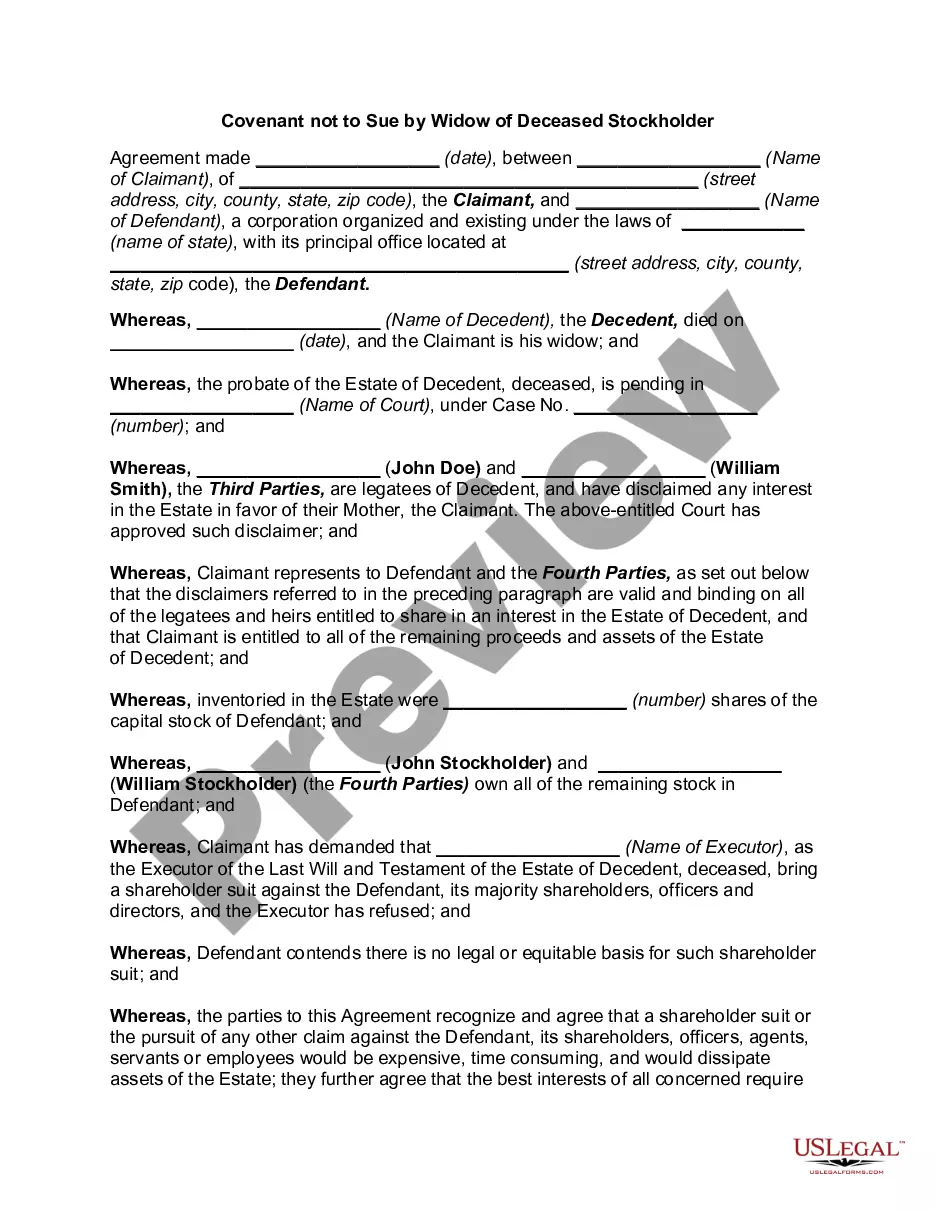

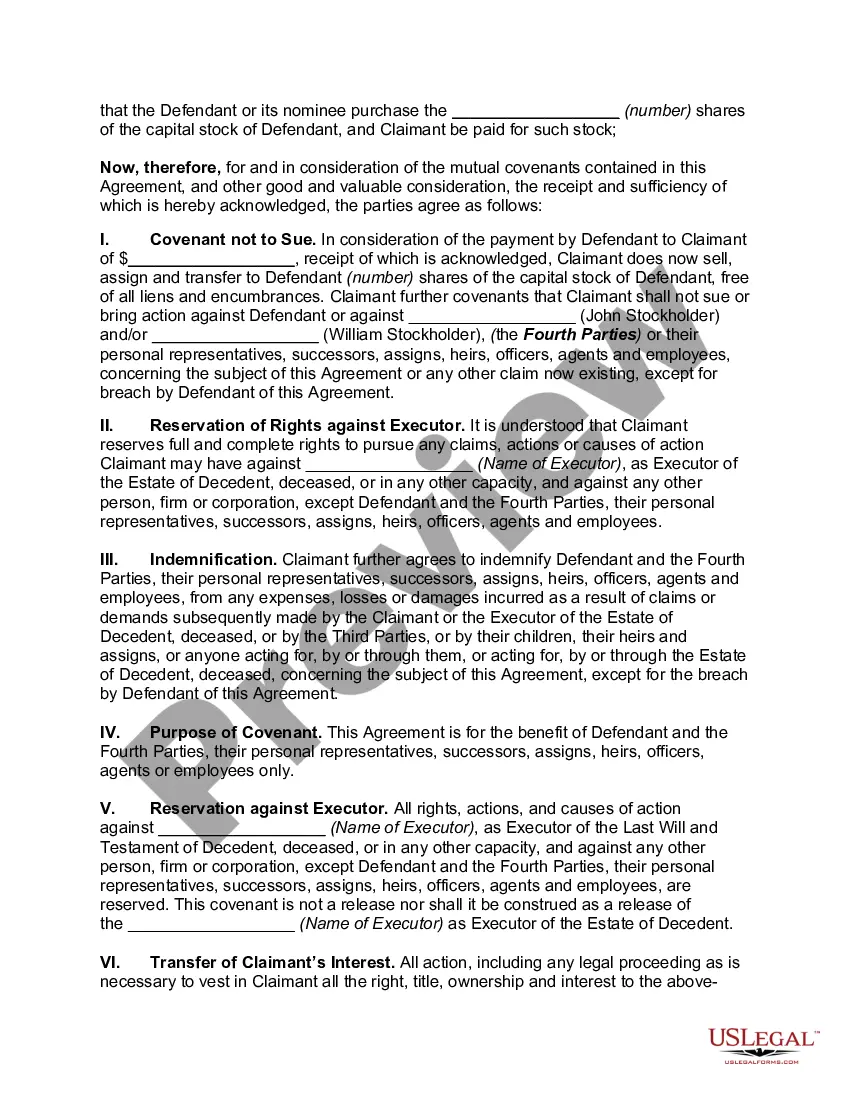

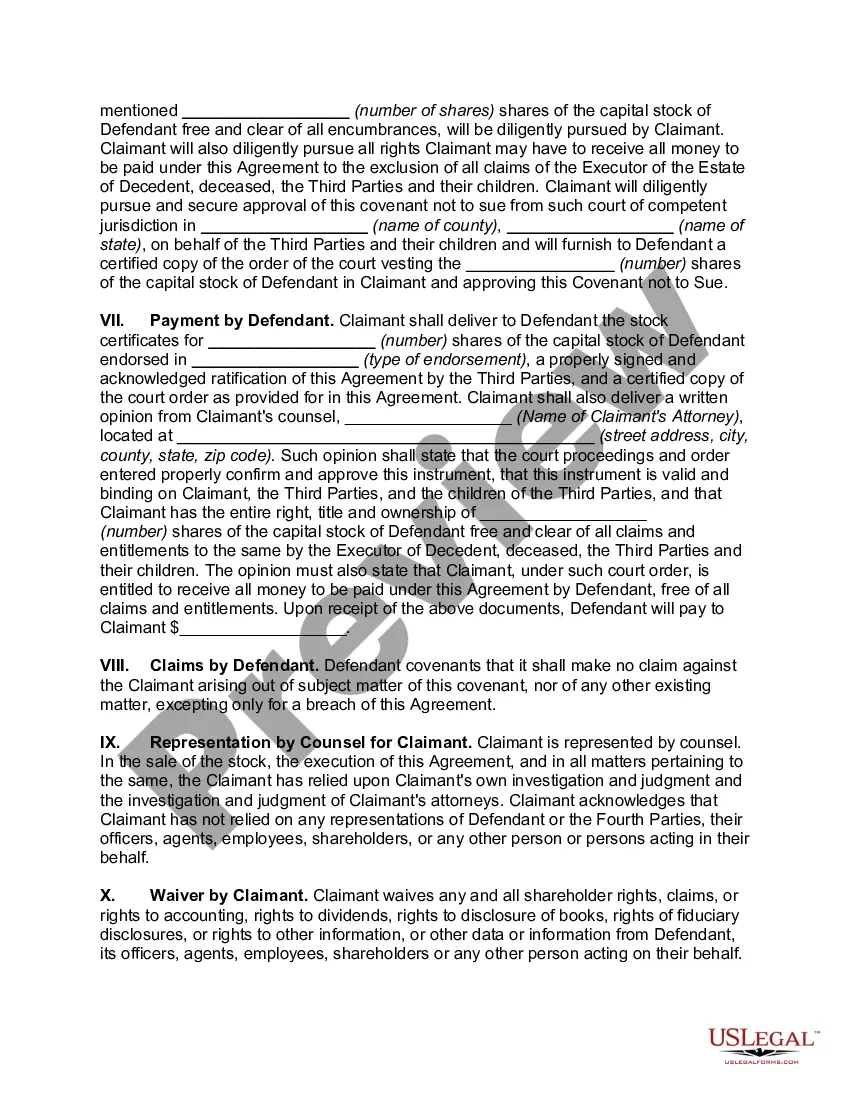

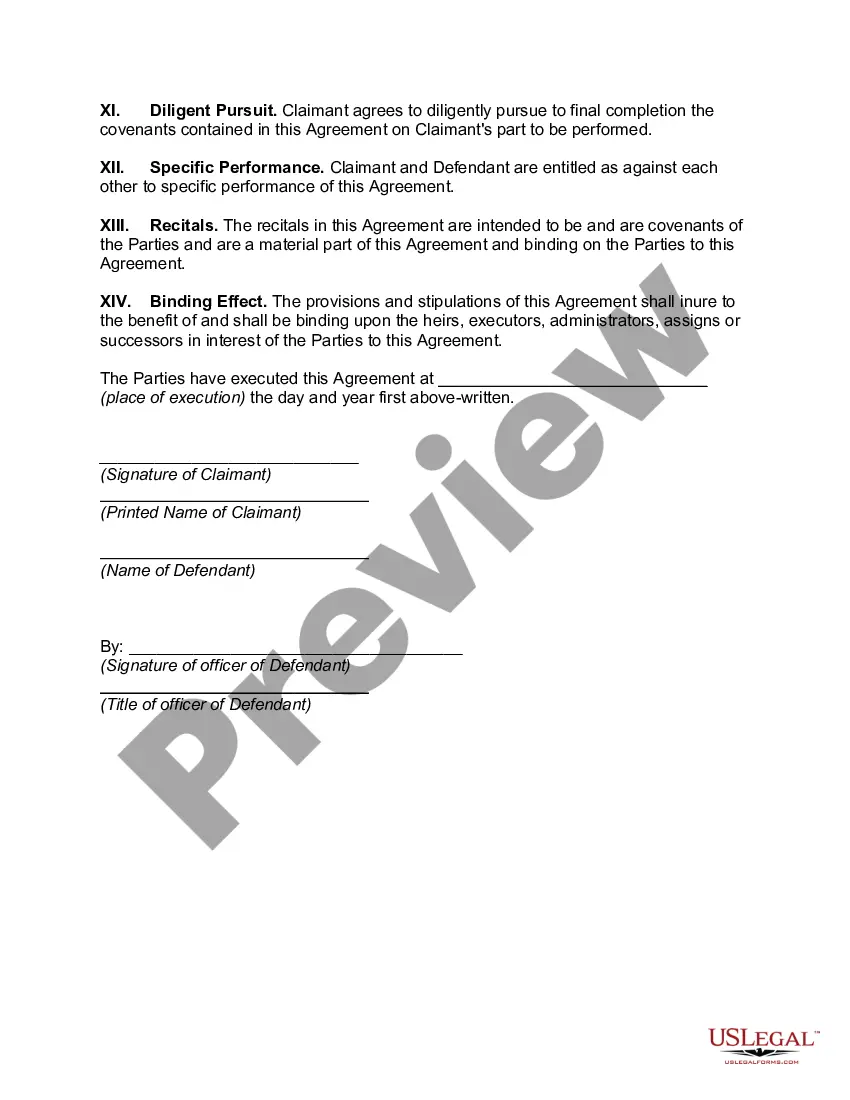

Miami-Dade Florida Covenant Not to Sue by Widow of Deceased Stockholder: A Comprehensive Guide Keywords: Miami-Dade Florida, covenant not to sue, widow, deceased stockholder, legal agreement, shareholder rights, inheritance, dispute resolution Introduction: A Miami-Dade Florida Covenant Not to Sue by Widow of Deceased Stockholder refers to a legally binding agreement entered into by the widow of a deceased stockholder, specifically in the Miami-Dade County area of Florida. This agreement aims to outline the terms and conditions that govern the resolution of any potential legal disputes or claims related to the deceased stockholder's assets, inheritance, or shareholder rights. Types of Miami-Dade Florida Covenant Not to Sue by Widow of Deceased Stockholder: 1. Estate Distribution Covenant: This type of covenant focuses on the fair and equitable distribution of the deceased stockholder's estate among the heirs, including the widow. It aims to prevent any potential lawsuits or disputes that may arise regarding the allocation of assets. 2. Shareholder Rights Covenant: In situations where the deceased stockholder held shares in a company or corporation, this covenant aims to clarify the widow's rights and responsibilities as a shareholder. It ensures that the widow can exercise their rights without facing unnecessary legal hurdles. 3. Dispute Resolution Covenant: This specific type of covenant focuses on establishing a framework for resolving any disputes that may arise among the widow and other beneficiaries or stakeholders of the deceased stockholder's estate. It provides guidelines for alternative dispute resolution methods, such as mediation or arbitration, before resorting to costly court proceedings. Key Elements of Miami-Dade Florida Covenant Not to Sue by Widow of Deceased Stockholder: 1. Consent and Agreement: The covenant starts with the explicit consent and agreement of the widow, acknowledging their understanding of the legal implications and the intent to resolve potential disputes amicably. 2. Release of Claims: The covenant reaffirms the widow's agreement to release any present or future claims against the estate, its assets, or any other beneficiaries or stakeholders involved. 3. Preservation of Rights: While releasing claims, the covenant should also detail the rights that the widow is entitled to, such as shares, dividends, or other financial benefits related to the deceased stockholder's investments. 4. Inheritance Acknowledgment: This section ensures that the widow recognizes and understands their share in the deceased stockholder's inheritance, including any additional arrangements made in the will or testament. 5. Dispute Resolution Process: The covenant outlines a step-by-step procedure for dispute resolution, empowering the parties involved to attempt mediation, negotiation, or arbitration before resorting to court proceedings. By emphasizing alternative methods, it aims to save time and costs. 6. Governing Law and Jurisdiction: To provide clarity on applicable regulations and to ensure a smooth resolution process, the covenant should specify the governing law (such as Florida law) and the appropriate jurisdiction (such as Miami-Dade County) for any legal actions. Conclusion: In Miami-Dade County, Florida, a Covenant Not to Sue by Widow of Deceased Stockholder serves as a crucial legal agreement that allows for the peaceful resolution of potential disputes related to estate distribution, shareholder rights, and inheritance. By establishing clear terms and offering alternative dispute resolution options, this covenant provides a framework for preserving the deceased stockholder's wishes while safeguarding the widow's rights and interests.

Miami-Dade Florida Covenant Not to Sue by Widow of Deceased Stockholder

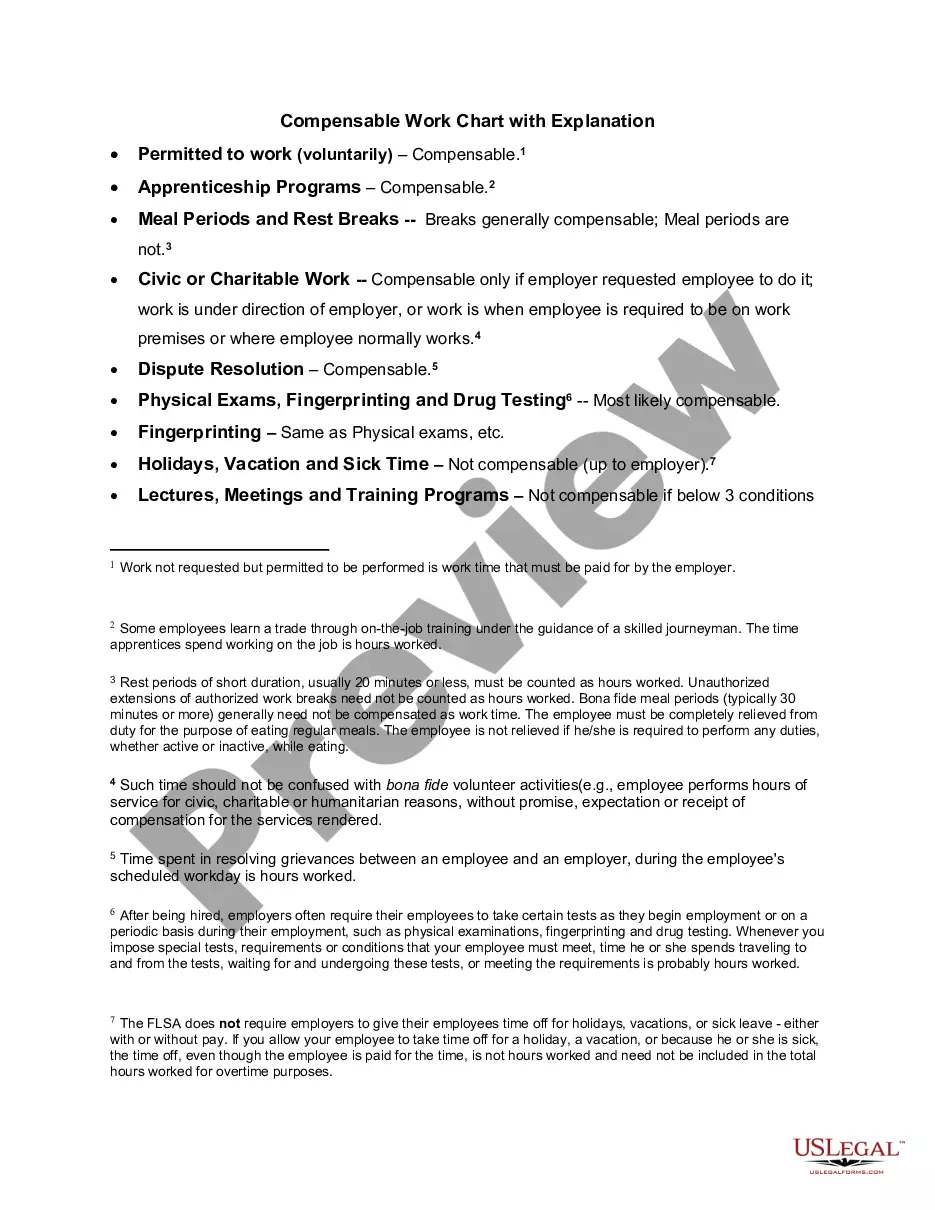

Description

Form popularity

FAQ

If an asset does not have a named beneficiary or rights of survivorship, it will have to go through probate to change ownership pursuant to the Florida Probate Rules (2022). The most common assets that go through this process are bank accounts, real estate, vehicles, and personal property.

Probate assets include, but are not limited to, the following: A bank account or investment account in the sole name of a decedent. A life insurance policy, annuity contract, or individual retirement account payable to the decedent's estate.

The deceased must have been a resident of Miami-Dade County at the time of death....You must submit: A certified copy of the death certificate. A copy of the itemized funeral contract. The receipt paid in full. A copy of any documentation of the decedent's assets. Applicable filing fees.

In Florida, the probate process is used to settle an estate, including all property, and assets of a deceased person. When a person dies, probate is required for any estate with non-exempt assets worth more than $75,000.

If you own the property alone under your individual name, then a will does dispose of the property at death. However, if you own the property as joint tenants with right of survivorship or as husband and wife, then the real property will pass outside of the will.

In most instances, there will need to be a court order to transfer the property. And in Florida, that means opening a probate. In Florida, probate is a court proceeding that is filed in the county where the deceased person last resided. The two types of probate are summary and formal.

An affidavit of heirs is a notarized document that identifies who inherits your property after you die. This document is often needed when an individual dies without a will or a living trust. When you die without a will, the court decides who receives your property by looking at state law.

(2) Exempt property shall consist of: (a) Household furniture, furnishings, and appliances in the decedent's usual place of abode up to a net value of $20,000 as of the date of death. (b) Two motor vehicles as defined in s.(c) All qualified tuition programs authorized by s.(d) All benefits paid pursuant to s.

If a Florida resident dies without a will, their property will pass to their closest relatives through the Florida intestate laws. Intestate laws set out a rigid formula for judges to distribute assets to family members to avoid a situation where the deceased person's assets end up with the state.

If a person passes away without a will or trust and has assets in their name ONLY, then probate is required to distribute property and monies. If property, bank accounts, insurance policies, annuities, 401K plans, and all assets have beneficiaries or joint owners, probate is unnecessary.