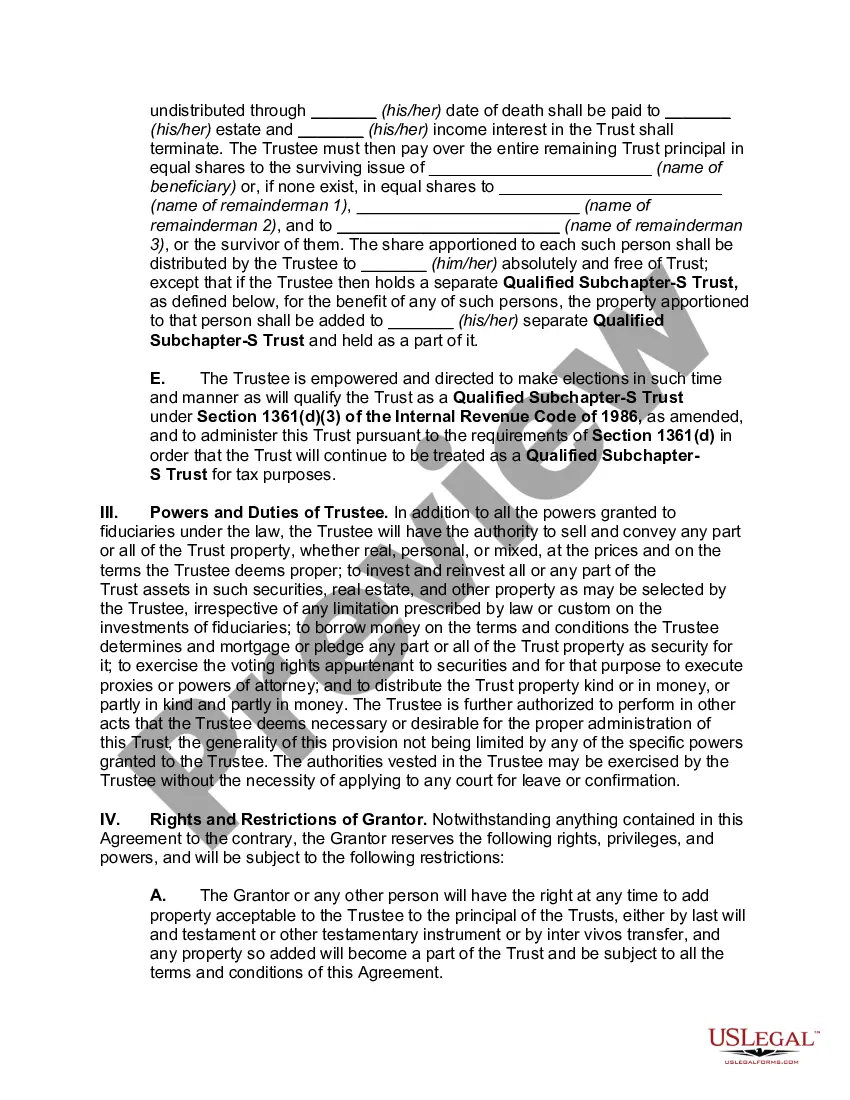

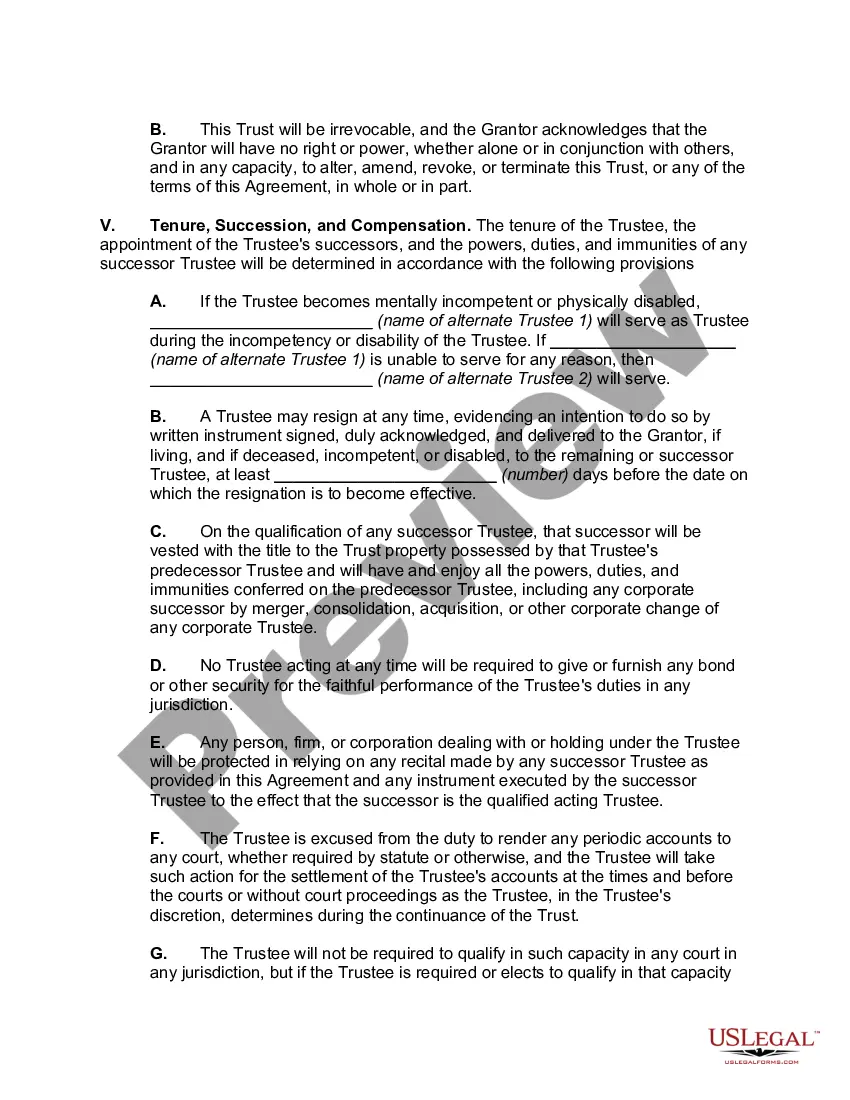

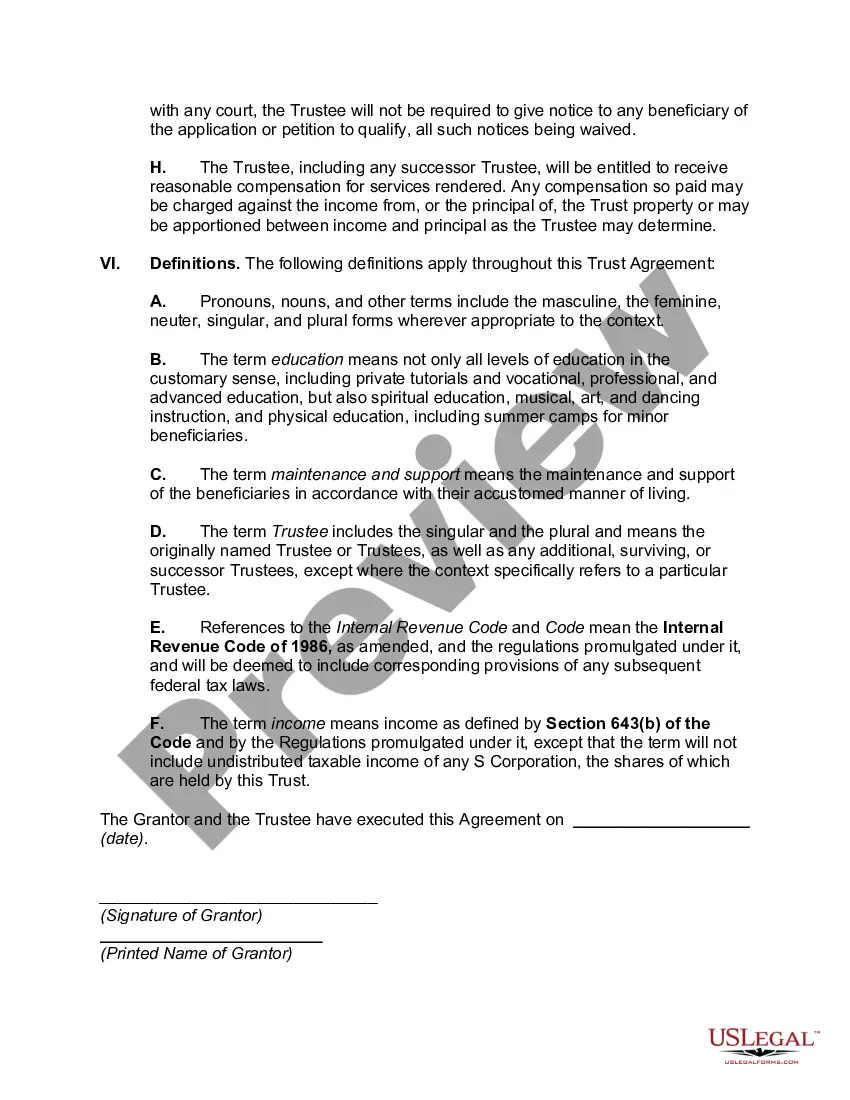

Maricopa, Arizona, offers individuals a unique estate planning option known as the Maricopa Arizona Irrevocable Trust, specifically designed as a Qualifying Subchapter-S Trust (SST). This trust, established in accordance with federal tax regulations, allows assets to be transferred, protected, and preserved for the benefits of beneficiaries while maintaining tax advantages. The Maricopa Arizona Irrevocable Trust is intended to ensure a smooth transfer of wealth, providing peace of mind to the granter and favorable tax treatment for the beneficiaries. By designating this trust as a qualifying Subchapter-S trust, it aligns itself with the rules and regulations outlined in the Internal Revenue Code (IRC) Section 1361(b)(3)(B). One of the primary benefits of the Maricopa Arizona Irrevocable Trust as an SST is the ability to retain the trust's status as a Subchapter S corporation, thereby avoiding double taxation. This unique feature allows income generated within the trust to pass directly to beneficiaries, who are then taxed at their individual income tax rates, rather than being subject to higher corporate tax rates. Moreover, the Maricopa Arizona Irrevocable Trust is specially crafted to meet various estate planning needs, leading to the creation of different types specific to individual circumstances. Here are a few notable variations: 1. Maricopa Arizona Irrevocable Life Insurance Trust (IIT): This trust variant holds life insurance policies outside the taxable estate. Upon the granter's passing, the trust receives the insurance proceeds, allowing for efficient estate settlement and potential estate tax reduction. 2. Maricopa Arizona Qualified Personnel Residence Trust (PRT): This trust variant allows the granter to transfer ownership of their primary residence or vacation home to the trust while retaining the right to live in it for a specified period. By doing so, the asset's value is potentially removed from the granter's estate for estate tax purposes. 3. Maricopa Arizona Granter Retained Annuity Trust (GREAT): An irrevocable trust variant in which the granter transfers assets while retaining an annuity payment back from the trust for a predetermined term. The remaining value of the assets, calculated using an IRS formula, is then passed on to beneficiaries. 4. Maricopa Arizona Charitable Remainder Trust (CRT): This trust allows the granter to donate appreciated assets while retaining an income stream for themselves or other beneficiaries for a specified period. At the end of the trust's term, the remaining assets are distributed to charitable organizations, providing potential income tax benefits. It is essential to consult with a qualified estate planning attorney or financial advisor to understand the intricacies and determine the most appropriate Maricopa Arizona Irrevocable Trust type, tailored to individual goals and objectives. The specific trust chosen will depend on the granter's assets, intended beneficiaries, and long-term objectives.

Maricopa Arizona Irrevocable Trust which is a Qualifying Subchapter-S Trust

Description

How to fill out Maricopa Arizona Irrevocable Trust Which Is A Qualifying Subchapter-S Trust?

Are you looking to quickly draft a legally-binding Maricopa Irrevocable Trust which is a Qualifying Subchapter-S Trust or maybe any other form to take control of your own or corporate matters? You can select one of the two options: contact a legal advisor to write a valid document for you or create it entirely on your own. Luckily, there's another solution - US Legal Forms. It will help you get professionally written legal documents without having to pay sky-high fees for legal services.

US Legal Forms provides a rich collection of more than 85,000 state-compliant form templates, including Maricopa Irrevocable Trust which is a Qualifying Subchapter-S Trust and form packages. We offer templates for a myriad of life circumstances: from divorce paperwork to real estate documents. We've been on the market for over 25 years and gained a spotless reputation among our clients. Here's how you can become one of them and get the needed document without extra hassles.

- First and foremost, carefully verify if the Maricopa Irrevocable Trust which is a Qualifying Subchapter-S Trust is adapted to your state's or county's regulations.

- In case the form includes a desciption, make sure to check what it's intended for.

- Start the searching process over if the document isn’t what you were hoping to find by using the search bar in the header.

- Choose the plan that best suits your needs and move forward to the payment.

- Select the format you would like to get your form in and download it.

- Print it out, fill it out, and sign on the dotted line.

If you've already set up an account, you can easily log in to it, find the Maricopa Irrevocable Trust which is a Qualifying Subchapter-S Trust template, and download it. To re-download the form, simply go to the My Forms tab.

It's easy to find and download legal forms if you use our catalog. Moreover, the paperwork we provide are reviewed by industry experts, which gives you greater confidence when dealing with legal affairs. Try US Legal Forms now and see for yourself!