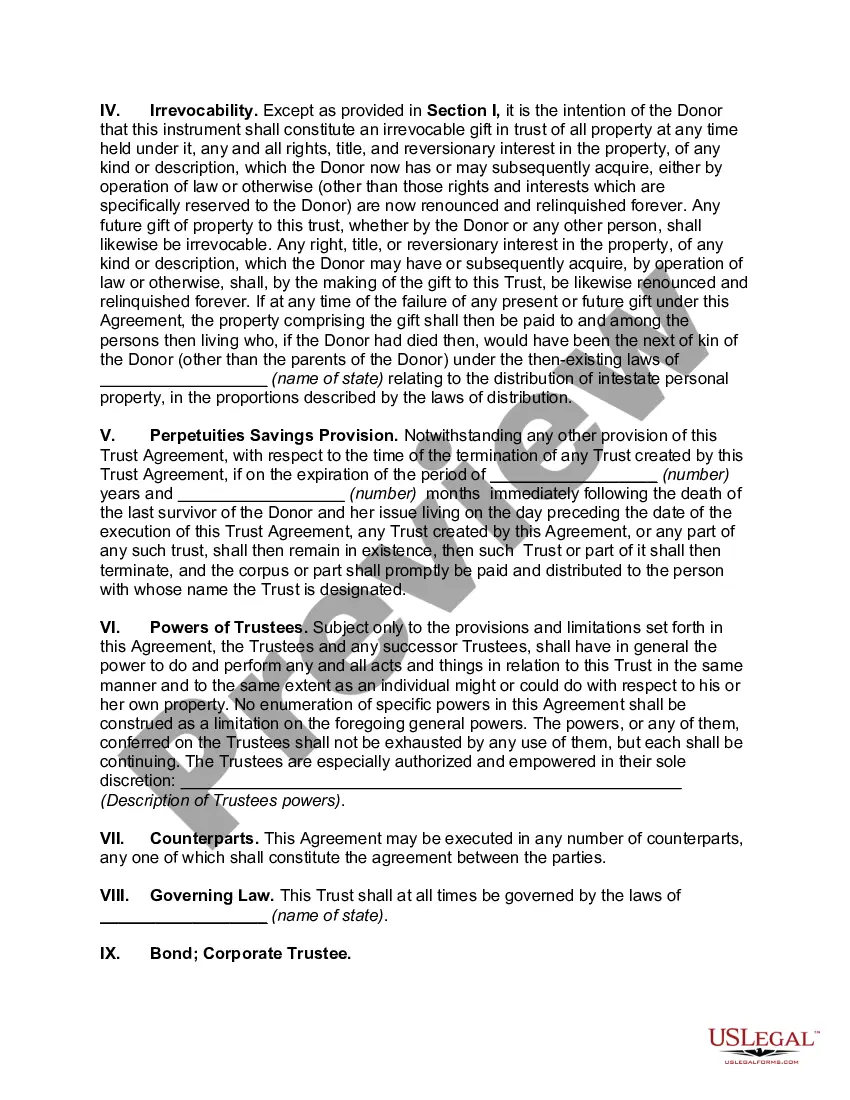

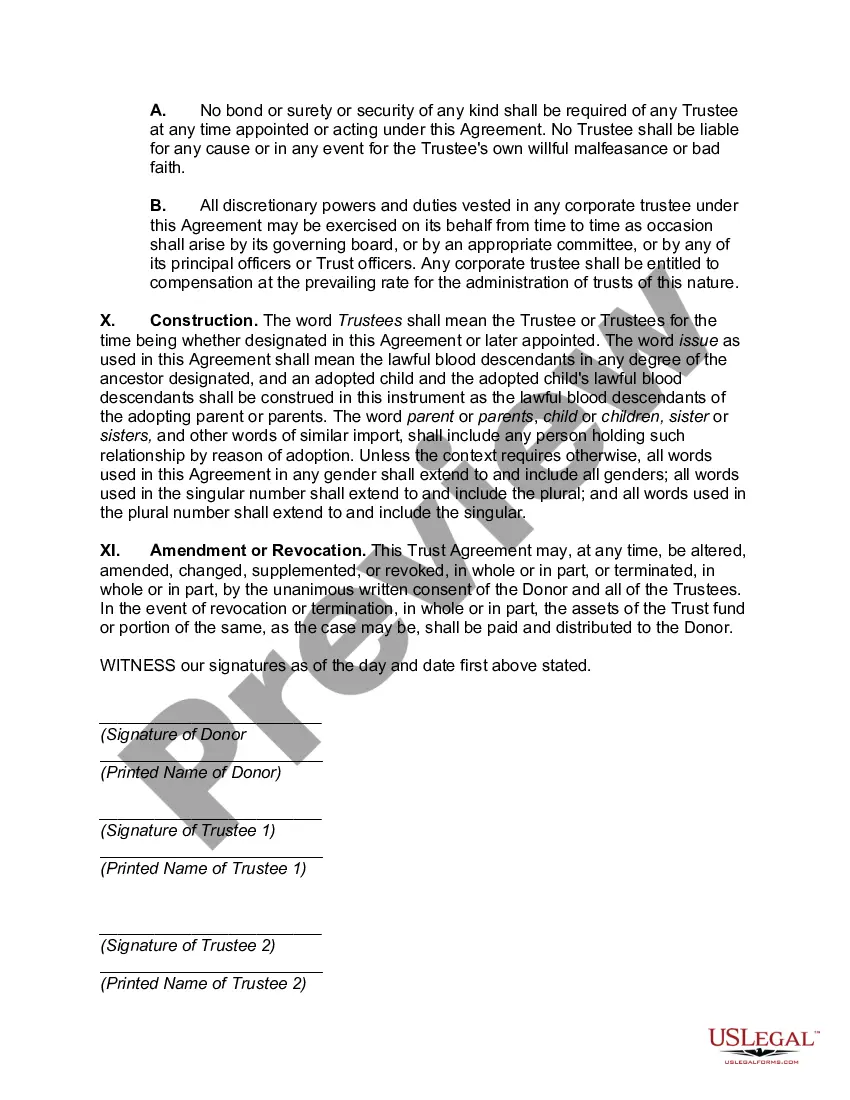

Queens New York Granter Retained Income Trust with Division into Trusts for Issue after Term of Years is a sophisticated estate planning tool that allows individuals to transfer assets to their beneficiaries while still maintaining control and receiving income during their lifetime. This type of trust is highly customizable and can be tailored to meet the specific needs and goals of the granter. A Granter Retained Income Trust (GRIT) is created when the granter transfers assets, such as real estate, stocks, or business interests, into an irrevocable trust and retains the right to receive income from the trust for a specified period of time. The income received by the granter from the trust is typically fixed, either as a fixed dollar amount or a percentage of the trust's value. The granter retains control over the trust during this period. The Division into Trusts for Issue after Term of Years is an additional feature that can be added to the Queens New York GRIT. This feature allows for the assets remaining in the trust after the specified term to be divided into separate trusts for the benefit of the granter's chosen beneficiaries, typically their children or grandchildren. The division into trusts ensures that the assets are protected and distributed according to the granter's wishes after their passing. This estate planning strategy offers several benefits. Firstly, it allows the granter to enjoy a steady stream of income during their lifetime. This can be particularly useful for individuals who rely on the income generated by their assets for their day-to-day expenses. Secondly, it allows for the transfer of wealth to future generations with potential tax advantages. By transferring assets to the trust, the granter removes them from their taxable estate, potentially reducing estate taxes upon their passing. Some types of Queens New York Granter Retained Income Trusts with Division into Trusts for Issue after Term of Years include: 1. One-generation GRIT: This type of GRIT allows the granter to retain income for a specific period, usually their lifetime, and then distribute the remaining assets to their chosen beneficiaries. 2. Multi-generation GRIT: This GRIT extends the period during which the granter retains income beyond their lifetime. The income may continue to be distributed to their children or grandchildren over several generations before the remaining assets are eventually divided into separate trusts. 3. Charitable GRIT: In this type of GRIT, the income generated from the trust is directed towards a charitable organization or foundation of the granter's choice. After the specified term, the remaining assets can be distributed to both charitable and non-charitable beneficiaries. Queens New York Granter Retained Income Trust with Division into Trusts for Issue after Term of Years offers individuals a powerful estate planning option to control their assets, receive income during their lifetime, and efficiently transfer wealth to future generations. It is advisable to consult with a qualified estate planning attorney to understand the legal and financial implications of this trust and to create a personalized plan that aligns with one's unique circumstances and goals.

Queens New York Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years

Description

How to fill out Queens New York Grantor Retained Income Trust With Division Into Trusts For Issue After Term Of Years?

Drafting paperwork for the business or individual demands is always a huge responsibility. When creating a contract, a public service request, or a power of attorney, it's essential to consider all federal and state laws and regulations of the particular area. However, small counties and even cities also have legislative provisions that you need to consider. All these details make it stressful and time-consuming to generate Queens Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years without professional help.

It's possible to avoid spending money on attorneys drafting your documentation and create a legally valid Queens Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years by yourself, using the US Legal Forms online library. It is the most extensive online catalog of state-specific legal documents that are professionally verified, so you can be certain of their validity when selecting a sample for your county. Previously subscribed users only need to log in to their accounts to download the needed document.

In case you still don't have a subscription, follow the step-by-step guideline below to obtain the Queens Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years:

- Examine the page you've opened and verify if it has the sample you need.

- To accomplish this, use the form description and preview if these options are presented.

- To locate the one that suits your requirements, use the search tab in the page header.

- Recheck that the sample complies with juridical standards and click Buy Now.

- Opt for the subscription plan, then sign in or create an account with the US Legal Forms.

- Use your credit card or PayPal account to pay for your subscription.

- Download the chosen document in the preferred format, print it, or complete it electronically.

The exceptional thing about the US Legal Forms library is that all the documentation you've ever acquired never gets lost - you can get it in your profile within the My Forms tab at any moment. Join the platform and quickly get verified legal forms for any situation with just a couple of clicks!

Form popularity

FAQ

For the election to be valid, the election form must be filed not later than the time prescribed under section 6072 for filing the Form 1041 for the first taxable year of the trust, taking into account the trustee's election to treat the trust as an estate under section 645 (regardless of whether there is sufficient

Key Takeaways. Grantor retained annuity trusts (GRATs) are estate planning instruments in which a grantor locks assets in a trust from which they earn annual income. Upon expiry, the beneficiary receives the assets with minimal or no gift tax liability. GRATs are used by wealthy individuals to minimize tax liabilities.

The primary benefit of a Grantor Retained Annuity Trust (GRAT) is to freeze the value of a property transferred to the trust, typically business interests, securities, or real estate, so that the future appreciation on such property will pass estate tax-free to the Grantor's beneficiaries.

The IRC § 645 election is irrevocable once made. The election must be made on IRS Form 8855 (Election to Treat a Qualified Revocable Trust as Part of an Estate) by the due date, including extensions, of the estate's initial income tax return.

Well, a §645 election allows the executor of an estate and the trustee of a revocable trust to elect to treat the estate and the trust as one for tax purposes. Generally, estates have the ability to elect a fiscal year end or a calendar year end, whereas trusts default to a calendar year end.

The IRC § 645 election is irrevocable once made. The election must be made on IRS Form 8855 (Election to Treat a Qualified Revocable Trust as Part of an Estate) by the due date, including extensions, of the estate's initial income tax return.

At the end of the initial term retained by the Grantor, if the Grantor is still living, the remainder beneficiaries (or a trust to be administered for the benefit of the remainder beneficiaries) receive $100,0000 plus all capital growth (which is the amount over and above the net income that was paid to the Grantor).

Out GRAT is a GRAT where the annuity payable to the trust's creator is set in a manner that results, mathematically, in a net gift of zero.

To distribute real estate held by a trust to a beneficiary, the trustee will have to obtain a document known as a grant deed, which, if executed correctly and in accordance with state laws, transfers the title of the property from the trustee to the designated beneficiaries, who will become the new owners of the asset.

A GRIT is an irrevocable trust established in a written trust agreement whereby the creator of the trust (the Grantor) transfers assets to the GRIT while retaining the right to receive all of the net income from the trust assets for a fixed term of years (the initial term).