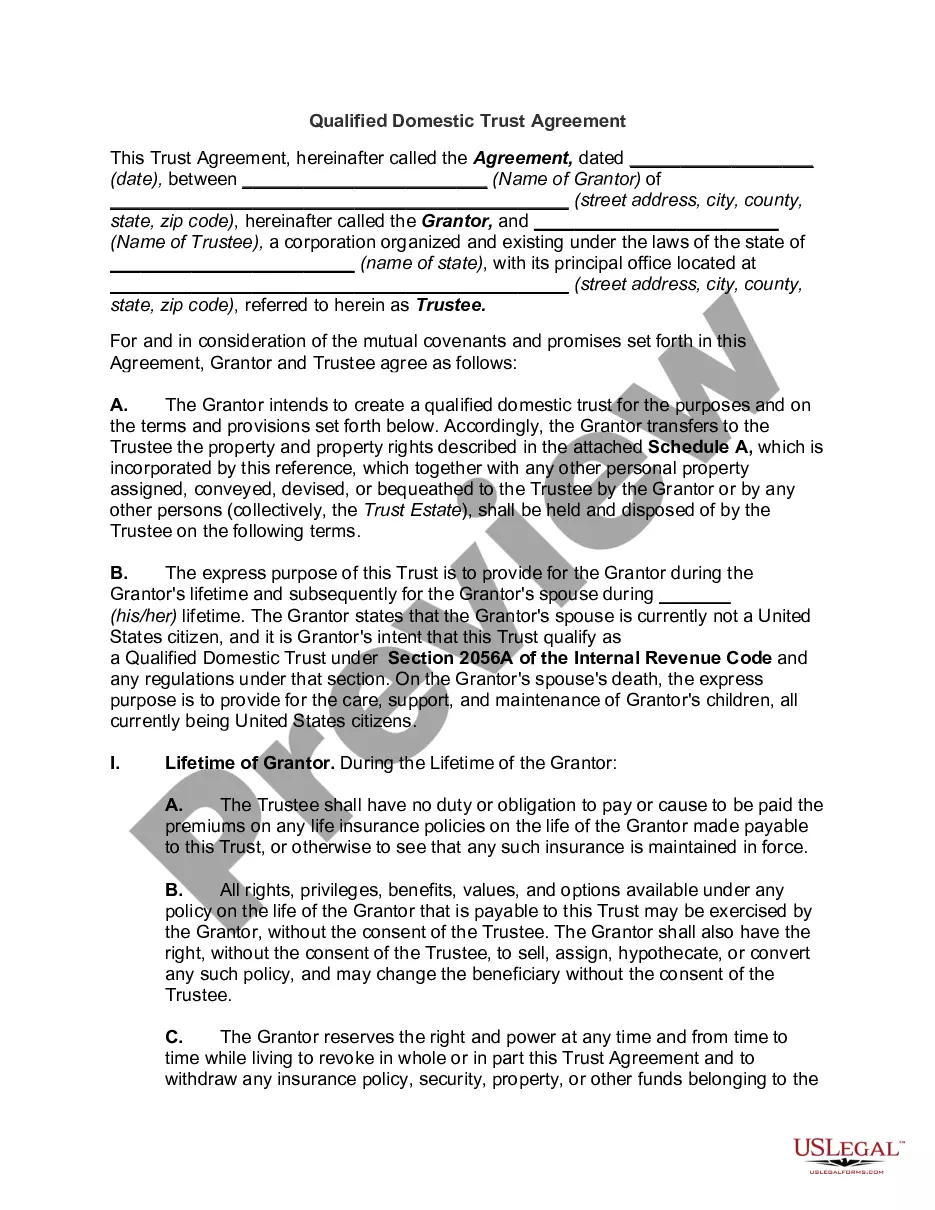

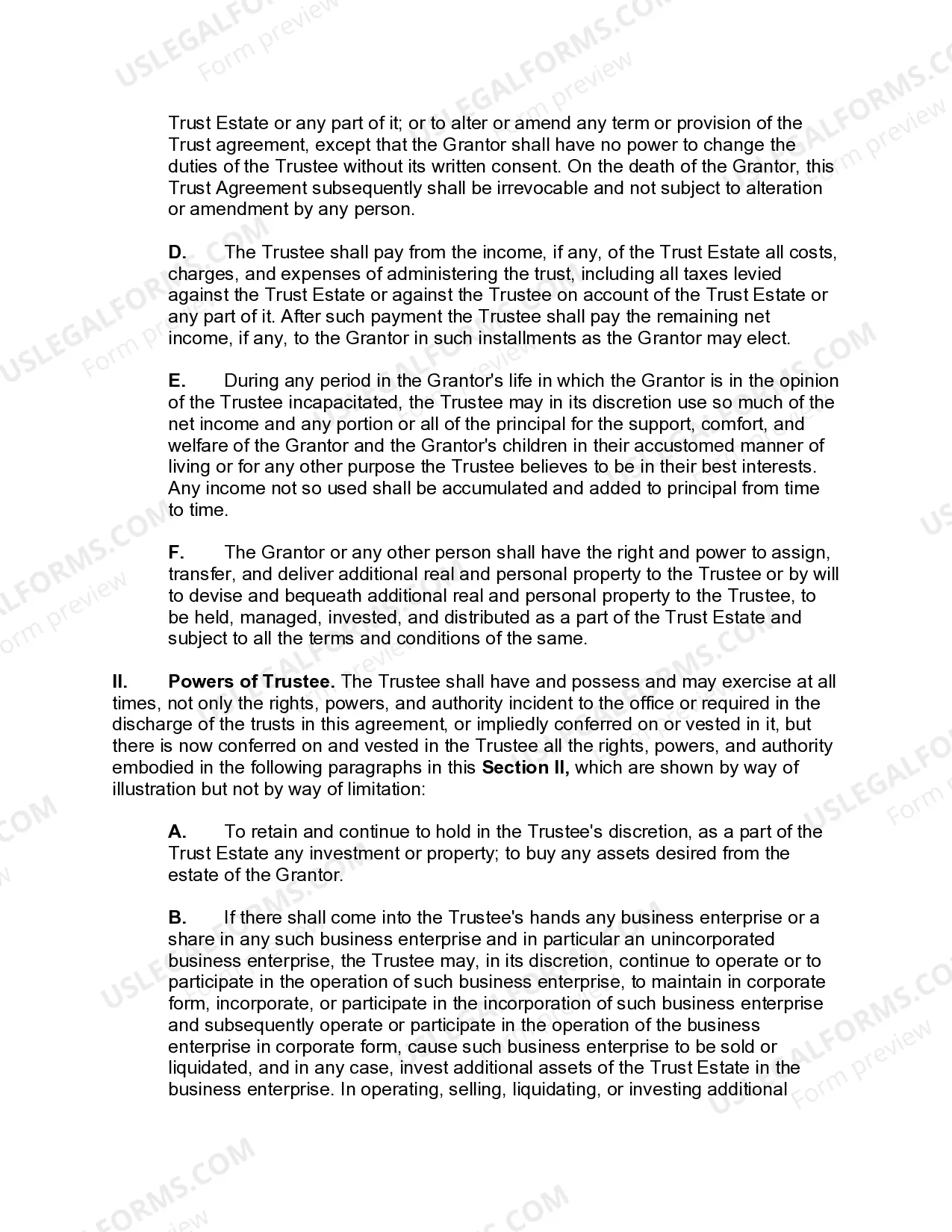

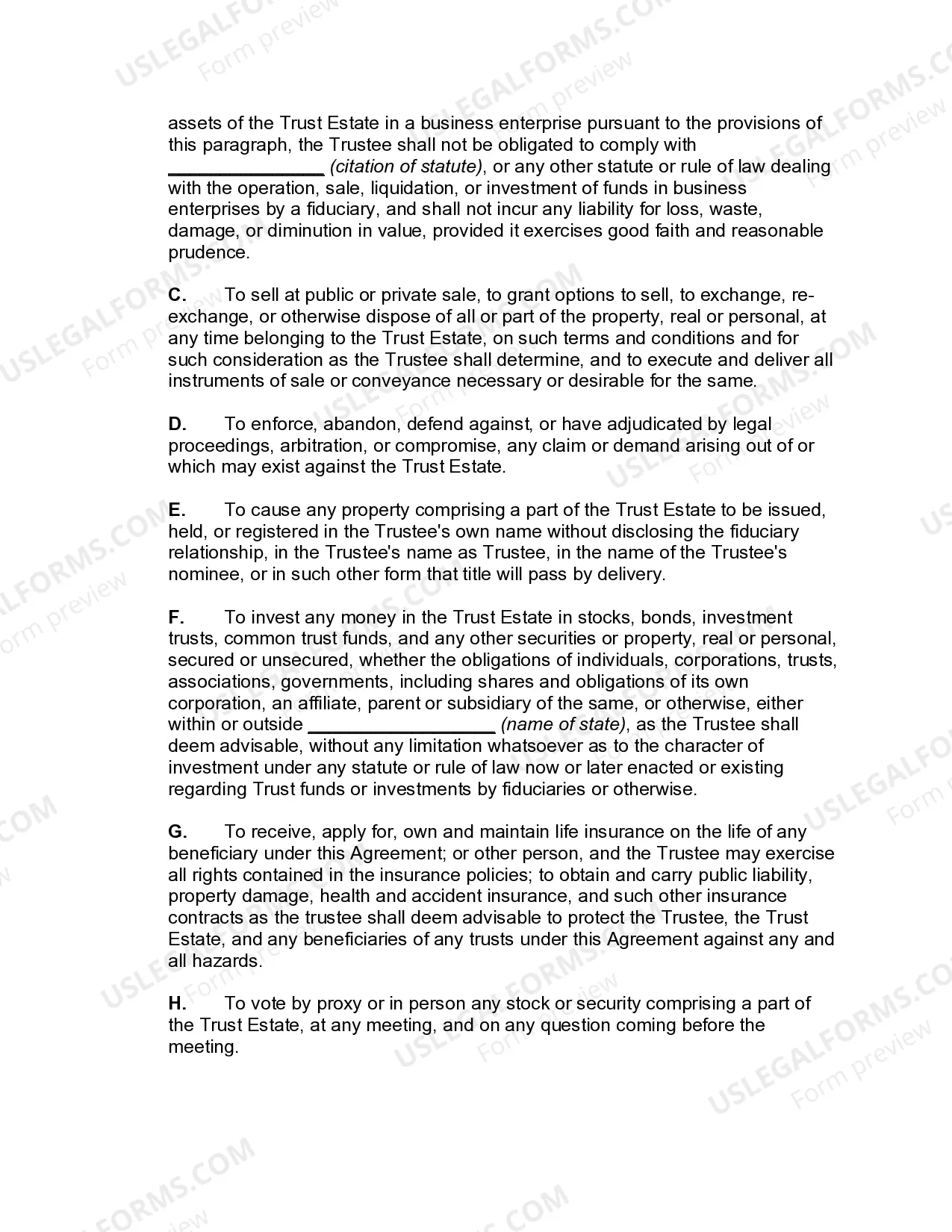

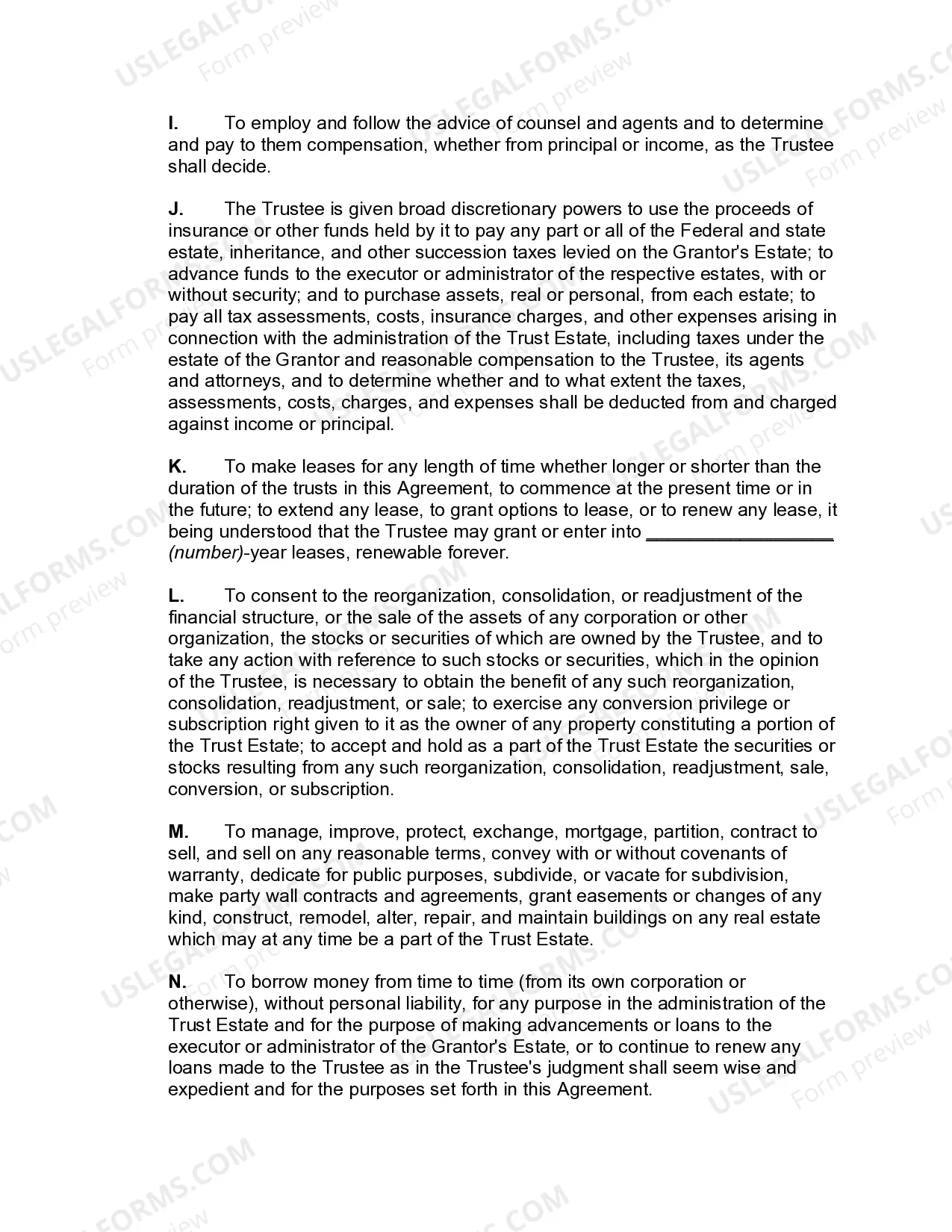

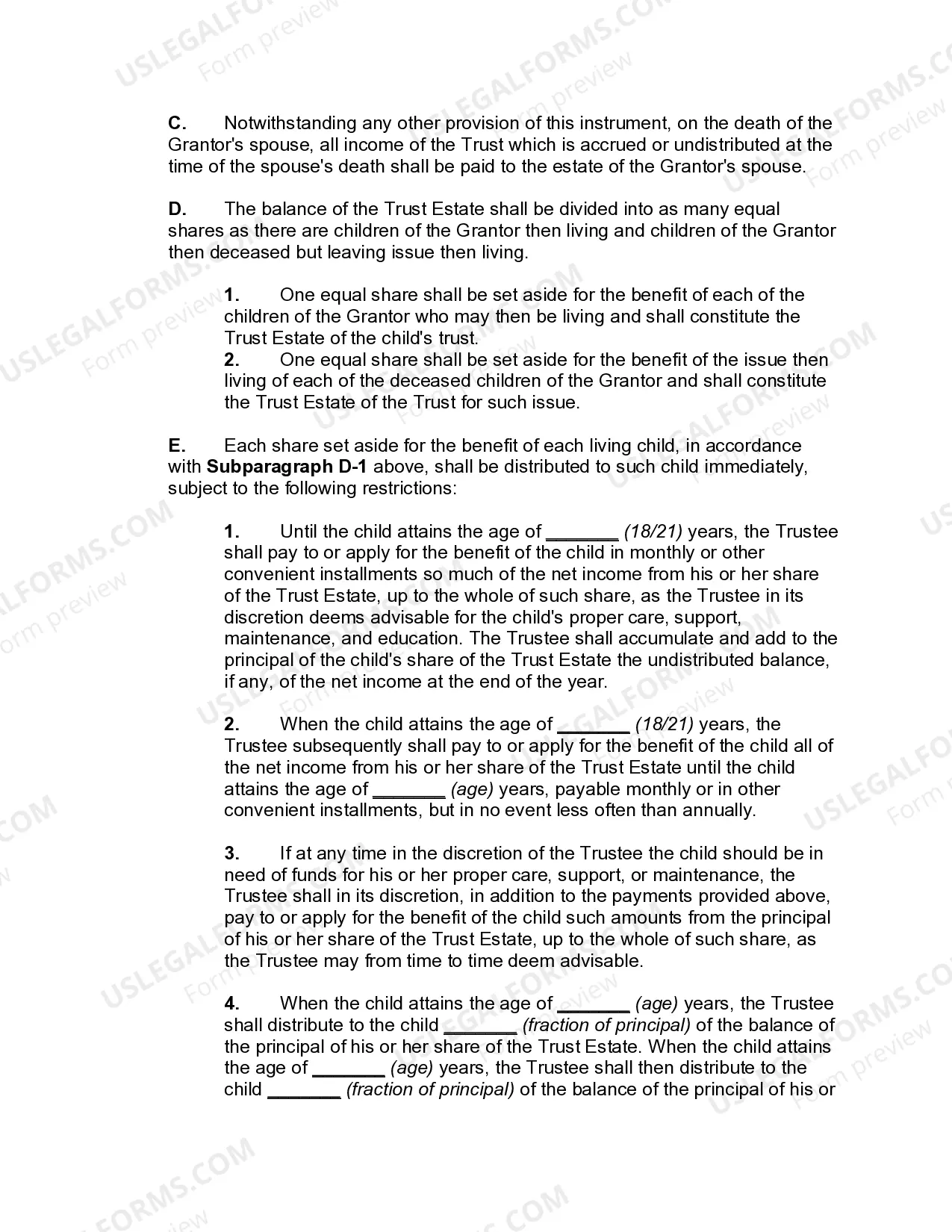

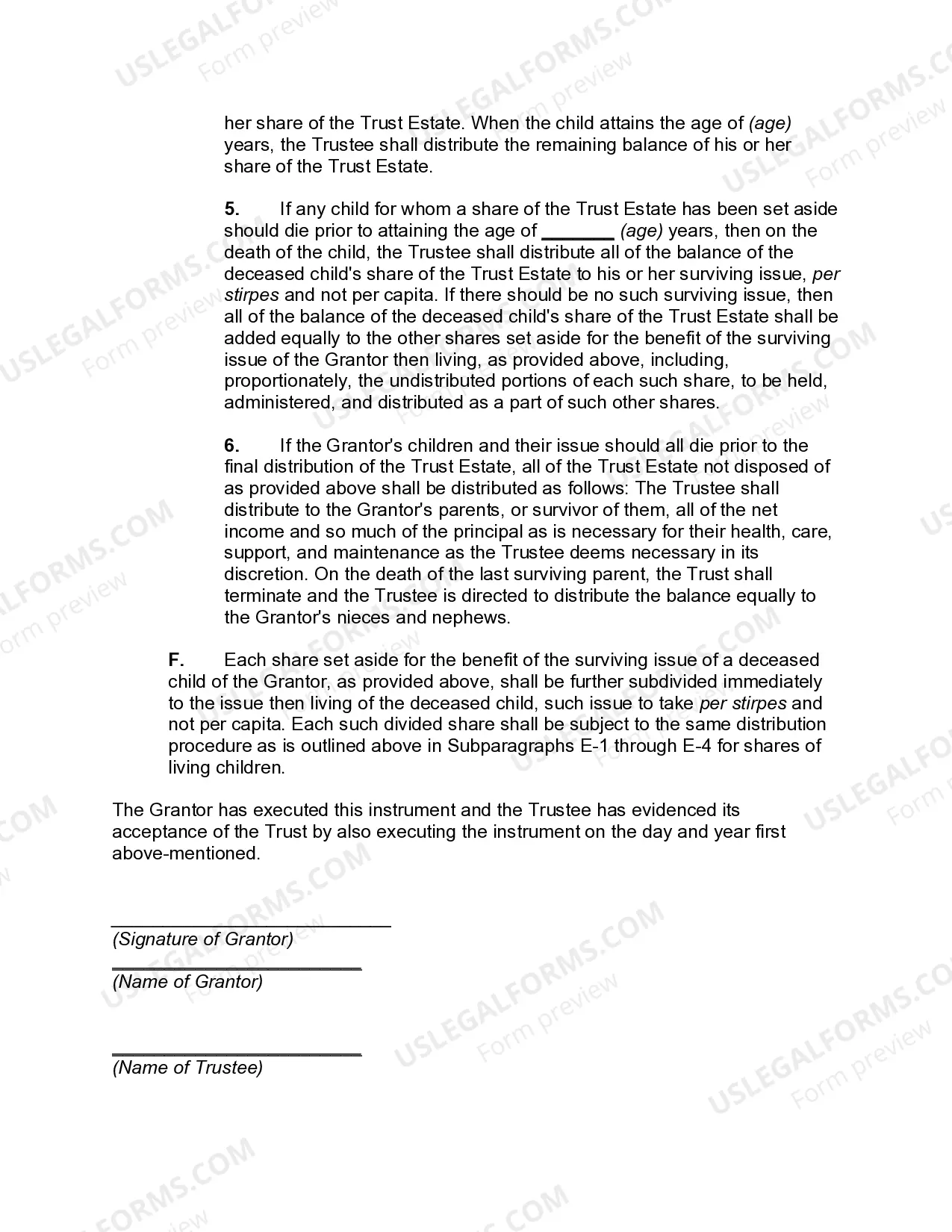

A Kings New York Qualified Domestic Trust Agreement is a legal arrangement that allows a non-U.S. citizen surviving spouse to qualify for the marital deduction under U.S. estate tax laws. This type of trust is specifically designed for individuals who are not U.S. citizens but have assets in the United States. The Kings New York Qualified Domestic Trust Agreement ensures that the non-U.S. citizen spouse receives income generated from the trust's assets during their lifetime while delaying the estate tax until their death. This arrangement provides significant estate planning advantages for couples with mixed citizenship. There are two types of Kings New York Qualified Domestic Trust Agreements: 1. Inter Vivos Qualified Domestic Trust (DOT): This type of trust agreement is established during the granter's lifetime and is commonly used to transfer assets to the non-U.S. citizen spouse while still meeting the requirements for the marital deduction. The granter can fund the trust with various assets such as cash, securities, or real estate. 2. Testamentary Qualified Domestic Trust (DOT): This trust agreement is created through the granter's will and takes effect upon their death. The granter can designate a portion of their estate to be transferred to the DOT, ensuring that the non-U.S. citizen spouse fulfills the requirements for the marital deduction and continues to receive income from the trust during their lifetime. Both types of Kings New York Qualified Domestic Trust Agreements have specific provisions and requirements to ensure compliance with U.S. tax laws. These agreements typically involve an appointed trustee who manages the trust's assets, makes distributions to the non-U.S. citizen spouse, files tax returns, and adheres to reporting obligations. In summary, the Kings New York Qualified Domestic Trust Agreement is a valuable estate planning tool for non-U.S. citizen spouses with assets in the United States. It enables them to qualify for the marital deduction under U.S. estate tax laws, ensuring the smooth transfer of assets while minimizing the impact of estate taxes.

Kings New York Qualified Domestic Trust Agreement

Description

How to fill out Kings New York Qualified Domestic Trust Agreement?

Laws and regulations in every area vary from state to state. If you're not an attorney, it's easy to get lost in a variety of norms when it comes to drafting legal paperwork. To avoid expensive legal assistance when preparing the Kings Qualified Domestic Trust Agreement, you need a verified template valid for your county. That's when using the US Legal Forms platform is so advantageous.

US Legal Forms is a trusted by millions online catalog of more than 85,000 state-specific legal templates. It's a perfect solution for specialists and individuals looking for do-it-yourself templates for various life and business occasions. All the documents can be used many times: once you purchase a sample, it remains available in your profile for future use. Therefore, if you have an account with a valid subscription, you can simply log in and re-download the Kings Qualified Domestic Trust Agreement from the My Forms tab.

For new users, it's necessary to make a few more steps to obtain the Kings Qualified Domestic Trust Agreement:

- Take a look at the page content to make sure you found the correct sample.

- Take advantage of the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your requirements.

- Click on the Buy Now button to get the template once you find the right one.

- Choose one of the subscription plans and log in or sign up for an account.

- Choose how you prefer to pay for your subscription (with a credit card or PayPal).

- Select the format you want to save the document in and click Download.

- Complete and sign the template in writing after printing it or do it all electronically.

That's the simplest and most cost-effective way to get up-to-date templates for any legal reasons. Find them all in clicks and keep your documentation in order with the US Legal Forms!