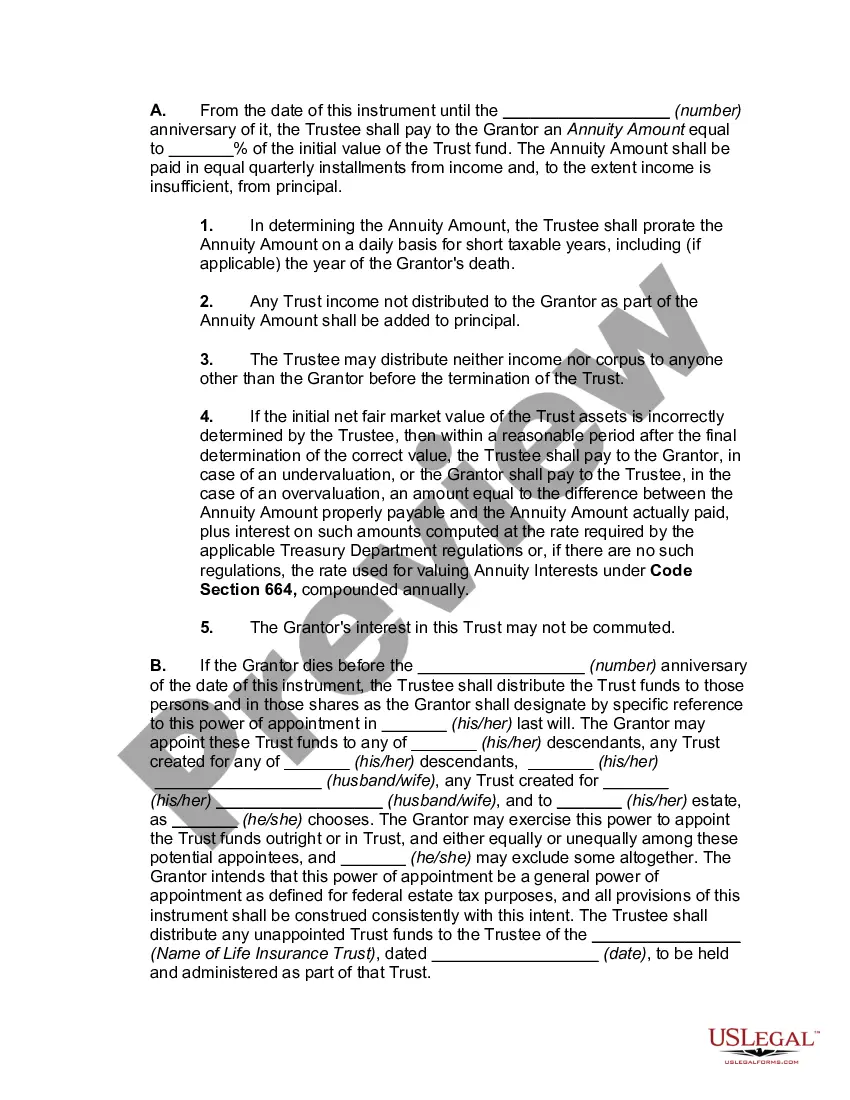

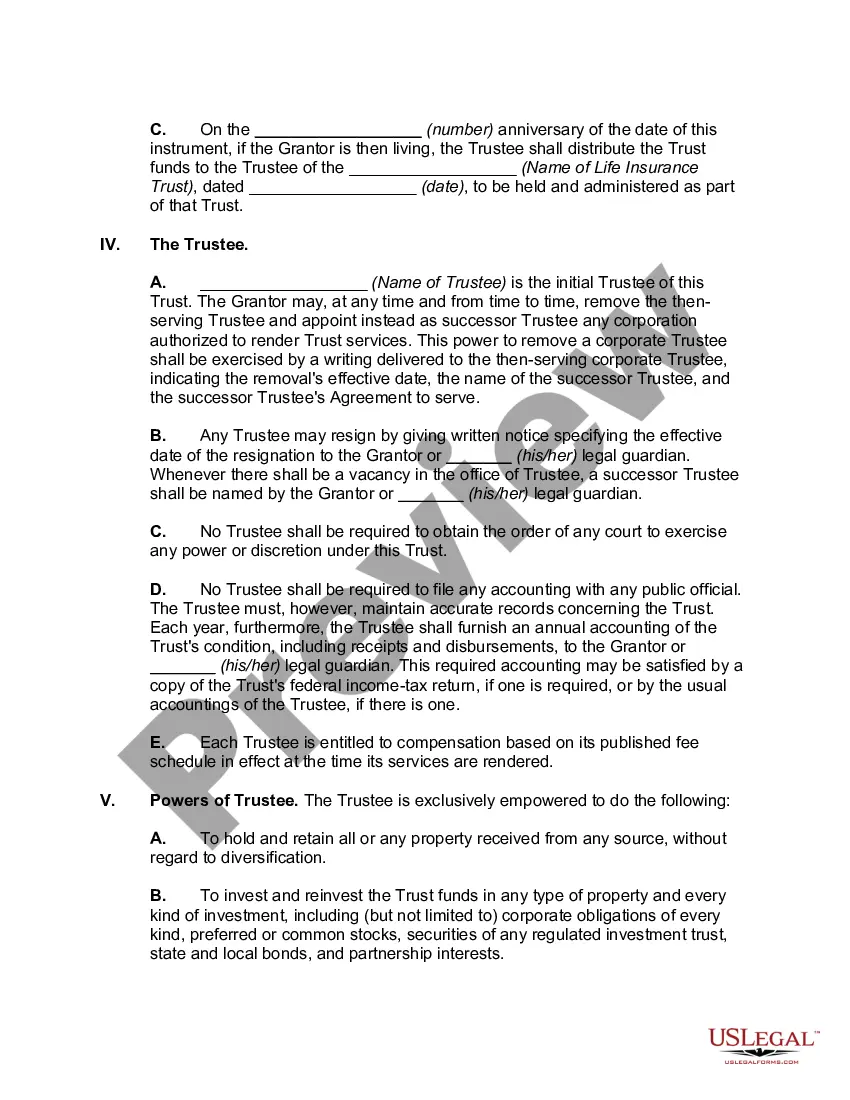

Allegheny, Pennsylvania Termination of Granter Retained Annuity Trust in Favor of Existing Life Insurance Trust is a legal process that allows individuals in Allegheny, Pennsylvania to terminate a Granter Retained Annuity Trust (GREAT) and transfer the assets into an Existing Life Insurance Trust (ELITE). This strategic move can be beneficial for individuals looking to maximize their estate planning and wealth preservation measures. A Granter Retained Annuity Trust (GREAT) is an irrevocable trust in which the granter transfers assets and retains an income stream from the trust for a specific period. The annuity payments are usually annual and reverts to the granter during the trust's existence. However, circumstances may arise where terminating the GREAT and transferring the assets to an Existing Life Insurance Trust (ELITE) becomes a more favorable option. By terminating the GREAT in favor of an ELITE, individuals can leverage life insurance policies to benefit their estate planning objectives. This process involves terminating the GREAT and distributing the assets into the ELITE, in which life insurance policies are purchased using the trust funds. Depending on individual circumstances and financial goals, there are different types of Allegheny Pennsylvania Termination of Granter Retained Annuity Trust in Favor of Existing Life Insurance Trust strategies: 1. GRAT-to-ELIT Conversion: This strategy involves terminating the GREAT and transferring its assets directly into an Existing Life Insurance Trust. The ELITE then acquires life insurance policies using the trust's funds, ensuring the growth and preservation of wealth for beneficiaries. 2. GREAT Rollover to FLAT (Charitable Lead Annuity Trust) then to ELITE: In this approach, the GREAT is terminated and rolled over into a Charitable Lead Annuity Trust, which pays a fixed annuity to a charitable organization for a specific period. After the charitable payments are completed, the remaining assets are transferred to the Existing Life Insurance Trust. 3. GREAT Rollover to a DGT (Dynasty Generation-Skipping Trust) then to ELITE: This strategy involves terminating the GREAT and rolling over its assets into a Dynasty Generation-Skipping Trust. The assets are then ultimately transferred to the Existing Life Insurance Trust. This approach is particularly useful for individuals aiming to pass on their wealth to future generations while minimizing estate taxes. By utilizing the Allegheny, Pennsylvania Termination of Granter Retained Annuity Trust in Favor of Existing Life Insurance Trust strategies, individuals can effectively manage their asset distributions, maximize wealth preservation, and ensure the financial security of their loved ones. It is crucial to consult with a qualified estate planning attorney or financial advisor to determine the most appropriate strategy based on individual goals, financial circumstances, and the applicable laws in Allegheny, Pennsylvania.

Allegheny Pennsylvania Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust

Description

How to fill out Allegheny Pennsylvania Termination Of Grantor Retained Annuity Trust In Favor Of Existing Life Insurance Trust?

How much time does it typically take you to draft a legal document? Because every state has its laws and regulations for every life sphere, locating a Allegheny Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust meeting all local requirements can be exhausting, and ordering it from a professional attorney is often costly. Numerous web services offer the most popular state-specific documents for download, but using the US Legal Forms library is most advantegeous.

US Legal Forms is the most extensive web collection of templates, grouped by states and areas of use. Aside from the Allegheny Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust, here you can get any specific document to run your business or personal affairs, complying with your county requirements. Professionals verify all samples for their actuality, so you can be certain to prepare your paperwork correctly.

Using the service is pretty simple. If you already have an account on the platform and your subscription is valid, you only need to log in, opt for the needed form, and download it. You can retain the file in your profile anytime later on. Otherwise, if you are new to the platform, there will be a few more steps to complete before you get your Allegheny Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust:

- Examine the content of the page you’re on.

- Read the description of the template or Preview it (if available).

- Search for another document utilizing the related option in the header.

- Click Buy Now when you’re certain in the chosen file.

- Select the subscription plan that suits you most.

- Sign up for an account on the platform or log in to proceed to payment options.

- Pay via PalPal or with your credit card.

- Change the file format if necessary.

- Click Download to save the Allegheny Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust.

- Print the doc or use any preferred online editor to complete it electronically.

No matter how many times you need to use the purchased template, you can find all the samples you’ve ever saved in your profile by opening the My Forms tab. Give it a try!

Form popularity

FAQ

out GRAT allows the grantor to transfer any appreciation in excess of the Sec. 7520 rate without using any of the grantor's lifetime exemption. If the assets fail to appreciate at the Sec. 7520 rate, the only cost to the grantor will have been the legal and administrative costs of setting up the GRAT.

The annuity amount is paid to the grantor during the term of the GRAT, and any property remaining in the trust at the end of the GRAT term passes to the beneficiaries with no further gift tax consequences.

The annuity payments cannot, however, be made in advance of the payment date. For that reason, it is important to consider the cash flow constraints on the grantor when deciding which assets will be used to fund the GRAT.

GRATs are taxed in two ways: Any income you earn from the appreciation of your assets in the trust is subject to regular income tax, and any remaining funds/assets that transfer to a beneficiary are subject to gift taxes.

The transfer of assets to a GRAT is a transfer to a trust and not to a grandchild. The generation-skipping transfer occurs when the grantor's interest in the GRAT terminates. Thus, GST exemption must be applied when the GRAT terminates and the ability to leverage the client's GST exemption is lost.

To implement this strategy, you zero out the grantor retained annuity trust by accepting combined payments that are equal to the entire value of the trust, including the anticipated appreciation. In theory, there would be nothing left for the beneficiary if the trust is really zeroed out.

Out GRAT is a GRAT where the annuity payable to the trust's creator is set in a manner that results, mathematically, in a net gift of zero.

Thus, the trustee cannot terminate the GRAT before expiration of the term of the grantor's qualified interest by distributing to the grantor and the remainder beneficiaries the actuarial value of their term and remainder interests, respectively.

A grantor retained annuity trust is a type of irrevocable gifting trust that allows a grantor or trustmaker to potentially pass a significant amount of wealth to the next generation with little or no gift tax cost.