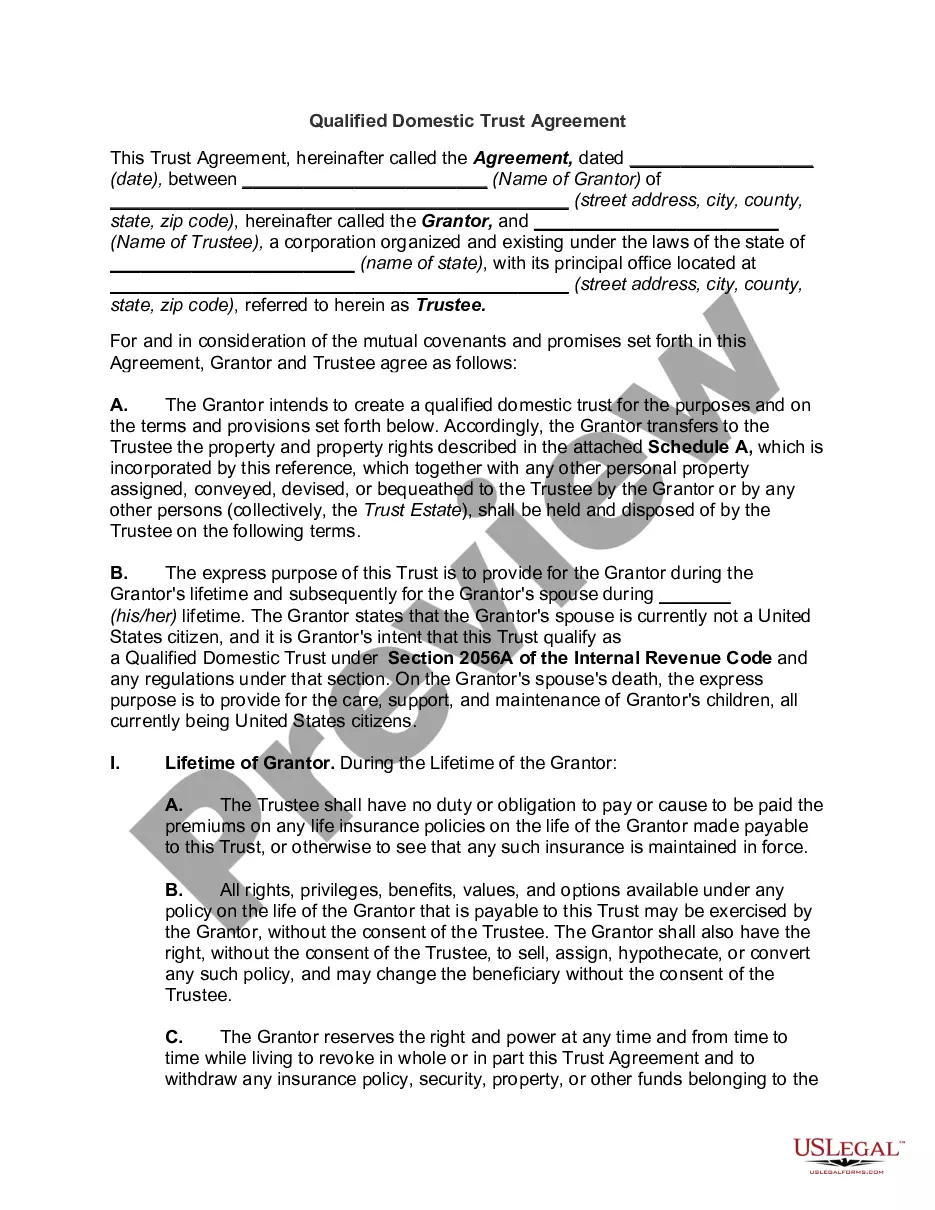

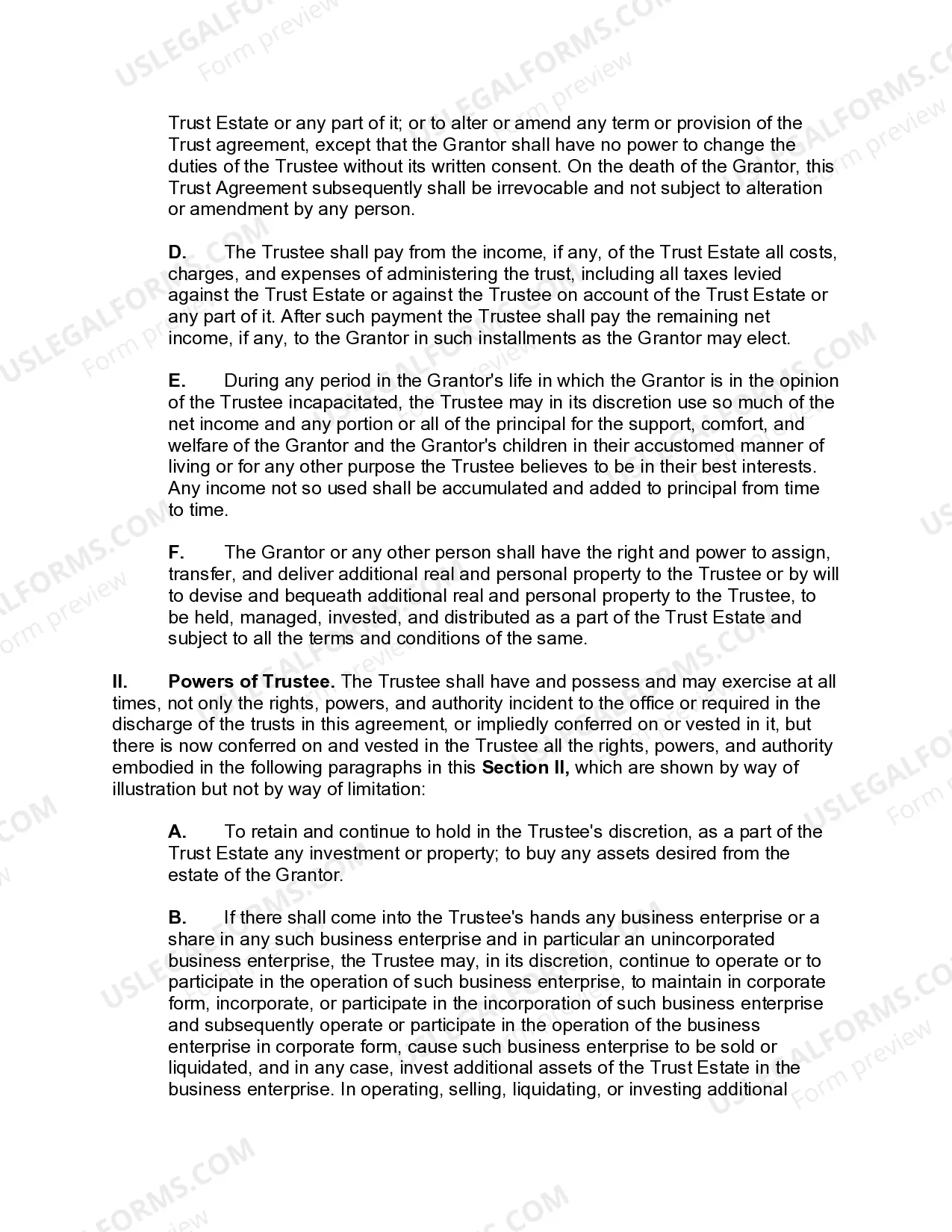

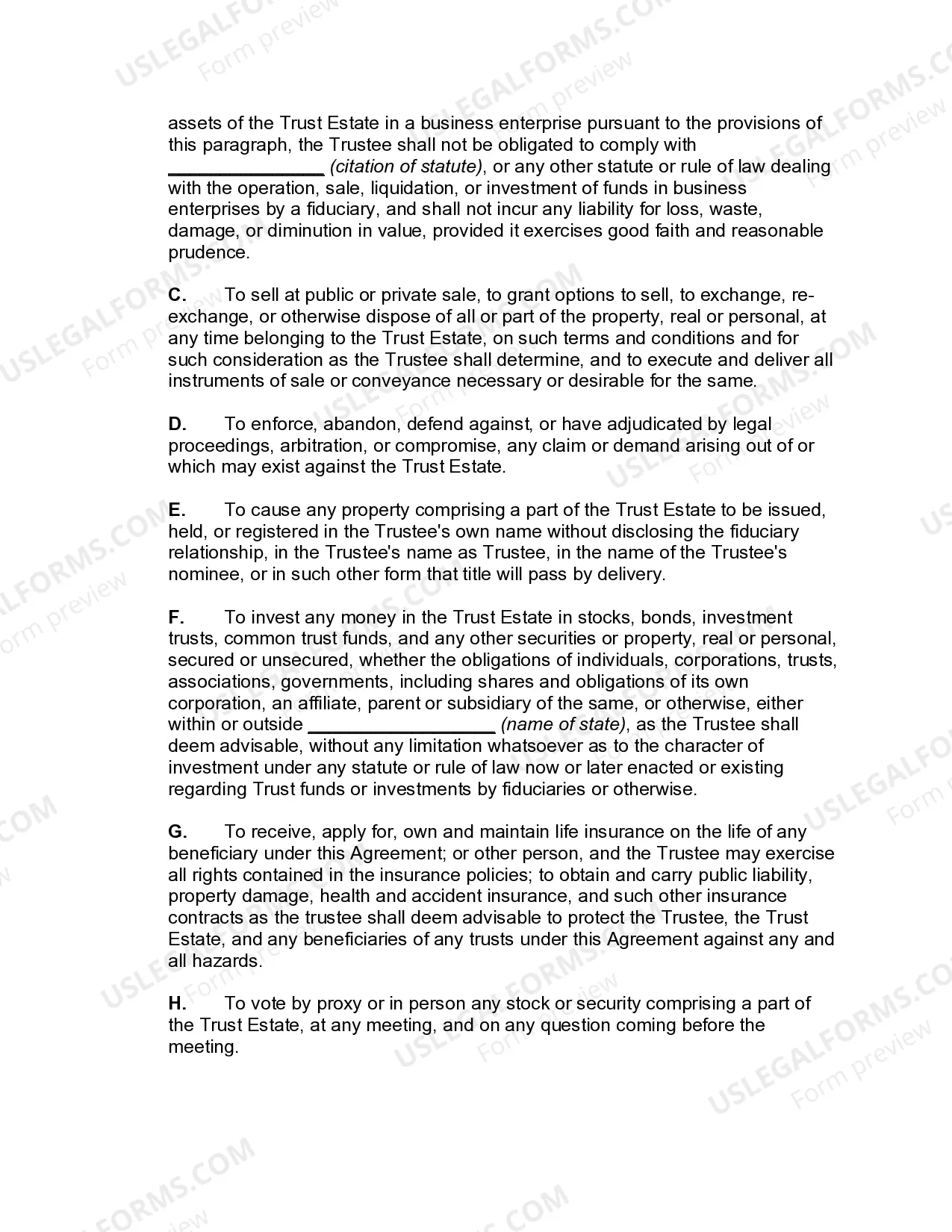

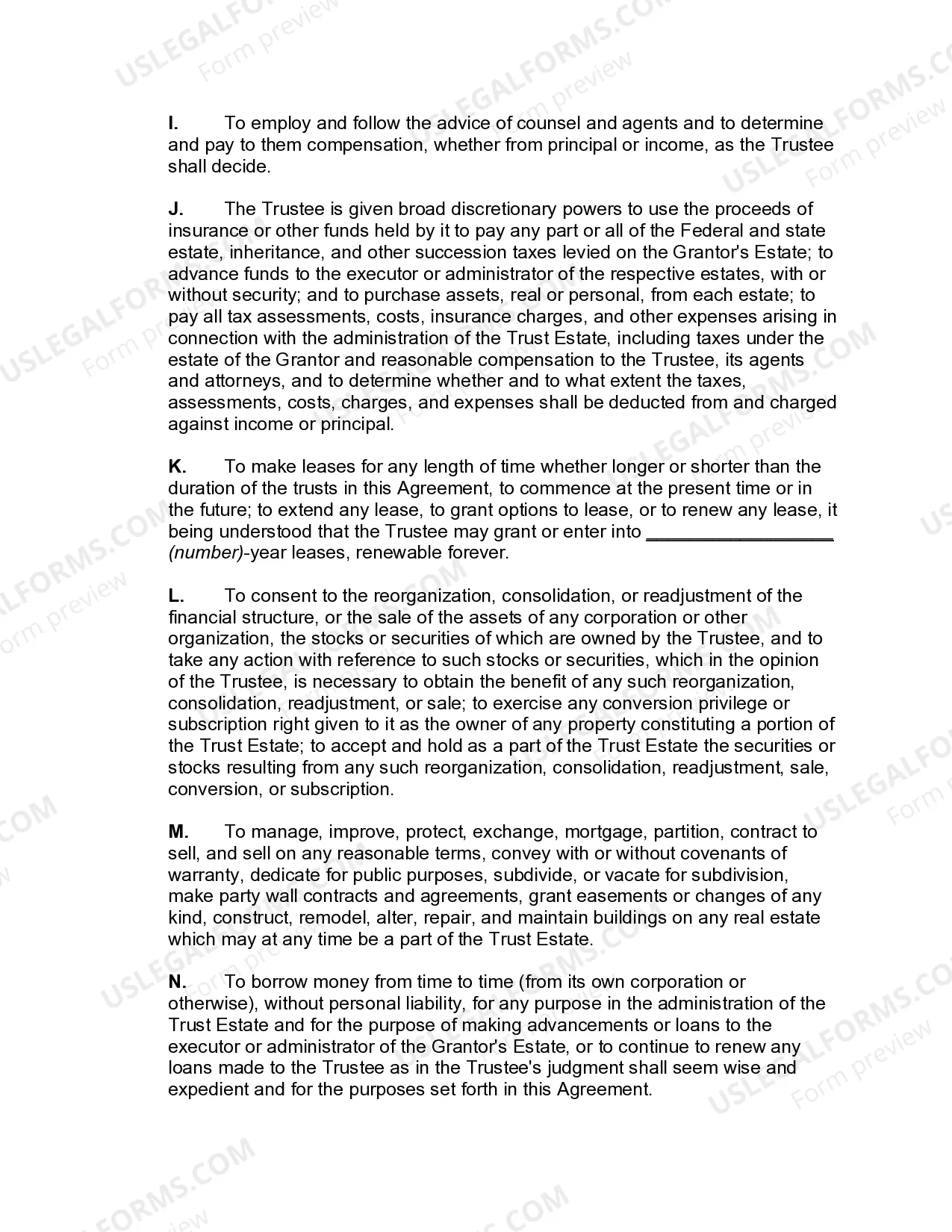

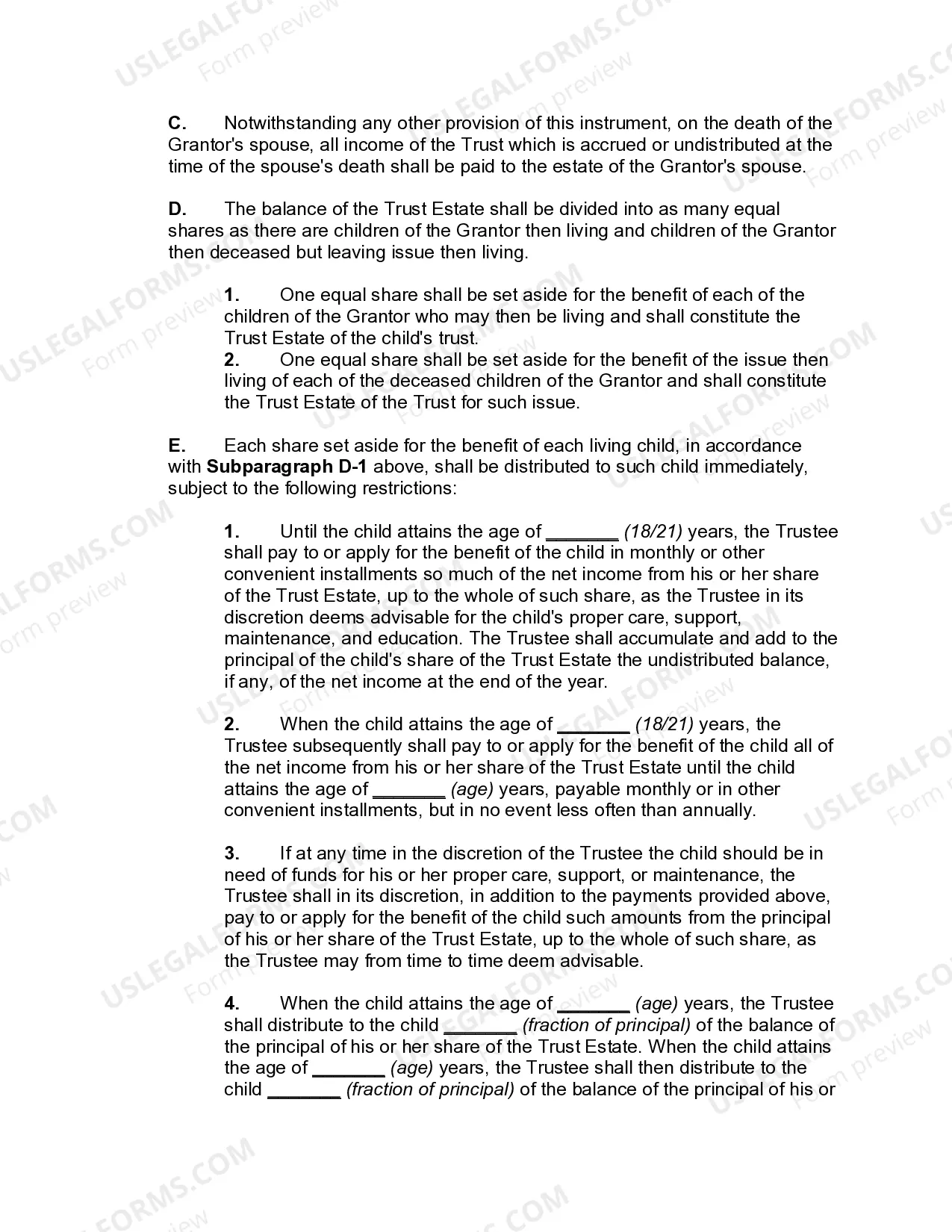

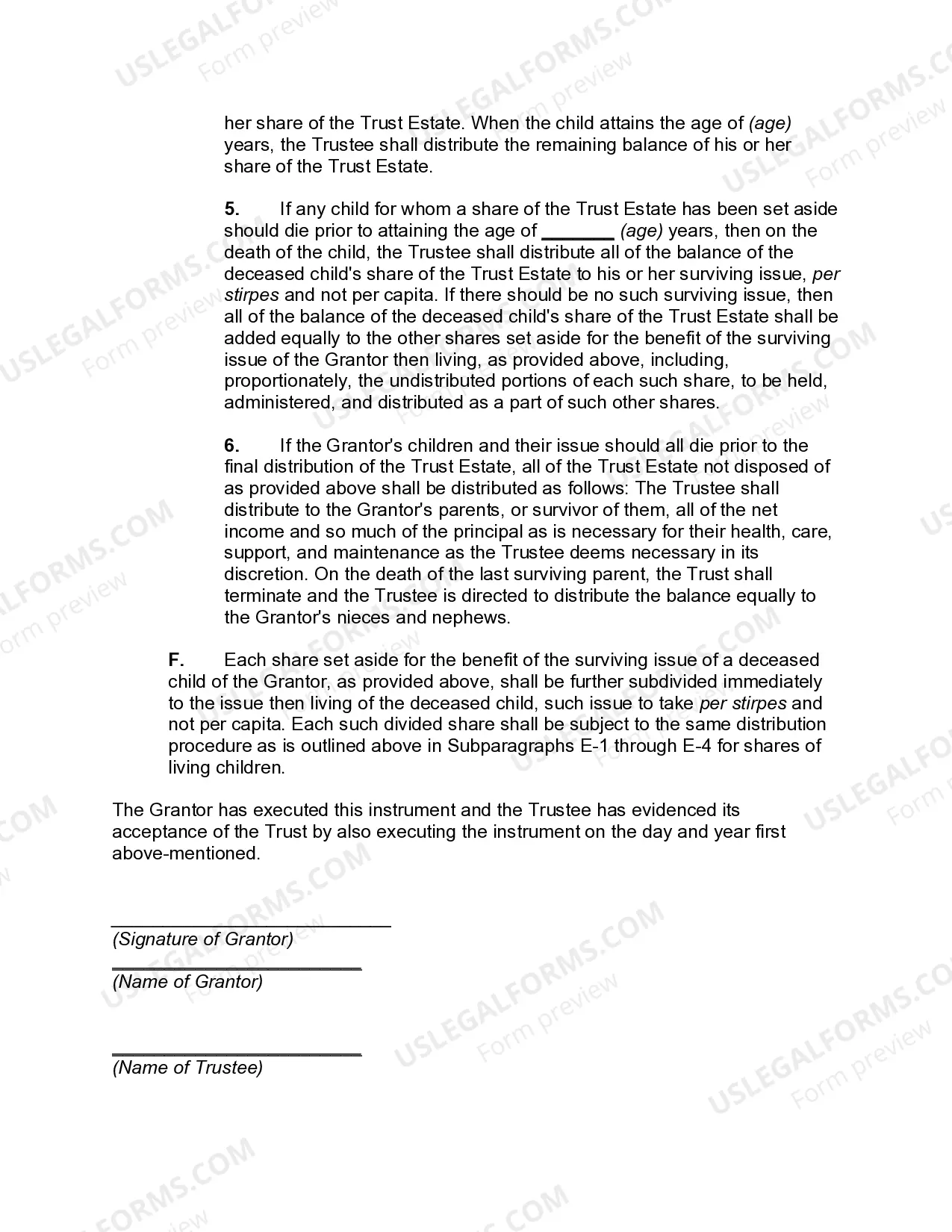

A Clark Nevada Qualified Domestic Trust Agreement (DOT) is a legal document that allows a non-U.S. citizen surviving spouse to maintain eligibility for an estate tax marital deduction upon the death of their U.S. citizen spouse. It is specifically designed to handle estate planning for couples where one spouse is a non-U.S. citizen. Under U.S. tax laws, when a U.S. citizen dies, their estate is subject to federal estate taxes. However, the unlimited marital deduction provision allows for the transfer of an unlimited amount of assets to a surviving spouse without incurring any estate taxes. This provision applies when the surviving spouse is a U.S. citizen. In situations where the surviving spouse is a non-U.S. citizen, the estate tax marital deduction is not automatically applicable. This is where a Clark Nevada DOT Agreement comes into play. It enables the non-U.S. citizen spouse to receive assets from the estate of the deceased U.S. citizen spouse while deferring the estate tax until the non-U.S. citizen spouse's death or until certain distributions are made from the trust. The Clark Nevada DOT Agreement requires the creation of an irrevocable trust, which must meet certain requirements to qualify as a DOT. Some of these requirements include appointing a U.S. trustee or executor, filing annual tax returns for the trust, and limiting distributions to the surviving spouse to only income or limited principal amounts. These restrictions ensure that the estate tax is paid upon distributions from the trust, without being completely exempted, as in the case of a U.S. citizen surviving spouse. The Clark Nevada DOT Agreement is specifically unique to the state of Nevada and is part of the larger category of DOT Agreements. There are variations of Dots in different states, each with its own set of specific requirements and regulations. However, the Clark Nevada DOT Agreement is particularly beneficial for individuals who reside in Nevada. In summary, the Clark Nevada Qualified Domestic Trust Agreement is an essential estate planning tool for couples where one spouse is a non-U.S. citizen. It allows the non-U.S. citizen surviving spouse to maintain eligibility for the estate tax marital deduction, thereby reducing potential estate tax liabilities. By meeting specific requirements, this agreement ensures compliance with U.S. tax laws and provides a structured means of transferring assets while deferring estate taxes.

Clark Nevada Qualified Domestic Trust Agreement

Description

How to fill out Clark Nevada Qualified Domestic Trust Agreement?

Preparing legal paperwork can be cumbersome. In addition, if you decide to ask a legal professional to draft a commercial agreement, documents for ownership transfer, pre-marital agreement, divorce papers, or the Clark Qualified Domestic Trust Agreement, it may cost you a lot of money. So what is the most reasonable way to save time and money and draw up legitimate forms in total compliance with your state and local regulations? US Legal Forms is an excellent solution, whether you're searching for templates for your individual or business needs.

US Legal Forms is biggest online library of state-specific legal documents, providing users with the up-to-date and professionally checked templates for any use case collected all in one place. Therefore, if you need the current version of the Clark Qualified Domestic Trust Agreement, you can easily locate it on our platform. Obtaining the papers requires a minimum of time. Those who already have an account should check their subscription to be valid, log in, and pick the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Clark Qualified Domestic Trust Agreement:

- Glance through the page and verify there is a sample for your area.

- Examine the form description and use the Preview option, if available, to make sure it's the sample you need.

- Don't worry if the form doesn't satisfy your requirements - search for the right one in the header.

- Click Buy Now when you find the needed sample and pick the best suitable subscription.

- Log in or sign up for an account to pay for your subscription.

- Make a payment with a credit card or through PayPal.

- Choose the file format for your Clark Qualified Domestic Trust Agreement and download it.

Once finished, you can print it out and complete it on paper or upload the template to an online editor for a faster and more convenient fill-out. US Legal Forms allows you to use all the documents ever acquired multiple times - you can find your templates in the My Forms tab in your profile. Give it a try now!