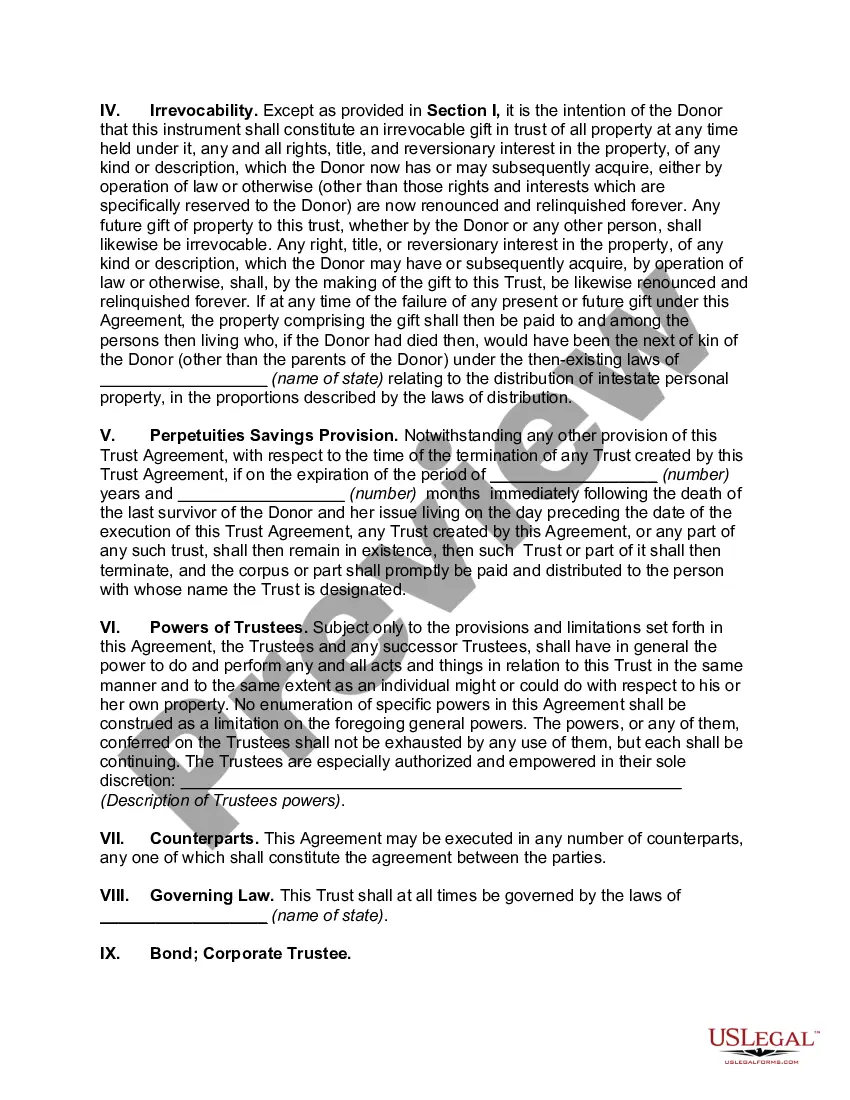

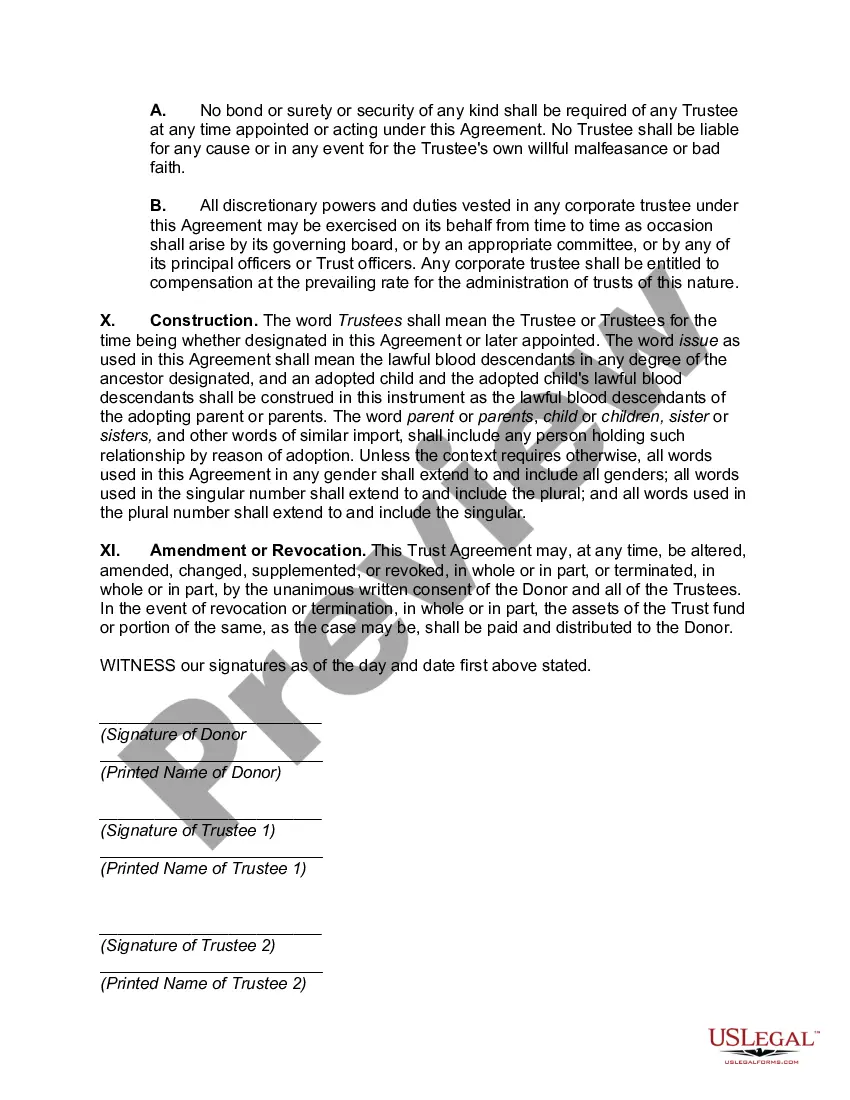

A Harris Texas Granter Retained Income Trust with Division into Trusts for Issue after Term of Years is a specialized estate planning tool that allows the granter to transfer assets onto a trust while retaining an income stream for a specified term of years. This type of trust is commonly utilized to reduce the granter's taxable estate, protect assets, and transfer wealth to their beneficiaries. The Harris Texas Granter Retained Income Trust with Division into Trusts for Issue after Term of Years can be divided into two primary types: the Granter Retained Annuity Trust (GREAT) and the Granter Retained Unit rust (GUT). 1. Granter Retained Annuity Trust (GREAT): A GREAT allows the granter to transfer assets into a trust and retain a fixed annuity payment for a specified term of years. The annuity payment is calculated based on the value of the assets transferred and an interest rate set by the IRS. At the end of the term, any remaining trust assets pass to the beneficiaries named by the granter. 2. Granter Retained Unit rust (GUT): In a GUT, the granter transfers assets into a trust but retains a fixed percentage of the trust's value as an annual income. The value of the income is recalculated annually based on the trust's total value. At the end of the specified term, the remaining assets are distributed to the beneficiaries. The Harris Texas Granter Retained Income Trust with Division into Trusts for Issue after Term of Years can be a powerful wealth transfer strategy. By placing assets into these trusts, granters may reduce estate taxes and potentially protect assets from creditors. It is important to work with an experienced attorney or financial advisor to determine the best trust structure and ensure compliance with IRS regulations. When establishing a Harris Texas Granter Retained Income Trust with Division into Trusts for Issue after Term of Years, it is essential to consider various factors like the value of the assets transferred, the length of the term, and the best candidates for named beneficiaries. Professional guidance should be sought to evaluate the potential tax implications, select appropriate trustees, and determine the specific terms of the trust. In summary, a Harris Texas Granter Retained Income Trust with Division into Trusts for Issue after Term of Years is a complex estate planning tool that allows individuals to transfer assets into a trust while retaining an income stream. The two main types of this trust are the Granter Retained Annuity Trust (GREAT) and the Granter Retained Unit rust (GUT). Proper consulting with professionals is crucial to ensure the trust is structured to suit individual goals and comply with regulations.

Harris Texas Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years

Description

How to fill out Harris Texas Grantor Retained Income Trust With Division Into Trusts For Issue After Term Of Years?

Do you need to quickly create a legally-binding Harris Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years or probably any other form to manage your own or corporate matters? You can select one of the two options: contact a professional to draft a legal document for you or create it completely on your own. Thankfully, there's another option - US Legal Forms. It will help you get neatly written legal paperwork without having to pay unreasonable prices for legal services.

US Legal Forms offers a huge collection of more than 85,000 state-specific form templates, including Harris Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years and form packages. We offer documents for a myriad of life circumstances: from divorce paperwork to real estate document templates. We've been out there for more than 25 years and got a rock-solid reputation among our customers. Here's how you can become one of them and obtain the needed document without extra hassles.

- First and foremost, carefully verify if the Harris Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years is tailored to your state's or county's laws.

- In case the document comes with a desciption, make sure to verify what it's intended for.

- Start the search again if the document isn’t what you were seeking by using the search bar in the header.

- Choose the subscription that best fits your needs and move forward to the payment.

- Choose the format you would like to get your document in and download it.

- Print it out, fill it out, and sign on the dotted line.

If you've already set up an account, you can easily log in to it, find the Harris Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years template, and download it. To re-download the form, just head to the My Forms tab.

It's effortless to buy and download legal forms if you use our services. Additionally, the paperwork we offer are reviewed by industry experts, which gives you greater confidence when dealing with legal affairs. Try US Legal Forms now and see for yourself!

Form popularity

FAQ

A GRAT is a type of trust that consists of two distinct terms: (i) a term of years (the GRAT term) during which the grantor of the GRAT receives an annuity payment based on the IRS rate in effect during the month the GRAT is funded and the fair market value of the assets used to fund the GRAT, and (ii) the remainder

Grantor Retained Income Trust, Definition A grantor retained income trust allows the person who creates the trust to transfer assets to it while still being able to receive net income from trust assets. The grantor maintains this right for a fixed number of years.

Grantor-Retained Income Trust (GRIT) is an old form of Grantor-Retained Trust set up by individuals to reduce taxes on an estate. To create a GRIT, a grantor creates an irrevocable trust that is for a limited period of time, paying taxes at the outset of the trust.

Upon the death of the grantor, grantor trust status terminates, and all pre-death trust activity must be reported on the grantor's final income tax return. As mentioned earlier, the once-revocable grantor trust will now be considered a separate taxpayer, with its own income tax reporting responsibility.

If the trust is a grantor trust, the income is taxed to the grantor even if the income and other distributions actually go to someone else. A nongrantor trust, by comparison, is taxed as its own separate taxpaying entity.

The annuity amount is paid to the grantor during the term of the GRAT, and any property remaining in the trust at the end of the GRAT term passes to the beneficiaries with no further gift tax consequences.

At the end of the initial term retained by the Grantor, if the Grantor is still living, the remainder beneficiaries (or a trust to be administered for the benefit of the remainder beneficiaries) receive $100,0000 plus all capital growth (which is the amount over and above the net income that was paid to the Grantor).

The 65-Day Rule applies only to complex trusts, because by definition, a simple trust's income is already taxed to the beneficiary at the beneficiary's presumably lower tax rate.

If the trust is a grantor trust, the income is taxed to the grantor even if the income and other distributions actually go to someone else. A nongrantor trust, by comparison, is taxed as its own separate taxpaying entity. The trustee of the trust has the trust file its own tax return, Form 1041.

Sales of assets between a grantor trust and its grantor are disregarded for income tax purposes, which allows sales to occur without triggering capital gains taxes. Distributions can be made from grantor trusts to beneficiaries of the trust without any gift tax consequence.