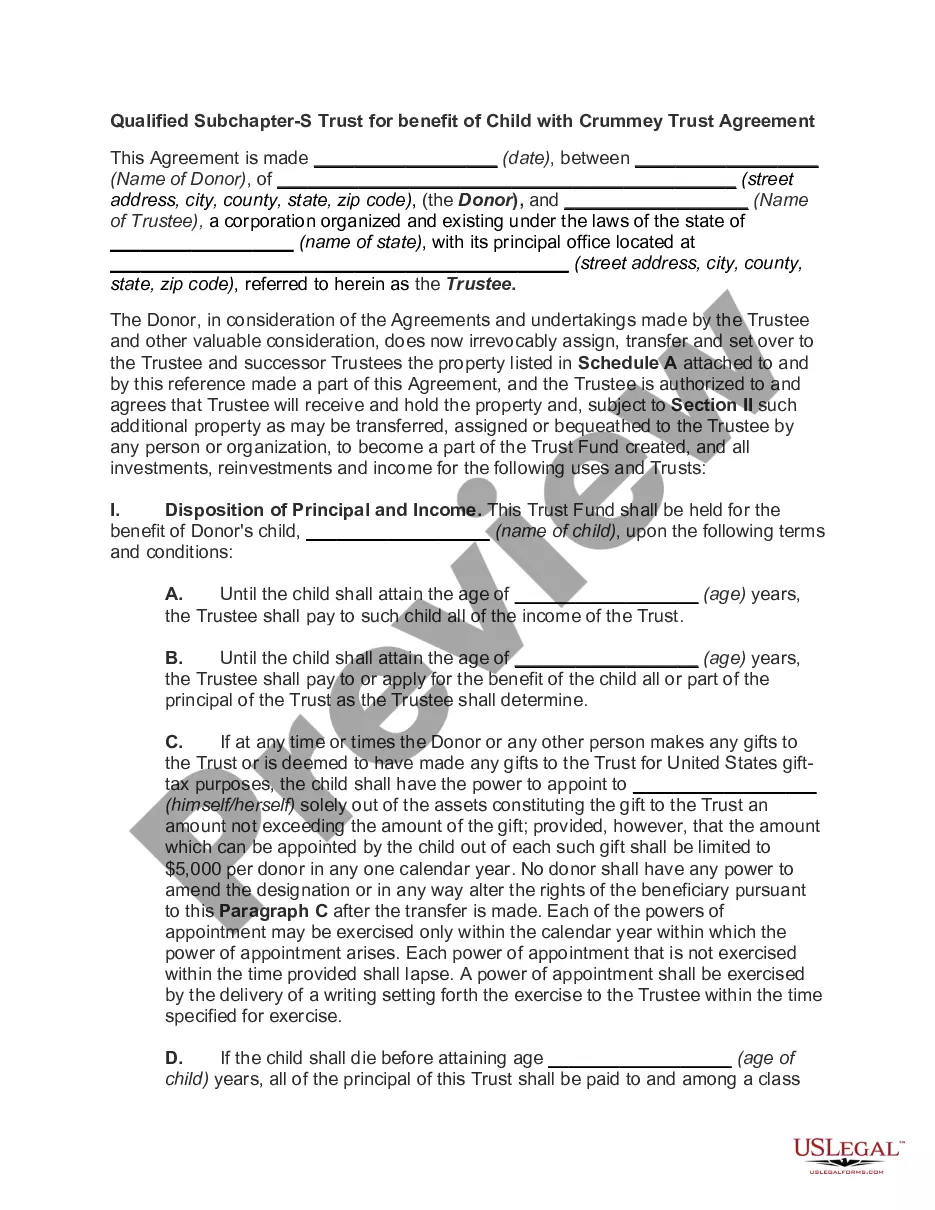

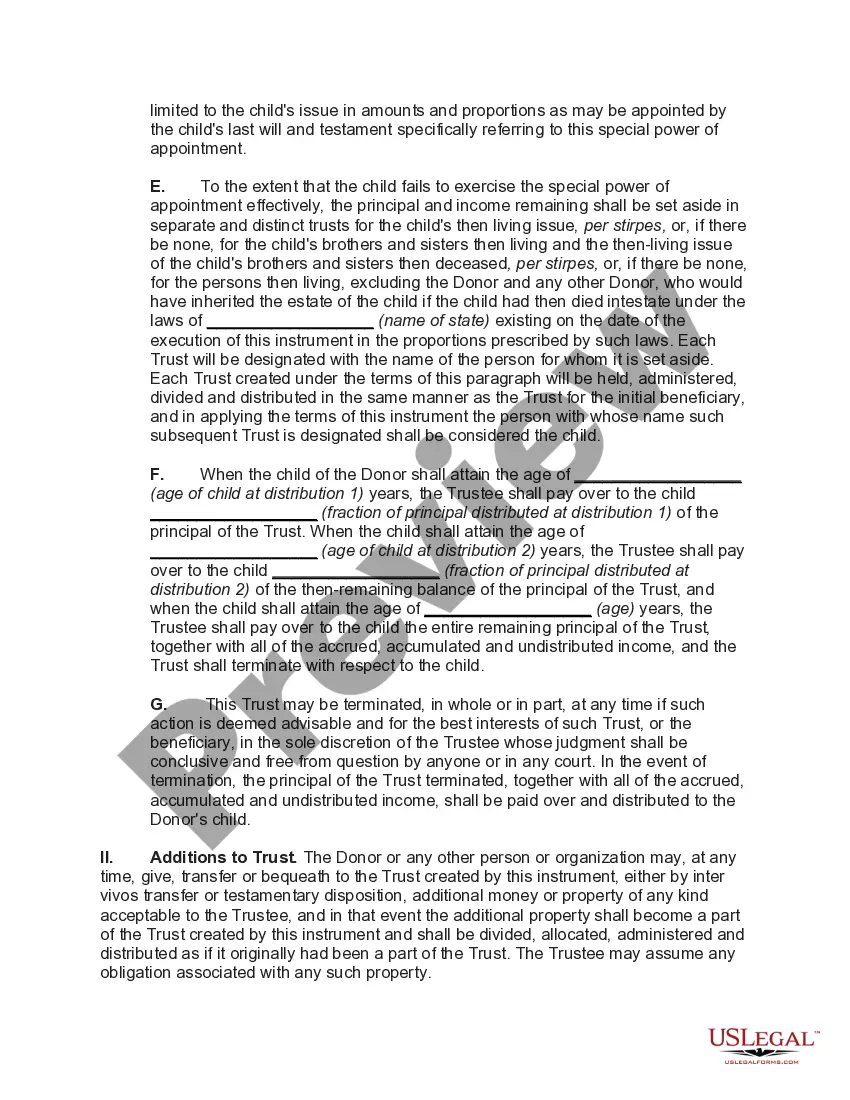

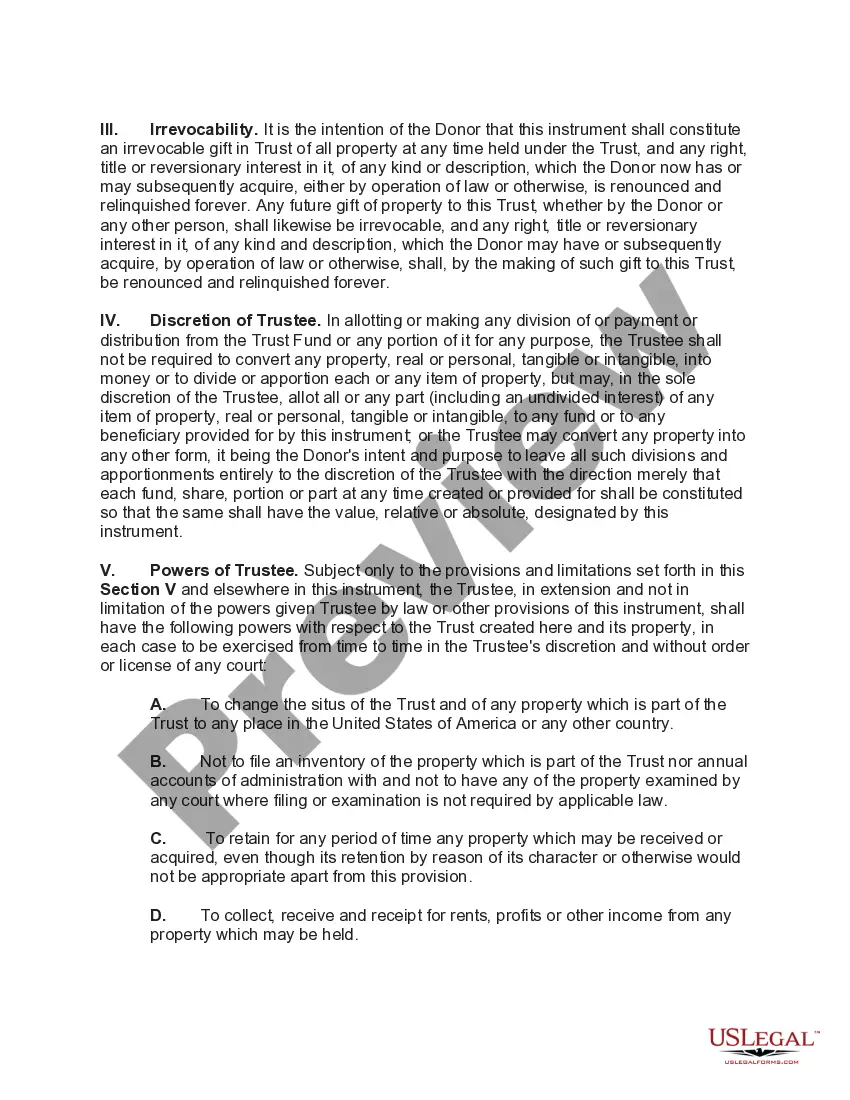

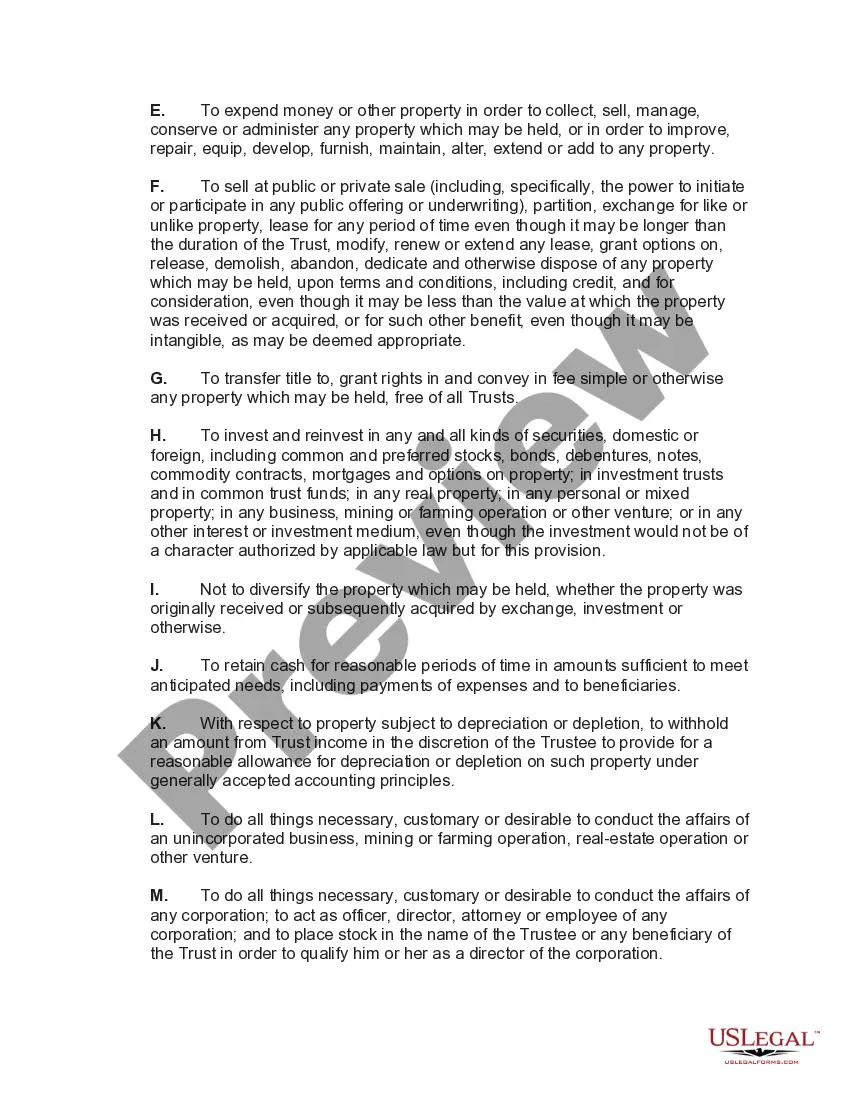

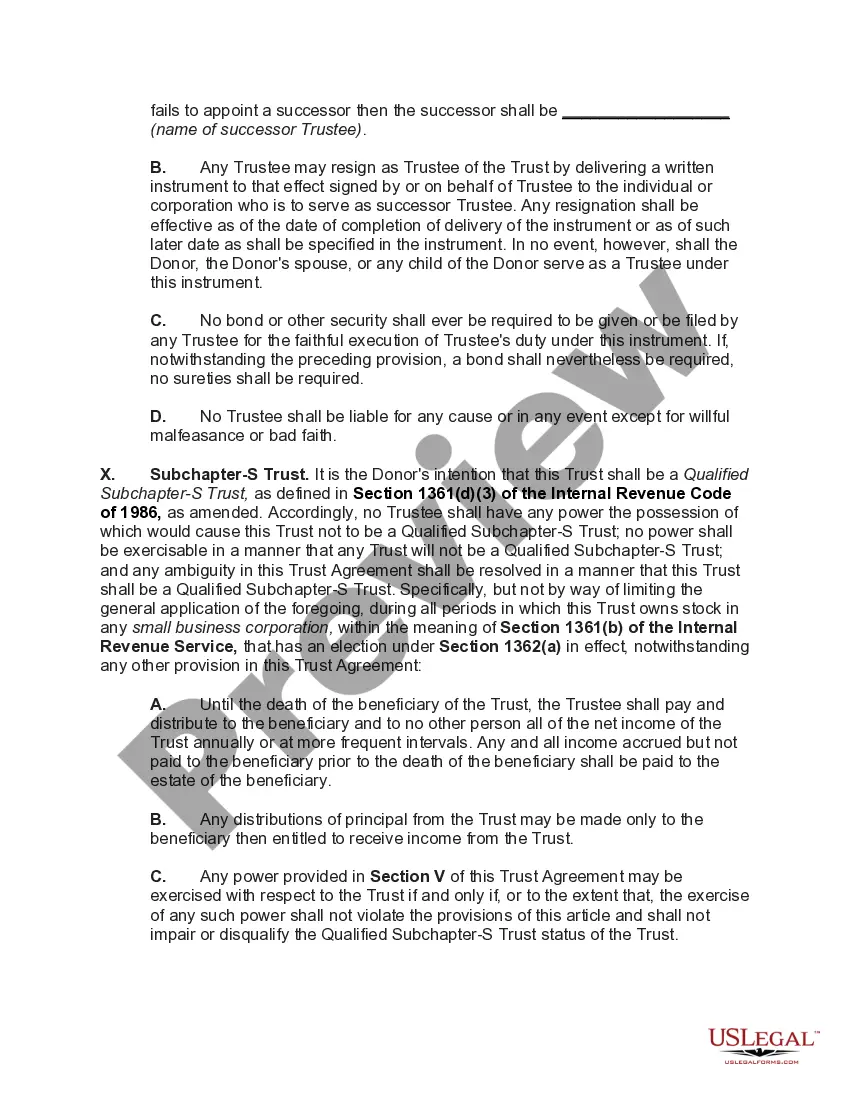

A Montgomery Maryland Qualified Subchapter-S Trust for the Benefit of a Child with a Crummy Trust Agreement is a specific type of trust arrangement designed to provide financial support and protection for a child while taking advantage of certain tax benefits offered under Subchapter-S of the Internal Revenue Code. This trust is commonly used by parents or grandparents who wish to transfer assets to a child while minimizing estate or gift taxes. The Crummy Trust Agreement, named after Clifford Crummy, a taxpayer involved in a significant tax court case, refers to a provision within the trust that allows for annual withdrawals of gifts made to the trust without incurring gift taxes. By utilizing the Crummy provision, individuals can contribute funds to the trust each year, up to certain limits, without triggering any gift tax liability. The Montgomery Maryland Qualified Subchapter-S Trust for the Benefit of a Child with a Crummy Trust Agreement offers several advantages. Firstly, it ensures that assets designated for the child's benefit are properly managed, protected, and distributed according to the trust terms, providing greater control over how the funds are used. Secondly, it offers potential tax benefits, including income tax pass-through treatment as granted to Subchapter-S corporations, which can minimize the tax burden on the trust's income. There might be variations of the Montgomery Maryland Qualified Subchapter-S Trust for the Benefit of a Child with a Crummy Trust Agreement based on individual preferences and specific circumstances. These variations could include different investment strategies, provisions for educational expenses, restrictions on trust distributions, or even additional siblings being named as beneficiaries within the trust. In summary, a Montgomery Maryland Qualified Subchapter-S Trust for the Benefit of a Child with a Crummy Trust Agreement is a specialized legal arrangement that combines the advantages of a trust structure with the tax benefits of Subchapter-S corporations. It allows individuals to transfer assets to a child while minimizing tax liabilities and ensuring that the designated funds are protected and distributed according to the trust's terms.

Montgomery Maryland Qualified Subchapter-S Trust for Benefit of Child with Crummey Trust Agreement

Description

How to fill out Montgomery Maryland Qualified Subchapter-S Trust For Benefit Of Child With Crummey Trust Agreement?

Dealing with legal forms is a necessity in today's world. Nevertheless, you don't always need to seek qualified assistance to create some of them from the ground up, including Montgomery Qualified Subchapter-S Trust for Benefit of Child with Crummey Trust Agreement, with a platform like US Legal Forms.

US Legal Forms has over 85,000 forms to select from in various categories varying from living wills to real estate paperwork to divorce documents. All forms are organized according to their valid state, making the searching experience less frustrating. You can also find information materials and guides on the website to make any activities related to paperwork execution straightforward.

Here's how you can find and download Montgomery Qualified Subchapter-S Trust for Benefit of Child with Crummey Trust Agreement.

- Take a look at the document's preview and outline (if available) to get a basic information on what you’ll get after getting the document.

- Ensure that the document of your choice is specific to your state/county/area since state laws can impact the legality of some documents.

- Examine the related document templates or start the search over to find the correct document.

- Click Buy now and create your account. If you already have an existing one, choose to log in.

- Pick the pricing {plan, then a needed payment gateway, and purchase Montgomery Qualified Subchapter-S Trust for Benefit of Child with Crummey Trust Agreement.

- Choose to save the form template in any offered file format.

- Visit the My Forms tab to re-download the document.

If you're already subscribed to US Legal Forms, you can find the needed Montgomery Qualified Subchapter-S Trust for Benefit of Child with Crummey Trust Agreement, log in to your account, and download it. Needless to say, our website can’t replace a legal professional completely. If you need to deal with an extremely challenging situation, we recommend using the services of a lawyer to check your document before signing and filing it.

With over 25 years on the market, US Legal Forms became a go-to platform for many different legal forms for millions of customers. Become one of them today and get your state-specific paperwork with ease!