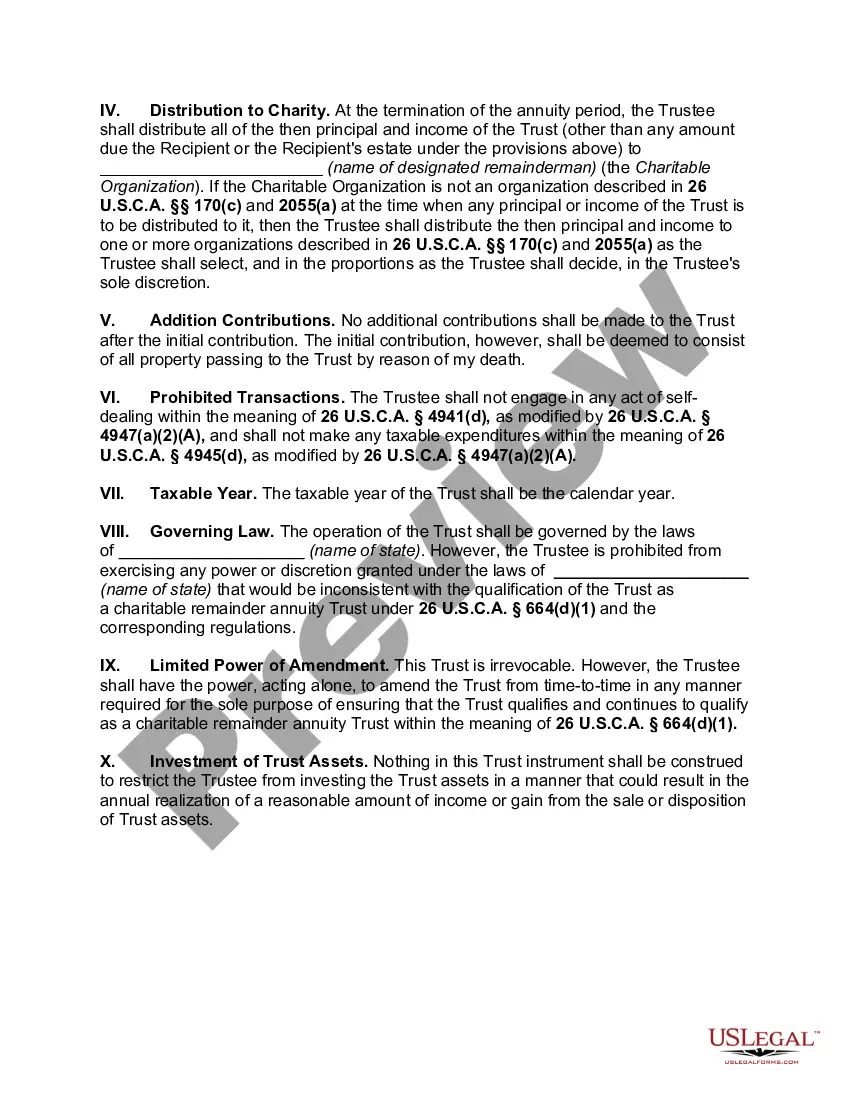

Chicago Illinois Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years refer to specific provisions in a will or trust document that dictate the establishment and operation of a Charitable Remainder Annuity Trust (CAT) in the state of Illinois, specifically in the city of Chicago. This specialized trust ensures a continuous stream of fixed income payments to one or more non-charitable beneficiaries for a set number of years or until their demise. The Chicago Illinois Testamentary Provisions for Charitable Remainder Annuity Trust for a Term of Years must adhere to the guidelines and regulations set forth by the Illinois state law. These provisions provide a framework for how the CAT will function, including the following key elements: 1. Charitable Intent: The testator's will or trust must express a clear intention to create a charitable remainder trust, specifying the assets to be placed in the trust, and naming the charitable organization(s) that will receive the remainder interest after the end of the term of years. 2. Trust Structure: The provisions define the terms of the trust, including the length of the term of years during which the non-charitable beneficiaries will receive fixed annuity payments from the trust. The provisions may also outline the possibility of early termination, conversion to a Charitable Remainder Unit rust (CUT), or other contingencies. 3. Payment Calculation: The provisions should include detailed instructions on how the annuity payout will be calculated. A fixed annuity payment, expressed as a percentage of the initial value of the trust assets, is distributed annually to the non-charitable beneficiary(IES) during the term of years. 4. Non-Charitable Beneficiaries: The trust provisions identify the individual(s) who will receive the fixed annuity payments during the specified term. Usually, these beneficiaries are family members or other loved ones, providing them with stable income, potentially minimizing estate taxes, and ultimately benefiting the designated charitable organization. 5. Qualified Charitable Organization: The trust provisions must clearly designate a qualified charitable organization to receive the remaining trust assets at the end of the term of years. The organization must be eligible under the Internal Revenue Code and registered with the Illinois Attorney General's Charitable Trust Bureau. It is worth mentioning that while the Chicago Illinois Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years provide a general framework, there may be variations and additional provisions depending on the specific circumstances and the individual's personal preferences. Some different types or variations of CAT provisions can include those with varying term lengths, provisions for inflation-adjusted annuity payments, contingent annuitant provisions allowing for possible changes in beneficiaries, and provisions that include charitable gift annuity options, among others. In summary, Chicago Illinois Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years are crucial components of estate planning for individuals in Chicago seeking to establish a trust that provides stable income to non-charitable beneficiaries for a specified time, with the remainder ultimately benefiting a designated charitable organization. These provisions outline the parameters of the trust, including the calculation and distribution of annuity payments, the identification of beneficiaries, and the designation of a qualified charitable organization.

Chicago Illinois Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years

Description

How to fill out Chicago Illinois Testamentary Provisions For Charitable Remainder Annuity Trust For Term Of Years?

Creating legal forms is a necessity in today's world. Nevertheless, you don't always need to look for professional help to create some of them from scratch, including Chicago Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years, with a service like US Legal Forms.

US Legal Forms has over 85,000 templates to select from in various types varying from living wills to real estate papers to divorce papers. All forms are arranged based on their valid state, making the searching process less frustrating. You can also find information materials and tutorials on the website to make any tasks related to paperwork execution simple.

Here's how you can locate and download Chicago Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years.

- Take a look at the document's preview and outline (if available) to get a basic information on what you’ll get after getting the form.

- Ensure that the document of your choice is specific to your state/county/area since state laws can impact the legality of some documents.

- Check the similar document templates or start the search over to locate the correct file.

- Click Buy now and register your account. If you already have an existing one, select to log in.

- Choose the option, then a needed payment method, and purchase Chicago Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years.

- Select to save the form template in any available format.

- Visit the My Forms tab to re-download the file.

If you're already subscribed to US Legal Forms, you can locate the needed Chicago Testamentary Provisions for Charitable Remainder Annuity Trust for Term of Years, log in to your account, and download it. Of course, our website can’t replace an attorney completely. If you need to deal with an exceptionally complicated case, we recommend using the services of an attorney to review your form before signing and filing it.

With over 25 years on the market, US Legal Forms proved to be a go-to platform for various legal forms for millions of customers. Become one of them today and get your state-compliant paperwork with ease!