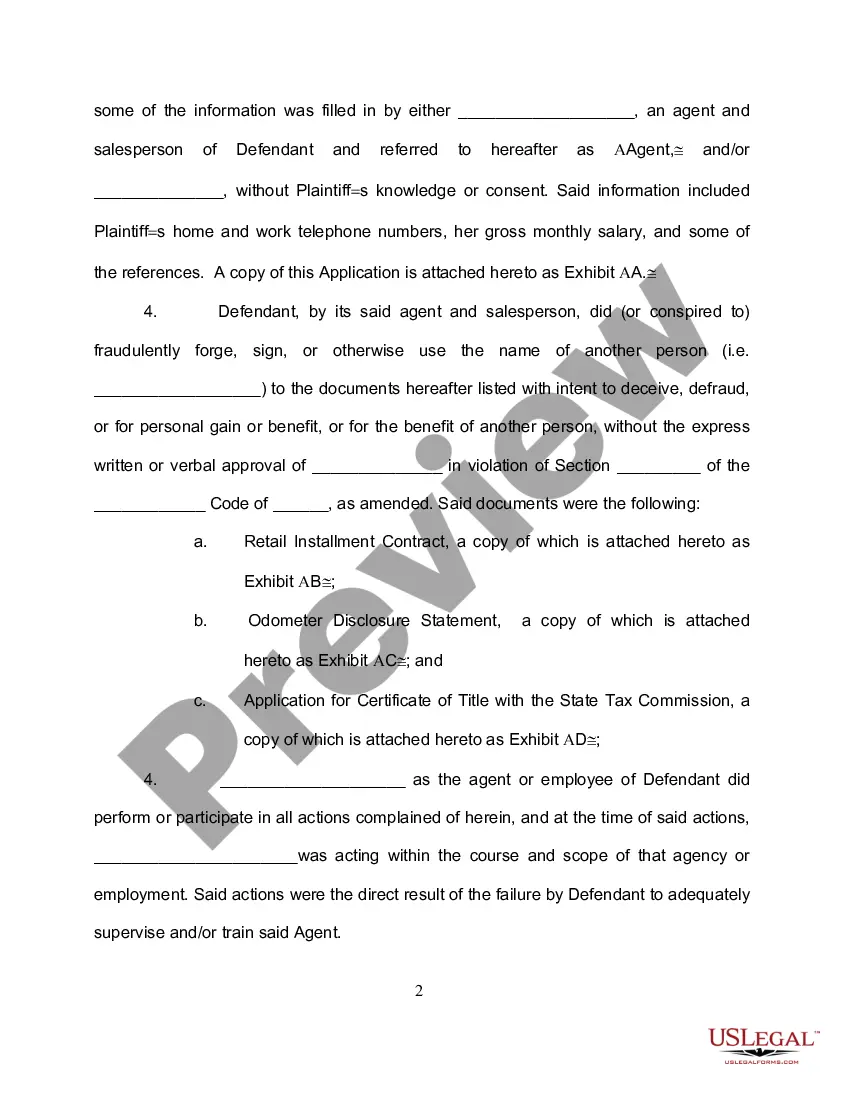

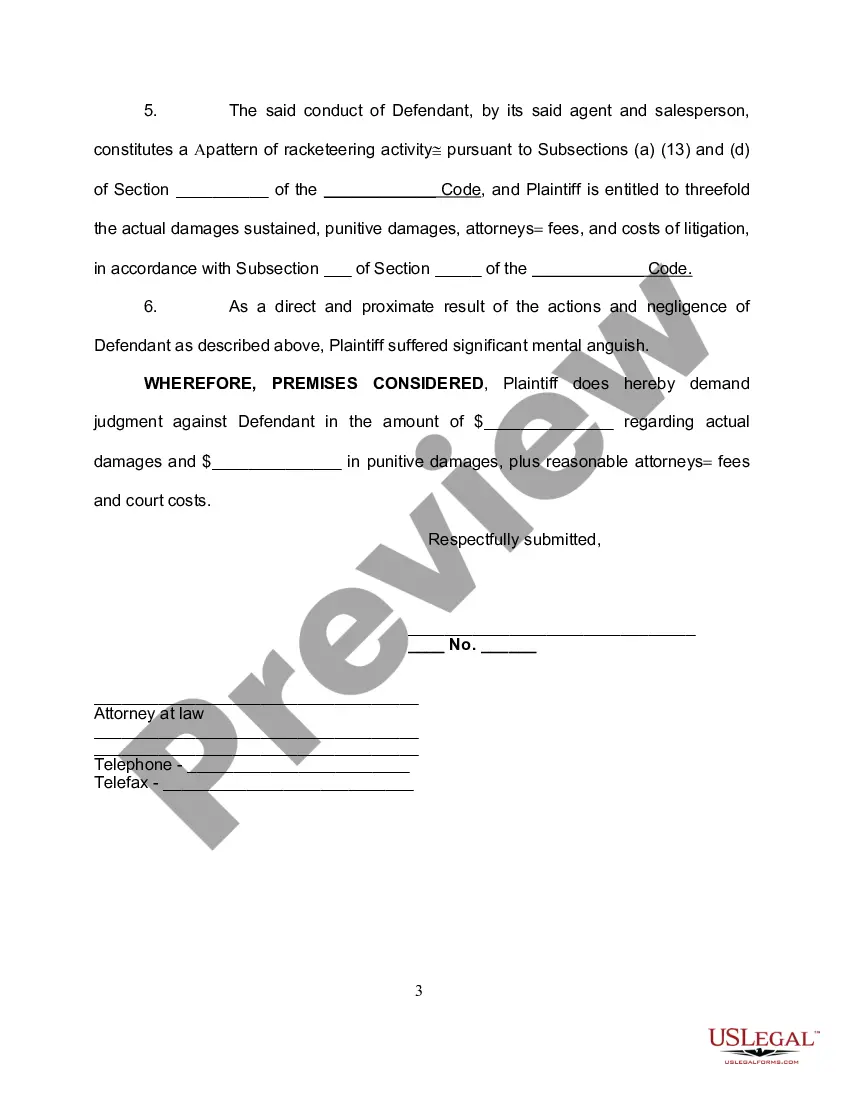

Title: Understanding Phoenix Arizona Complaint for Impropriety Involving Loan Application Keywords: Phoenix Arizona, complaint, impropriety, loan application In Phoenix, Arizona, individuals may file a formal complaint for impropriety involving loan applications to address any misconduct or unfair practices they have experienced throughout the loan application process. These complaints aim to protect borrowers' rights and ensure that lenders adhere to legal and ethical standards. Let's explore in detail what such complaints entail and the potential types associated with them. 1. Allegations of Misrepresentation: This type of complaint arises when the borrower suspects that the lender deliberately misrepresented crucial information related to the loan application process. This can include, but is not limited to, fraudulent representation of loan terms, interest rates, fees, or any other pertinent details. 2. Documentation Errors: Borrowers may file a complaint if they believe that the lender mishandled or manipulated their loan application documents. This could involve instances where important documents were fabricated, missing, altered without consent, or incomplete, potentially affecting the borrower's ability to secure a fair loan. 3. Discrimination Complaint: If borrowers believe they were subjected to discriminatory practices during the loan application process, such as being denied a loan based on factors protected under federal laws (e.g., race, gender, religion, disability), they can file a complaint for impropriety. 4. Non-Disclosure of Information: This complaint category focuses on situations where lenders fail to disclose crucial loan details to borrowers. If borrowers were not adequately informed about important terms, conditions, or potential risks associated with the loan application, they can raise concerns regarding non-disclosure. 5. Privacy Concerns: Borrowers may encounter instances where their personal or financial information is improperly handled or misused during the loan application process. Complaints surrounding privacy impropriety involve unauthorized sharing, selling, or unauthorized access to sensitive borrower information. 6. Unfair Collection Practices: In some cases, borrowers file complaints for impropriety against lenders who engage in unethical or illegal collections practices after the loan application process. This might involve harassment, threats, or deceptive tactics employed by lenders or collection agencies to recover loan payments. 7. Failure to Provide Proper Guidance: Borrowers may file complaints when lenders or loan officers fail to provide appropriate guidance throughout the loan application process. This can encompass lack of clarity or proper disclosure of the loan terms, leading to misunderstandings or misinterpretations that detrimentally impact the borrower. 8. General Misconduct: This category covers any additional complaints related to impropriety in loan applications that do not fall under the specific types mentioned above. It encompasses various situations where borrowers feel that the lender has engaged in unethical or improper practices throughout the loan application process. Conclusion: A Phoenix Arizona complaint for impropriety involving a loan application provides borrowers with a mechanism to address unfair, discriminatory, or unethical practices by lenders. By filing such complaints, borrowers aim to safeguard their rights, expose misconduct, and seek resolution. It is important for borrowers to understand their rights and consult legal professionals with expertise in consumer protection and loan-related matters for guidance in such situations.

Phoenix Arizona Complaint for Impropriety Involving Loan Application

Description

How to fill out Phoenix Arizona Complaint For Impropriety Involving Loan Application?

Dealing with legal forms is a must in today's world. However, you don't always need to seek qualified assistance to create some of them from the ground up, including Phoenix Complaint for Impropriety Involving Loan Application, with a service like US Legal Forms.

US Legal Forms has more than 85,000 templates to choose from in different types ranging from living wills to real estate papers to divorce documents. All forms are organized according to their valid state, making the searching experience less challenging. You can also find detailed materials and guides on the website to make any activities associated with document execution simple.

Here's how to purchase and download Phoenix Complaint for Impropriety Involving Loan Application.

- Take a look at the document's preview and description (if available) to get a basic information on what you’ll get after getting the form.

- Ensure that the document of your choosing is specific to your state/county/area since state regulations can impact the legality of some documents.

- Examine the similar document templates or start the search over to locate the right document.

- Hit Buy now and create your account. If you already have an existing one, choose to log in.

- Pick the option, then a suitable payment gateway, and buy Phoenix Complaint for Impropriety Involving Loan Application.

- Select to save the form template in any available format.

- Go to the My Forms tab to re-download the document.

If you're already subscribed to US Legal Forms, you can locate the appropriate Phoenix Complaint for Impropriety Involving Loan Application, log in to your account, and download it. Of course, our platform can’t take the place of a legal professional entirely. If you have to deal with an exceptionally complicated situation, we recommend getting an attorney to review your form before executing and filing it.

With more than 25 years on the market, US Legal Forms proved to be a go-to platform for various legal forms for millions of customers. Become one of them today and get your state-compliant paperwork with ease!