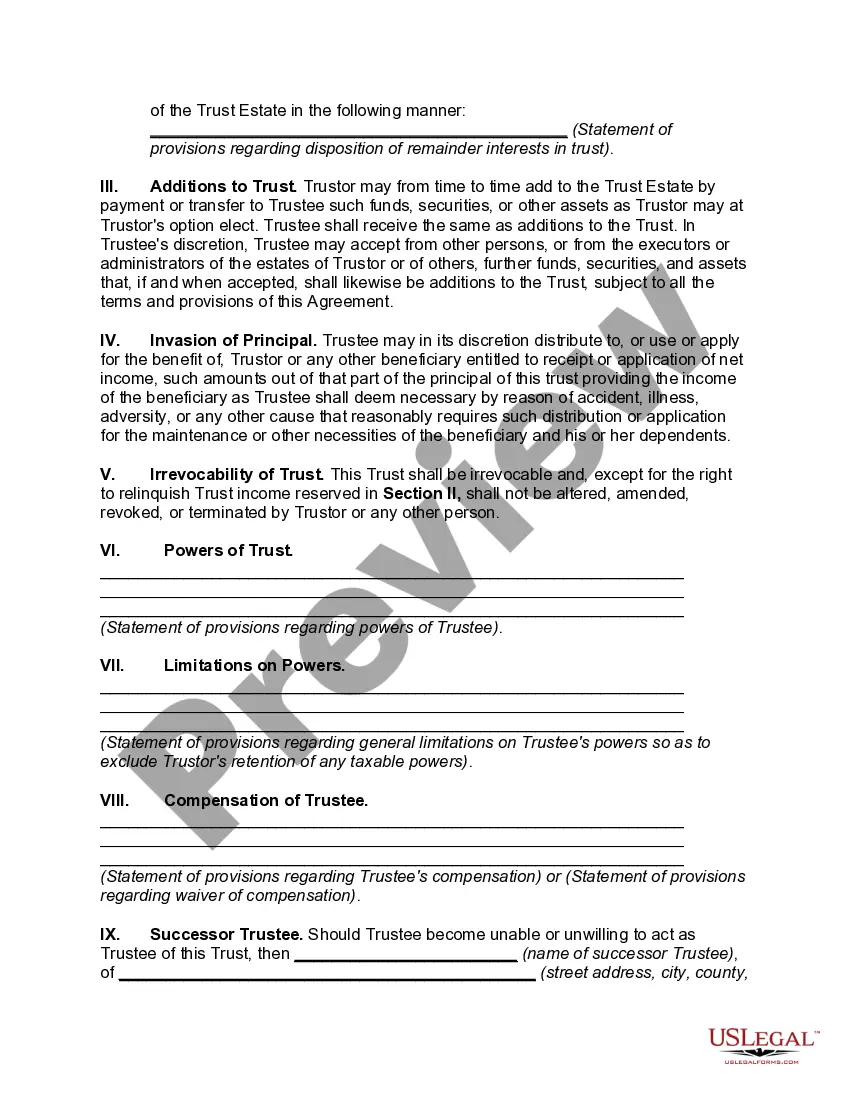

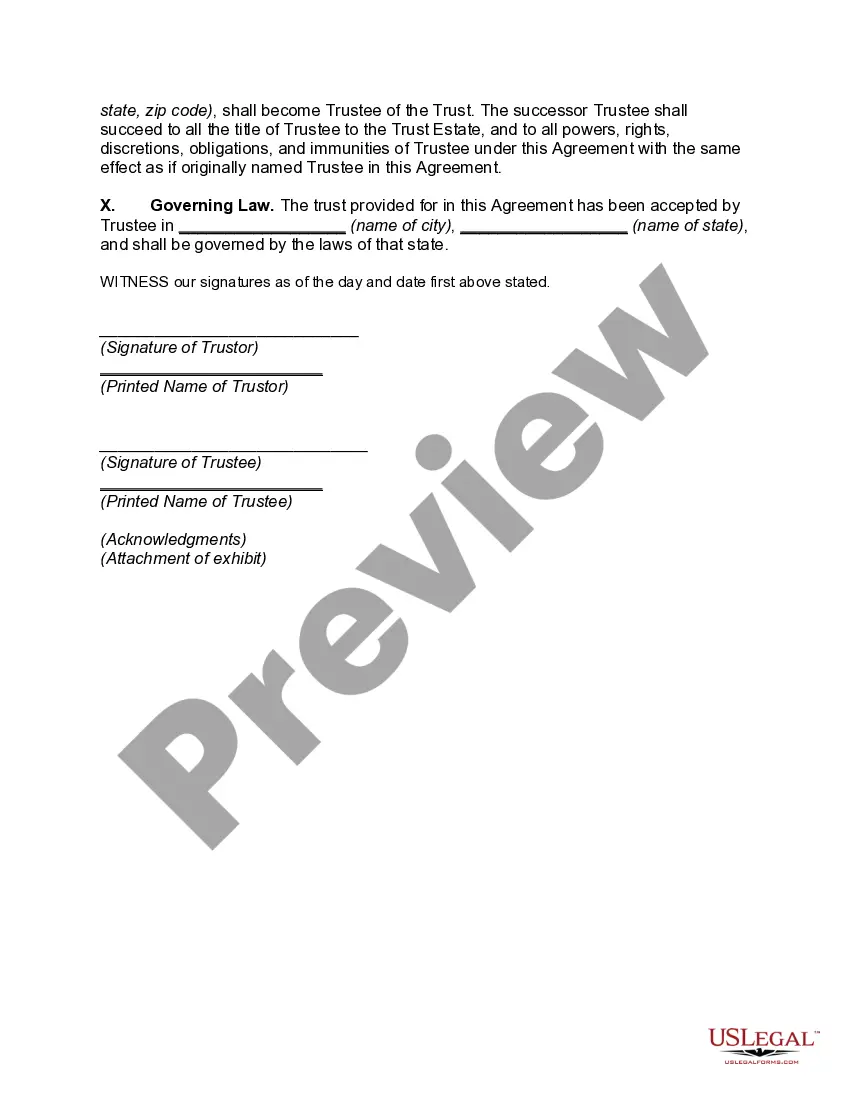

Palm Beach Florida Irrevocable Trust for Future Benefit of Trustor with Income Payable to Trustor after Specified Time

Description

How to fill out Palm Beach Florida Irrevocable Trust For Future Benefit Of Trustor With Income Payable To Trustor After Specified Time?

Dealing with legal forms is a must in today's world. Nevertheless, you don't always need to seek professional help to create some of them from scratch, including Palm Beach Irrevocable Trust for Future Benefit of Trustor with Income Payable to Trustor after Specified Time, with a service like US Legal Forms.

US Legal Forms has over 85,000 templates to pick from in various types ranging from living wills to real estate papers to divorce documents. All forms are organized according to their valid state, making the searching experience less frustrating. You can also find detailed materials and tutorials on the website to make any activities related to document completion simple.

Here's how you can find and download Palm Beach Irrevocable Trust for Future Benefit of Trustor with Income Payable to Trustor after Specified Time.

- Take a look at the document's preview and outline (if available) to get a basic information on what you’ll get after downloading the form.

- Ensure that the document of your choice is specific to your state/county/area since state laws can impact the legality of some documents.

- Check the similar forms or start the search over to find the correct file.

- Hit Buy now and create your account. If you already have an existing one, choose to log in.

- Pick the option, then a suitable payment method, and purchase Palm Beach Irrevocable Trust for Future Benefit of Trustor with Income Payable to Trustor after Specified Time.

- Select to save the form template in any available format.

- Visit the My Forms tab to re-download the file.

If you're already subscribed to US Legal Forms, you can find the needed Palm Beach Irrevocable Trust for Future Benefit of Trustor with Income Payable to Trustor after Specified Time, log in to your account, and download it. Needless to say, our platform can’t take the place of a lawyer entirely. If you have to cope with an exceptionally challenging case, we recommend using the services of a lawyer to examine your form before executing and filing it.

With over 25 years on the market, US Legal Forms proved to be a go-to platform for many different legal forms for millions of customers. Join them today and get your state-compliant paperwork with ease!

Form popularity

FAQ

An irrevocable trust reports income on Form 1041, the IRS's trust and estate tax return. Even if a trust is a separate taxpayer, it may not have to pay taxes. If it makes distributions to a beneficiary, the trust will take a distribution deduction on its tax return and the beneficiary will receive IRS Schedule K-1.

GrantorIf you are the grantor of an irrevocable grantor trust, then you will need to pay the taxes due on trust income from your own assetsrather than from assets held in the trustand to plan accordingly for this expense.

Assets transferred by a grantor to an irrevocable trusts are generally not part of the grantor's taxable estate for the purposes of the estate tax. This means that the assets will pass to the beneficiaries without being subject to estate tax.

Irrevocable trusts are generally set up to minimize estate taxes, access government benefits, and protect assets. This is in contrast to a revocable trust, which allows the grantor to modify the trust, but loses certain benefits such as creditor protection.

One of the greatest advantages of an irrevocable trust is that it can offer great protection from future creditors and lawsuits as well as bad marriages.

This allows you to sell assets or add new ones. When you create an irrevocable trust, however, you must appoint someone else as trustee, at least if you're going to reap all the legal benefits such a trust offers. In this case, only your trustee can add assets to your trust after you form it you've given up control.

Once money is placed into the trust, the interest it accumulates is taxable as income, either to the beneficiary or the trust itself. The trust must pay taxes on any interest income it holds and does not distribute past year-end. Interest income the trust distributes is taxable to the beneficiary who receives it.

The grantor (as an individual or couple) transfers their assets to an irrevocable trust. However, unlike other irrevocable trusts, the grantor can be the income beneficiary. Their children or spouse would be the residual beneficiaries.

Generally, taxpayers who have large estates are the ones who benefit the most from having an irrevocable trust. If you leave more than the IRS-allowed lifetime tax-free gift limit in estate assets to your beneficiaries, the amount over this tax-free limit is subject to a federal estate tax of 40 percent.

Beneficiaries of a trust typically pay taxes on the distributions they receive from the trust's income, rather than the trust itself paying the tax. However, such beneficiaries are not subject to taxes on distributions from the trust's principal.