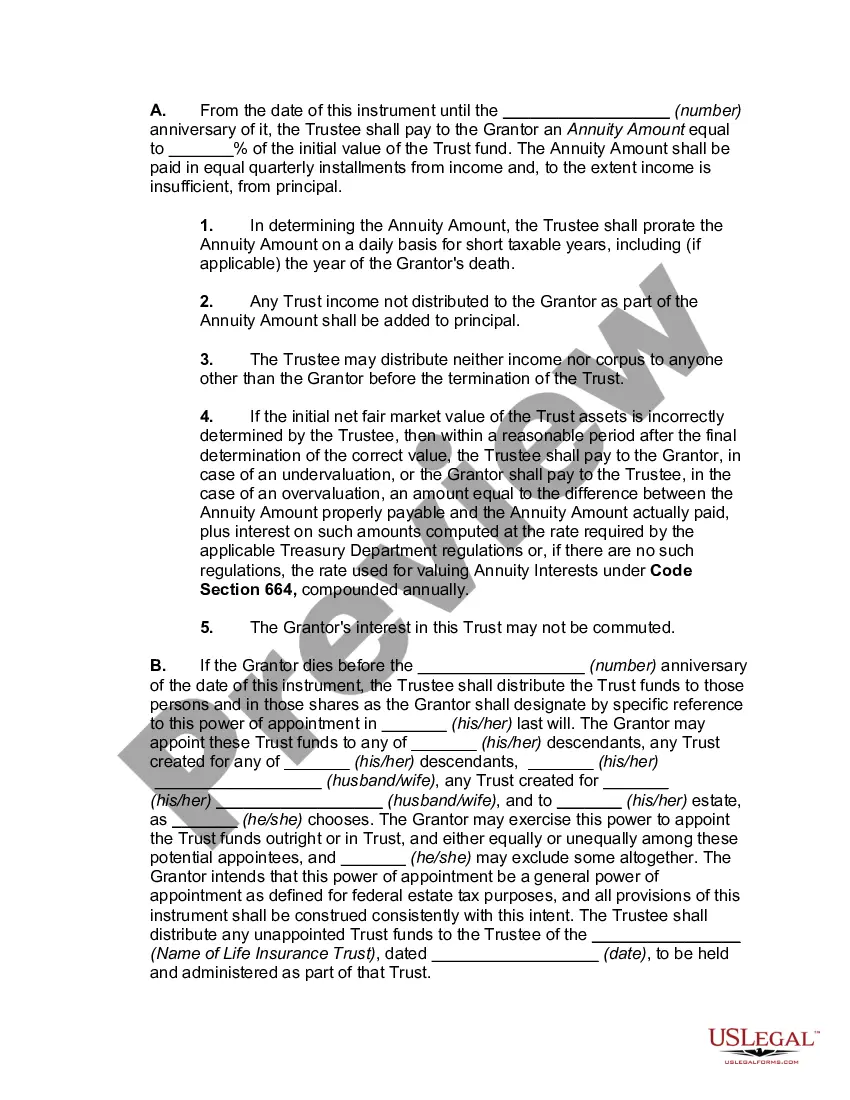

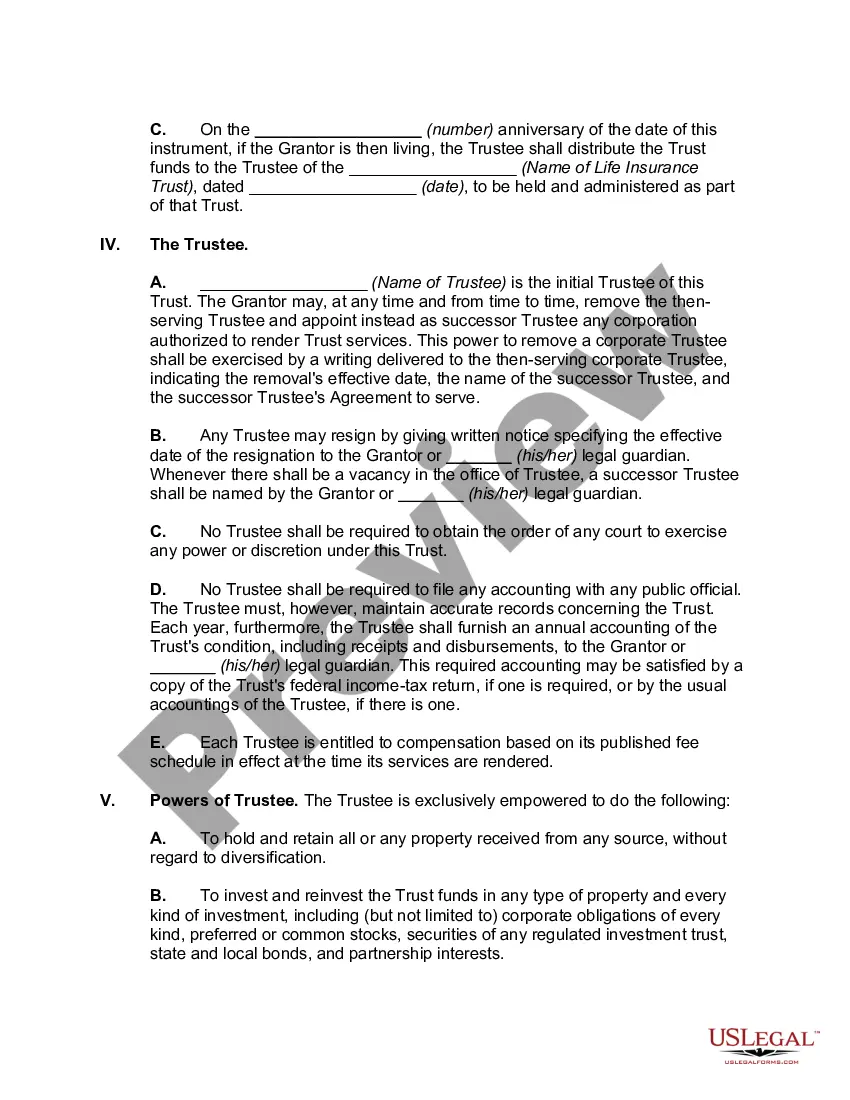

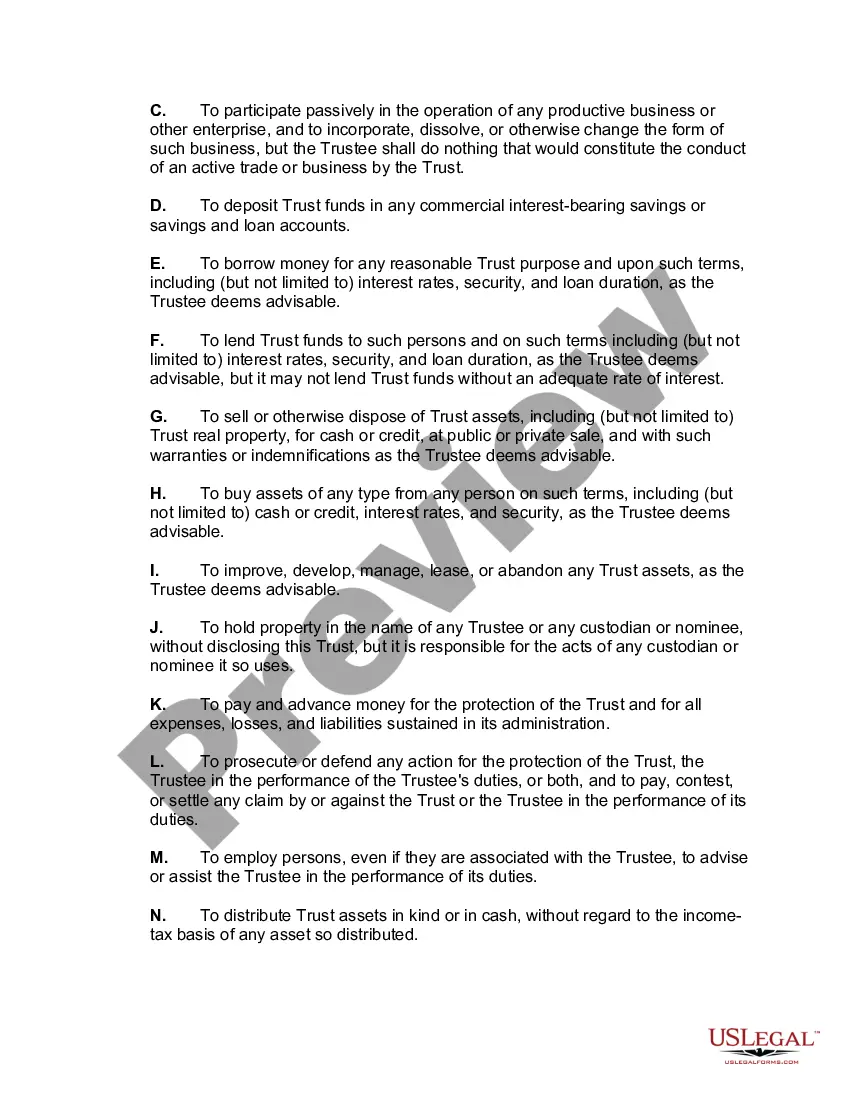

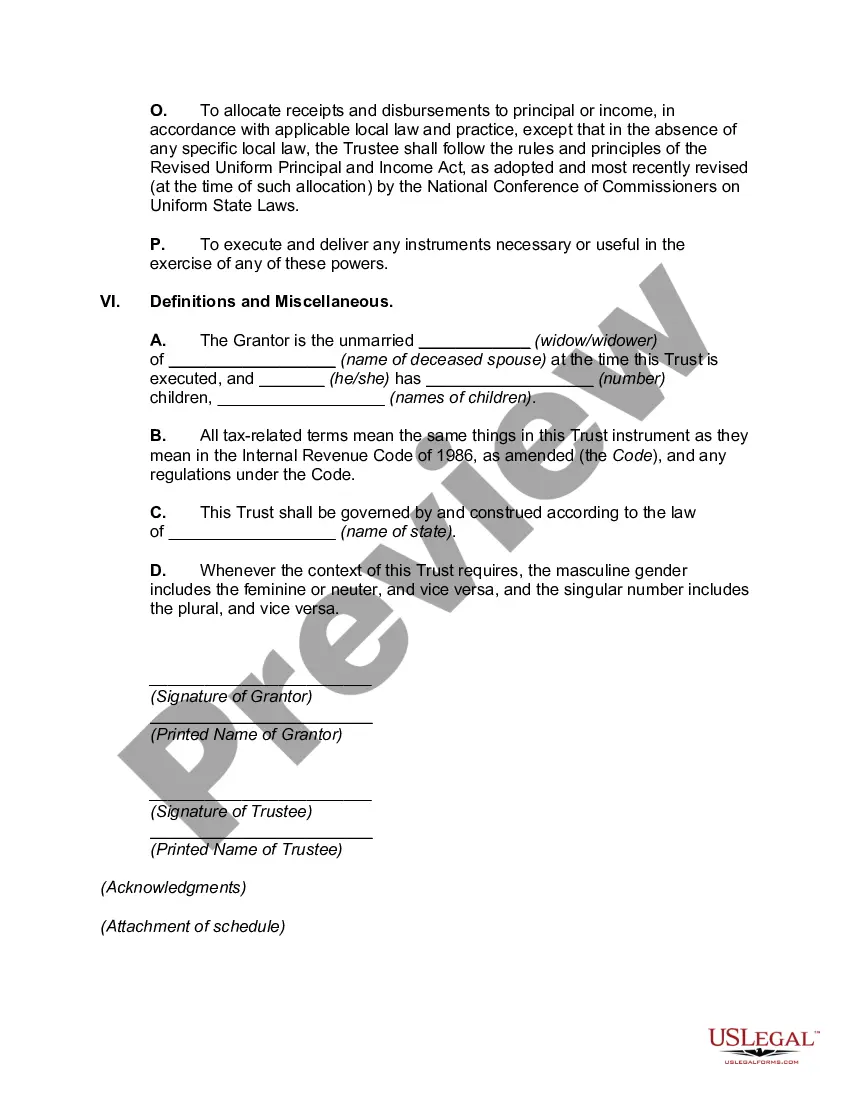

Mecklenburg North Carolina Termination of Granter Retained Annuity Trust in Favor of Existing Life Insurance Trust is a legal process that allows a granter to terminate a granter retained annuity trust (GREAT) and transfer its assets into an existing life insurance trust (IIT). This strategic decision is often made due to various factors, such as changes in estate planning goals or tax considerations. One type of Mecklenburg North Carolina Termination of Granter Retained Annuity Trust in Favor of Existing Life Insurance Trust is the "Simple Termination." This occurs when the granter decides to end the GREAT and direct its assets to an established IIT. The IIT then becomes the new owner and beneficiary of the assets, providing potential tax advantages and preserving wealth for future generations. Another type is the "Rolling GREAT Termination." With this approach, multiple Grants are created over time, and the granter terminates them one by one, transferring their assets into the existing IIT. This method allows for a continuous flow of assets from the Grants to the IIT, ensuring ongoing tax efficiency and wealth preservation. The "Step-Up GREAT Termination" is another variation of terminating a GREAT in favor of an existing IIT. This approach involves utilizing a stepped-up basis in assets upon the granter's death, which can provide significant tax benefits. By terminating the GREAT and transferring the assets to the IIT, the potential tax liability on the appreciated assets is potentially eliminated. In Mecklenburg North Carolina, the Termination of Granter Retained Annuity Trust in Favor of Existing Life Insurance Trust requires careful planning and legal expertise. It is crucial to consider factors such as the granter's specific financial situation, estate planning goals, and potential tax implications. Consulting with an experienced estate planning attorney in Mecklenburg North Carolina is highly recommended navigating the complexities of this process successfully. Keywords: Mecklenburg North Carolina, Termination of Granter Retained Annuity Trust, Existing Life Insurance Trust, estate planning, GREAT, IIT, tax considerations, wealth preservation, Simple Termination, Rolling GREAT Termination, Step-Up GREAT Termination, stepped-up basis, tax liability, legal expertise, estate planning attorney.

Mecklenburg North Carolina Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust

Description

How to fill out Mecklenburg North Carolina Termination Of Grantor Retained Annuity Trust In Favor Of Existing Life Insurance Trust?

Creating documents, like Mecklenburg Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust, to take care of your legal affairs is a tough and time-consumming process. Many circumstances require an attorney’s participation, which also makes this task expensive. However, you can consider your legal issues into your own hands and take care of them yourself. US Legal Forms is here to save the day. Our website features more than 85,000 legal documents intended for various cases and life situations. We make sure each form is compliant with the regulations of each state, so you don’t have to be concerned about potential legal problems associated with compliance.

If you're already familiar with our website and have a subscription with US, you know how straightforward it is to get the Mecklenburg Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust form. Simply log in to your account, download the template, and personalize it to your requirements. Have you lost your form? Don’t worry. You can find it in the My Forms tab in your account - on desktop or mobile.

The onboarding flow of new users is fairly straightforward! Here’s what you need to do before downloading Mecklenburg Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust:

- Make sure that your form is specific to your state/county since the regulations for creating legal paperwork may differ from one state another.

- Find out more about the form by previewing it or reading a brief description. If the Mecklenburg Termination of Grantor Retained Annuity Trust in Favor of Existing Life Insurance Trust isn’t something you were hoping to find, then take advantage of the search bar in the header to find another one.

- Log in or register an account to start using our website and get the form.

- Everything looks great on your end? Hit the Buy now button and choose the subscription option.

- Select the payment gateway and enter your payment details.

- Your form is ready to go. You can try and download it.

It’s an easy task to locate and purchase the appropriate template with US Legal Forms. Thousands of organizations and individuals are already taking advantage of our extensive collection. Sign up for it now if you want to check what other benefits you can get with US Legal Forms!