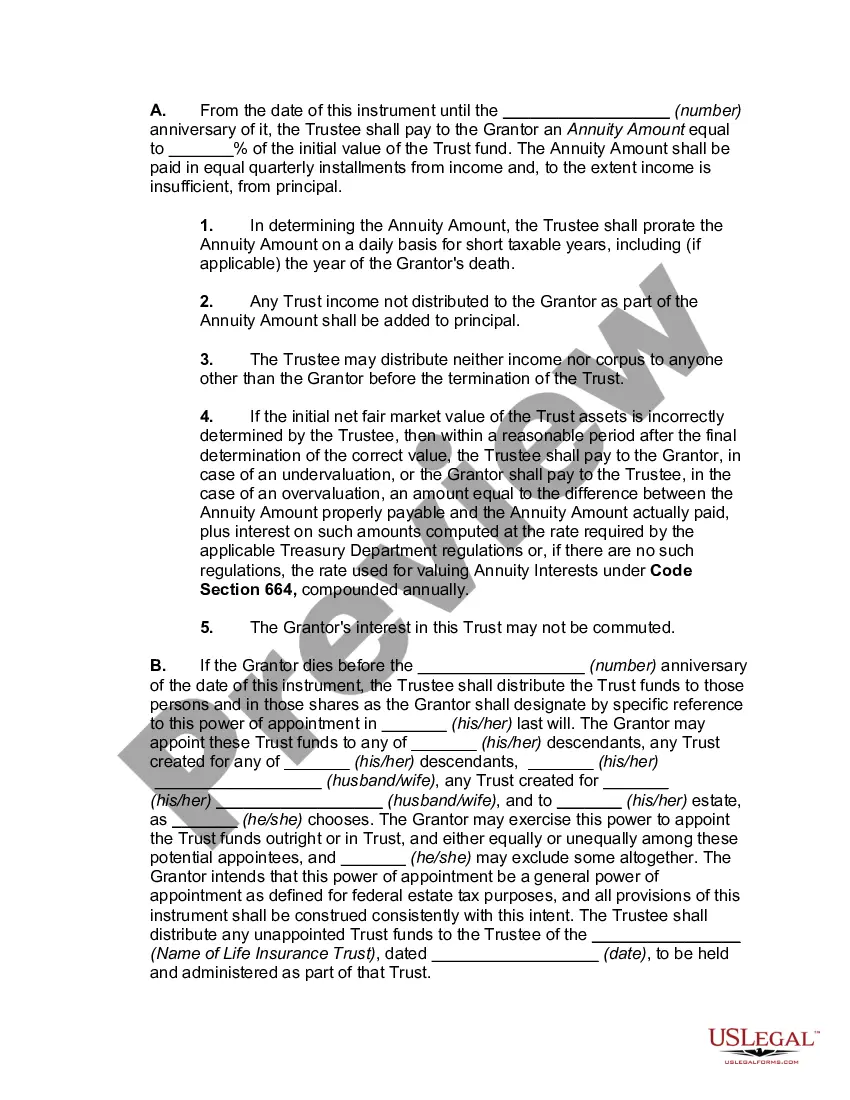

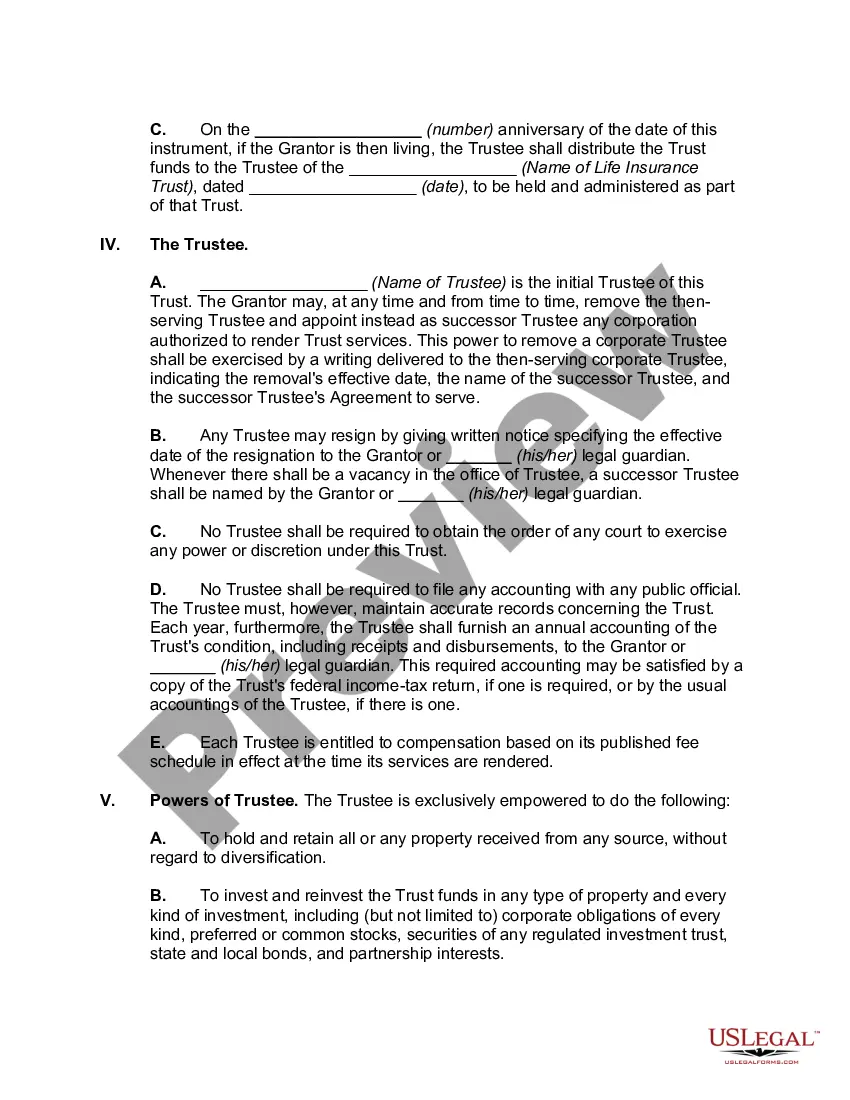

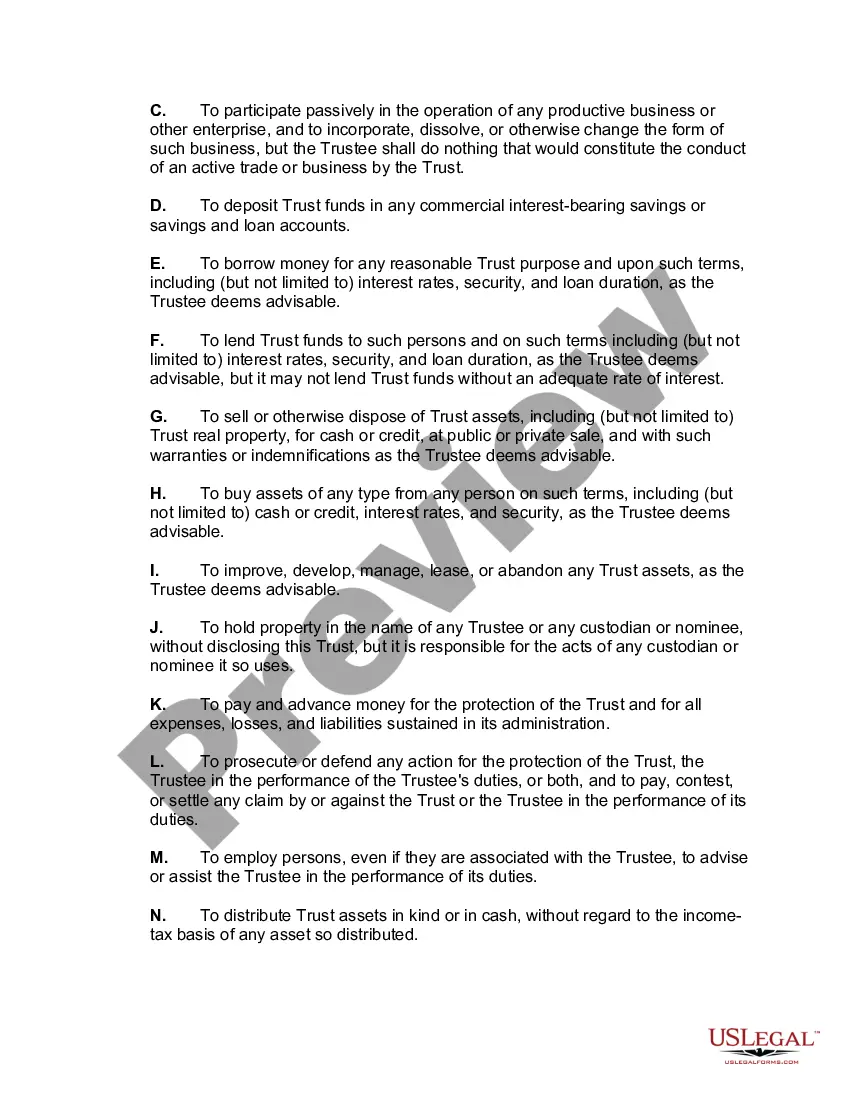

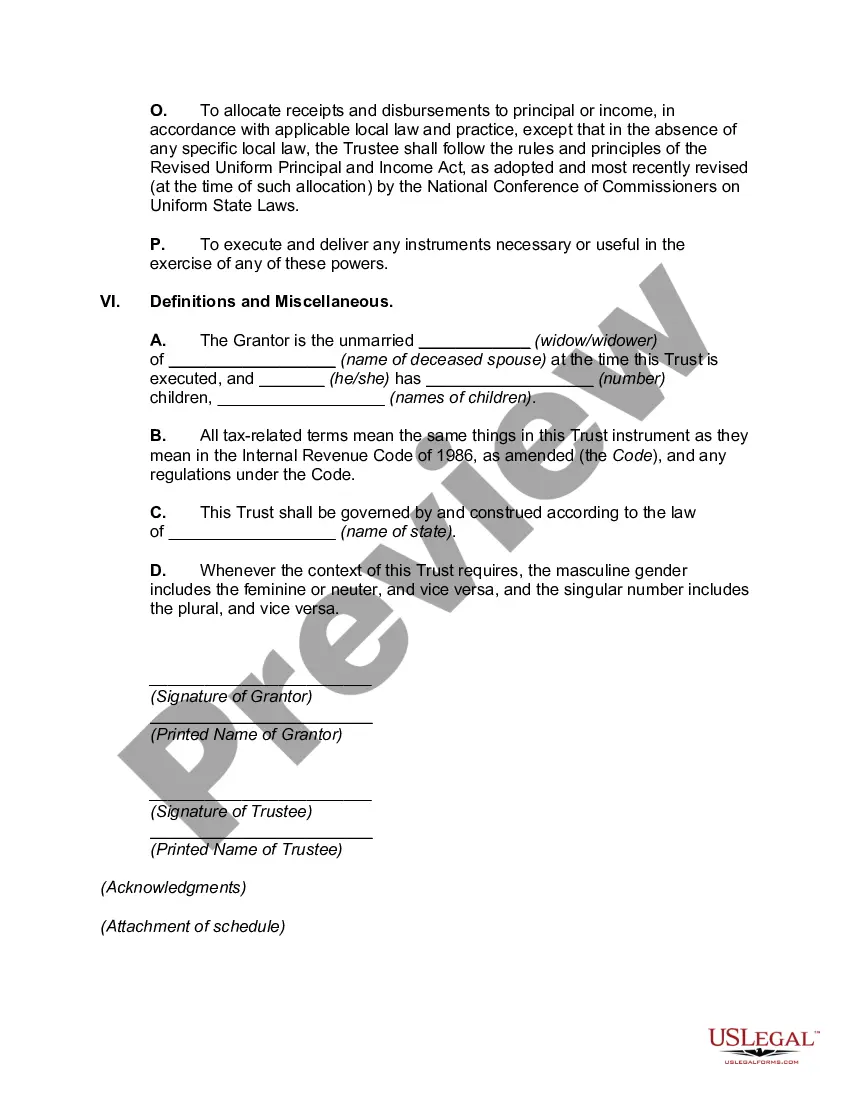

The King Washington Termination of Granter Retained Annuity Trust in Favor of Existing Life Insurance Trust refers to a legal process where a Granter Retained Annuity Trust (GREAT) is terminated in favor of an Existing Life Insurance Trust (IIT). This strategy allows individuals to maximize the value of their estate and efficiently transfer assets to beneficiaries while potentially minimizing estate taxes. In this specific arrangement, the Granter transfers assets into a GREAT, which pays the Granter an annuity for a predetermined period. At the end of the annuity term, any remaining assets pass to the designated beneficiaries, often at a reduced gift tax cost. However, in certain circumstances, it might be more beneficial to terminate the GREAT and establish an Existing IIT instead. The Existing IIT is a pre-existing trust that typically holds life insurance policies. By terminating the GREAT in favor of the IIT, the Granter can utilize the remaining assets to fund the IIT and purchase life insurance coverage. This ensures that the beneficiaries receive a tax-free death benefit upon the Granter's passing. Additionally, the Granter's annuity payments cease as the GREAT is terminated. The decision to terminate a GREAT in favor of an IIT depends on various factors, such as changes in tax laws, financial circumstances, and estate planning goals. By redirecting assets from the GREAT to the Existing IIT, individuals can potentially provide greater financial security and liquidity to their loved ones, as well as enhance the overall wealth transfer strategy. Some different types of King Washington Termination of Granter Retained Annuity Trust in Favor of Existing Life Insurance Trust include: 1. Traditional GREAT Termination: This refers to the termination of a standard GREAT in favor of an Existing IIT. It involves the transfer of assets remaining in the GREAT to the IIT to fund the life insurance policies. 2. GREAT Restructuring: In some cases, individuals may choose to restructure an existing GREAT to increase the likelihood of success. This may involve adjusting the annuity payments or term of the GREAT before considering termination in favor of an Existing IIT. 3. Hybrid GREAT Termination: Hybrid Grants have certain features that aim to reduce the potential downside of a failed GREAT. In the event that a hybrid GREAT shows signs of underperforming, termination in favor of an Existing IIT could be an alternative solution. It is crucial to consult with experienced estate planning professionals and financial advisors to determine the most suitable option based on individual circumstances and goals. Estate planning can be complex, so seeking expert advice is vital to ensure the appropriate strategy is implemented.

King Washington Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust

Description

How to fill out King Washington Termination Of Grantor Retained Annuity Trust In Favor Of Existing Life Insurance Trust?

How much time does it usually take you to create a legal document? Given that every state has its laws and regulations for every life sphere, locating a King Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust meeting all local requirements can be stressful, and ordering it from a professional lawyer is often expensive. Many online services offer the most common state-specific templates for download, but using the US Legal Forms library is most beneficial.

US Legal Forms is the most comprehensive online catalog of templates, gathered by states and areas of use. Aside from the King Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust, here you can get any specific document to run your business or individual affairs, complying with your regional requirements. Professionals verify all samples for their validity, so you can be certain to prepare your documentation properly.

Using the service is fairly easy. If you already have an account on the platform and your subscription is valid, you only need to log in, pick the required sample, and download it. You can pick the file in your profile at any moment in the future. Otherwise, if you are new to the website, there will be a few more steps to complete before you obtain your King Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust:

- Check the content of the page you’re on.

- Read the description of the template or Preview it (if available).

- Look for another document using the related option in the header.

- Click Buy Now when you’re certain in the chosen file.

- Decide on the subscription plan that suits you most.

- Register for an account on the platform or log in to proceed to payment options.

- Make a payment via PalPal or with your credit card.

- Switch the file format if necessary.

- Click Download to save the King Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust.

- Print the sample or use any preferred online editor to fill it out electronically.

No matter how many times you need to use the acquired document, you can find all the samples you’ve ever saved in your profile by opening the My Forms tab. Try it out!