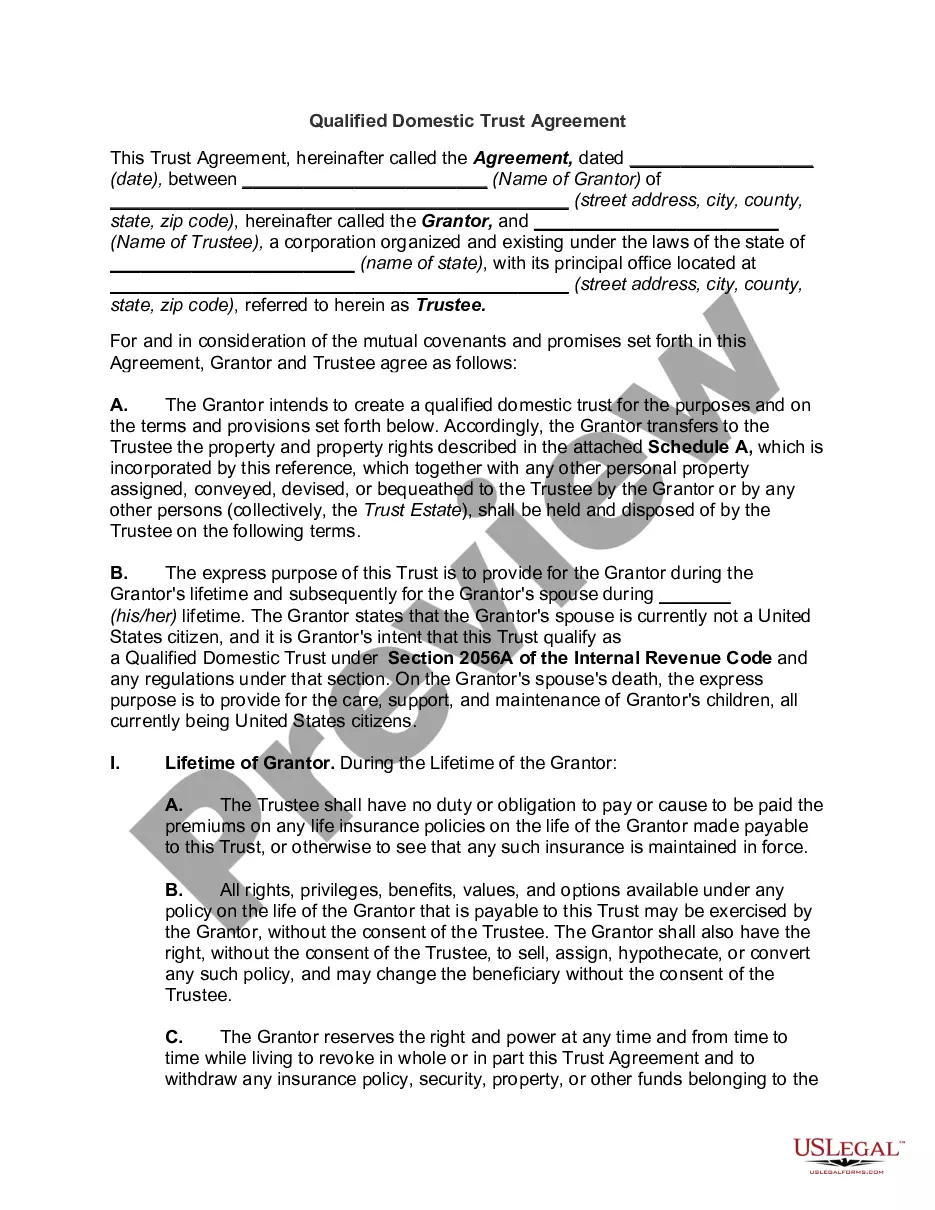

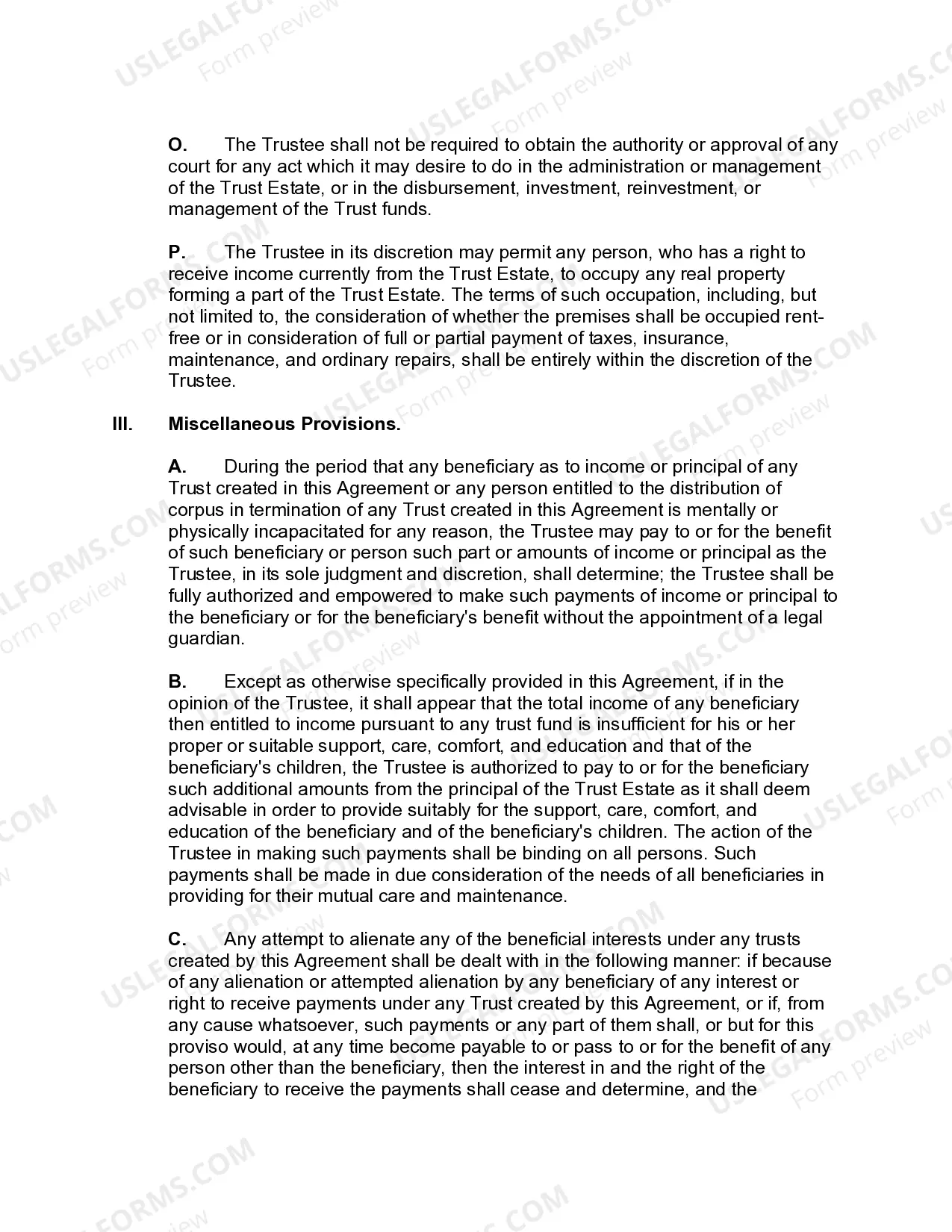

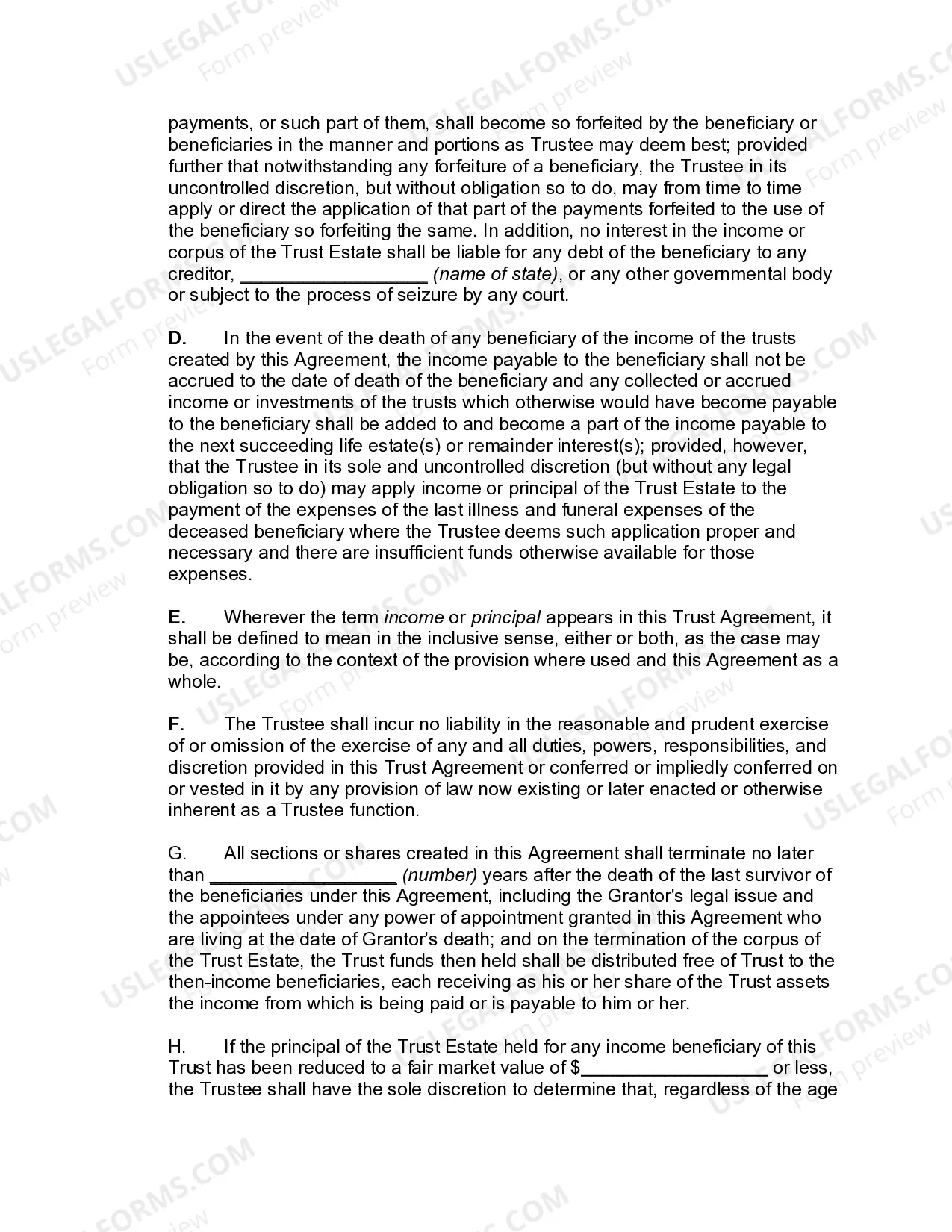

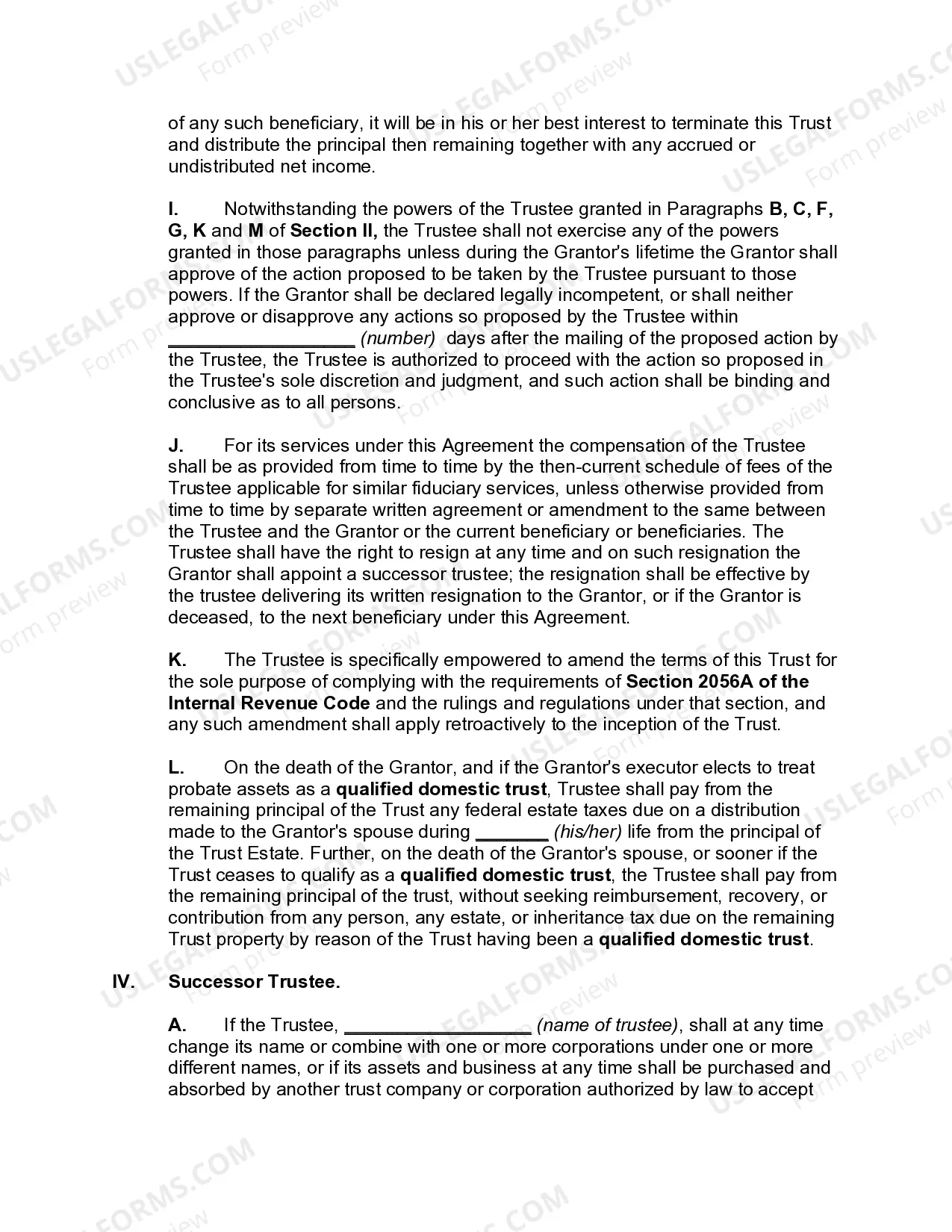

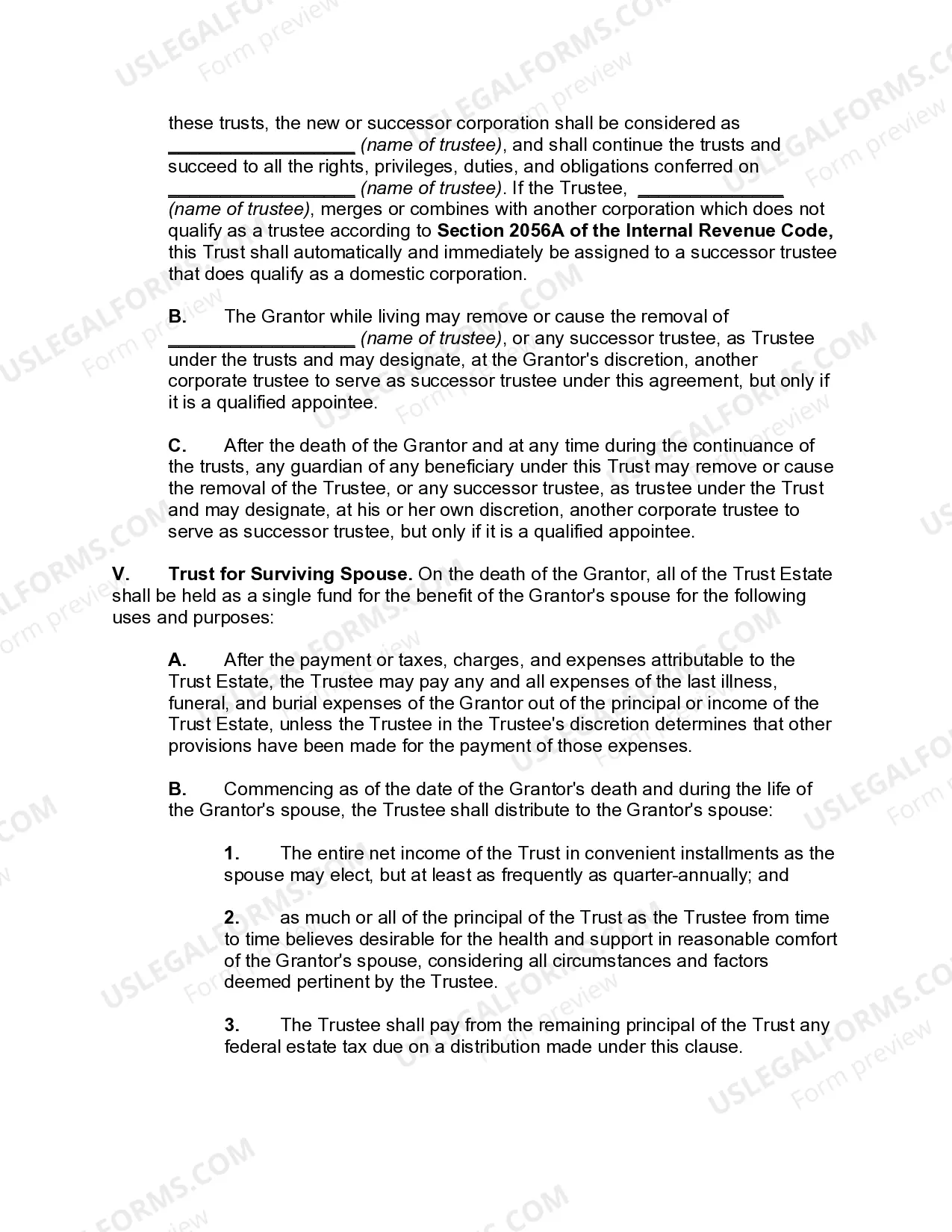

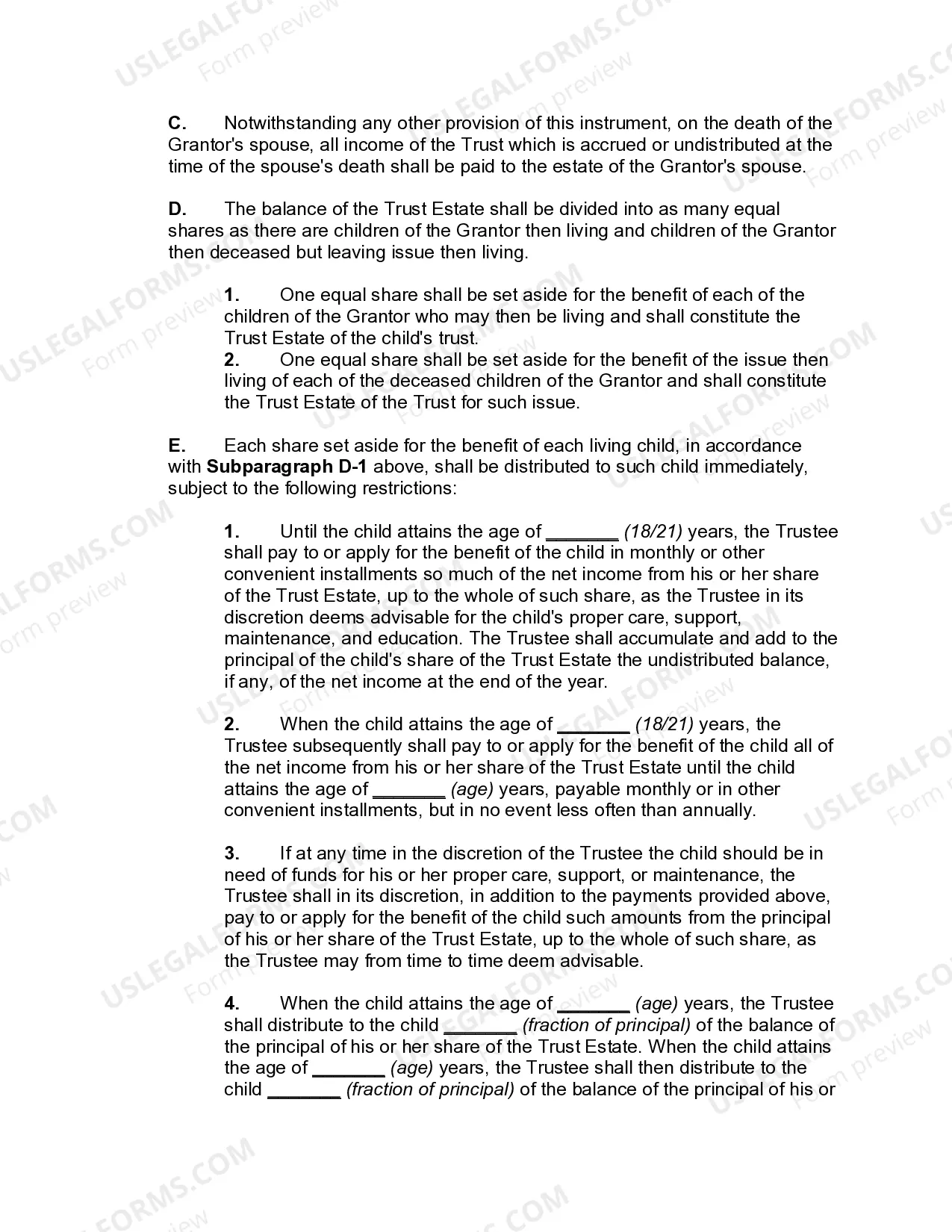

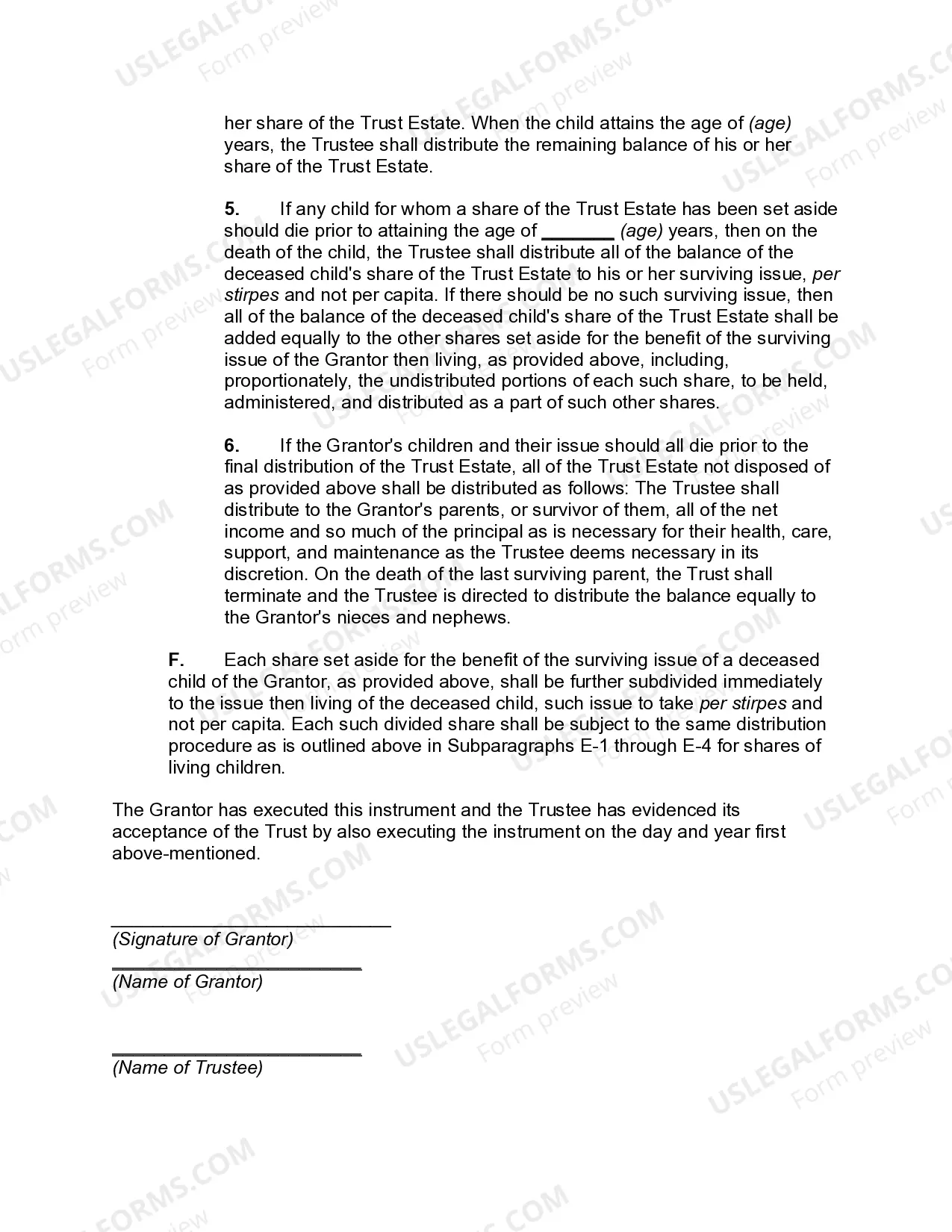

Contra Costa California Qualified Domestic Trust Agreement (CCC DTA) is a legal instrument that provides a means for non-U.S. citizen spouses to defer estate taxes on assets passed down to them by their U.S. citizen spouse. This trust agreement is specifically designed to meet the requirements of the Internal Revenue Service (IRS) for qualifying as a Qualified Domestic Trust (DOT). Under the CCC DTA, a non-U.S. citizen spouse can become the beneficiary of a trust established by their U.S. citizen spouse, allowing them to receive income from the trust assets while deferring the payment of estate taxes until the trust principal is distributed. This provides favorable tax treatment for non-U.S. citizen spouses, who would otherwise be subject to immediate estate tax liability upon receiving the assets. To qualify as a DOT under the CCC DTA, certain criteria outlined by the IRS must be met. The trust must have at least one U.S. trustee who is responsible for ensuring appropriate administration and compliance with tax regulations. Additionally, the DOT must meet the requirement of being subject to U.S. estate tax jurisdiction to ensure tax payment enforcement. There are different types of CCC DTA agreements that can be tailored to specific needs and circumstances. Examples include: 1. Revocable CCC DTA: This type of agreement allows the granter (U.S. citizen spouse) to modify or revoke the trust during their lifetime, providing flexibility while ensuring tax benefits for the non-U.S. citizen spouse. 2. Irrevocable CCC DTA: Unlike the revocable agreement, the irrevocable CCC DTA cannot be altered or revoked once established. This provides security and certainty for the non-U.S. citizen spouse, ensuring that the trust assets will be managed and distributed according to the granter's wishes. 3. Testamentary CCC DTA: This agreement is created within the granter's last will and testament and only takes effect upon their death. It allows for tax planning and deferral strategies while providing the ability to modify or revoke the trust during the granter's lifetime. Creating a CCC DTA agreement requires careful consideration of the assets, tax implications, and specific goals of the granter and non-U.S. citizen spouse. It is crucial to consult with an experienced estate planning attorney who specializes in international estate tax matters to ensure proper compliance with IRS regulations and maximize the tax benefits available.

Contra Costa California Qualified Domestic Trust Agreement

Description

How to fill out Contra Costa California Qualified Domestic Trust Agreement?

Preparing legal documentation can be cumbersome. In addition, if you decide to ask an attorney to write a commercial agreement, papers for proprietorship transfer, pre-marital agreement, divorce papers, or the Contra Costa Qualified Domestic Trust Agreement, it may cost you a fortune. So what is the best way to save time and money and draft legitimate documents in total compliance with your state and local laws? US Legal Forms is an excellent solution, whether you're looking for templates for your individual or business needs.

US Legal Forms is largest online library of state-specific legal documents, providing users with the up-to-date and professionally verified templates for any scenario accumulated all in one place. Therefore, if you need the current version of the Contra Costa Qualified Domestic Trust Agreement, you can easily locate it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and pick the sample by clicking on the Download button. If you haven't subscribed yet, here's how you can get the Contra Costa Qualified Domestic Trust Agreement:

- Glance through the page and verify there is a sample for your region.

- Examine the form description and use the Preview option, if available, to ensure it's the template you need.

- Don't worry if the form doesn't satisfy your requirements - search for the correct one in the header.

- Click Buy Now once you find the required sample and choose the best suitable subscription.

- Log in or sign up for an account to pay for your subscription.

- Make a payment with a credit card or via PayPal.

- Opt for the file format for your Contra Costa Qualified Domestic Trust Agreement and download it.

When finished, you can print it out and complete it on paper or upload the template to an online editor for a faster and more practical fill-out. US Legal Forms allows you to use all the documents ever acquired many times - you can find your templates in the My Forms tab in your profile. Try it out now!