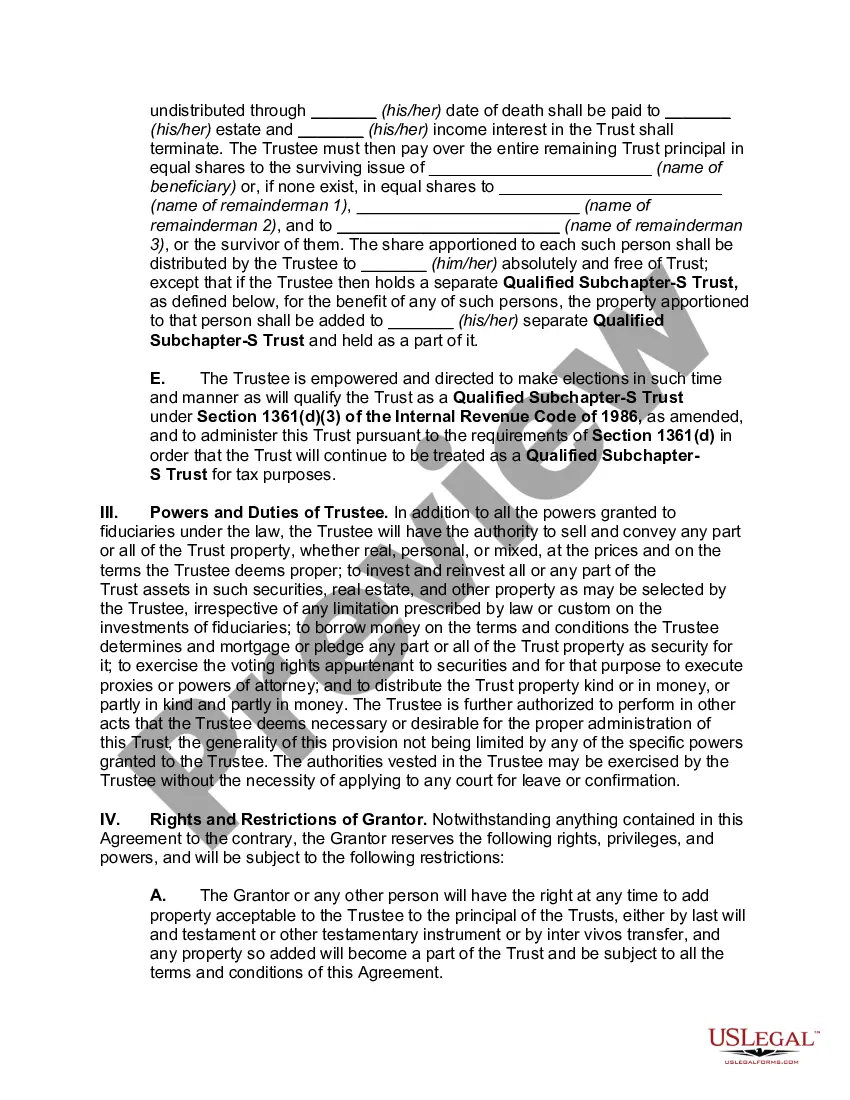

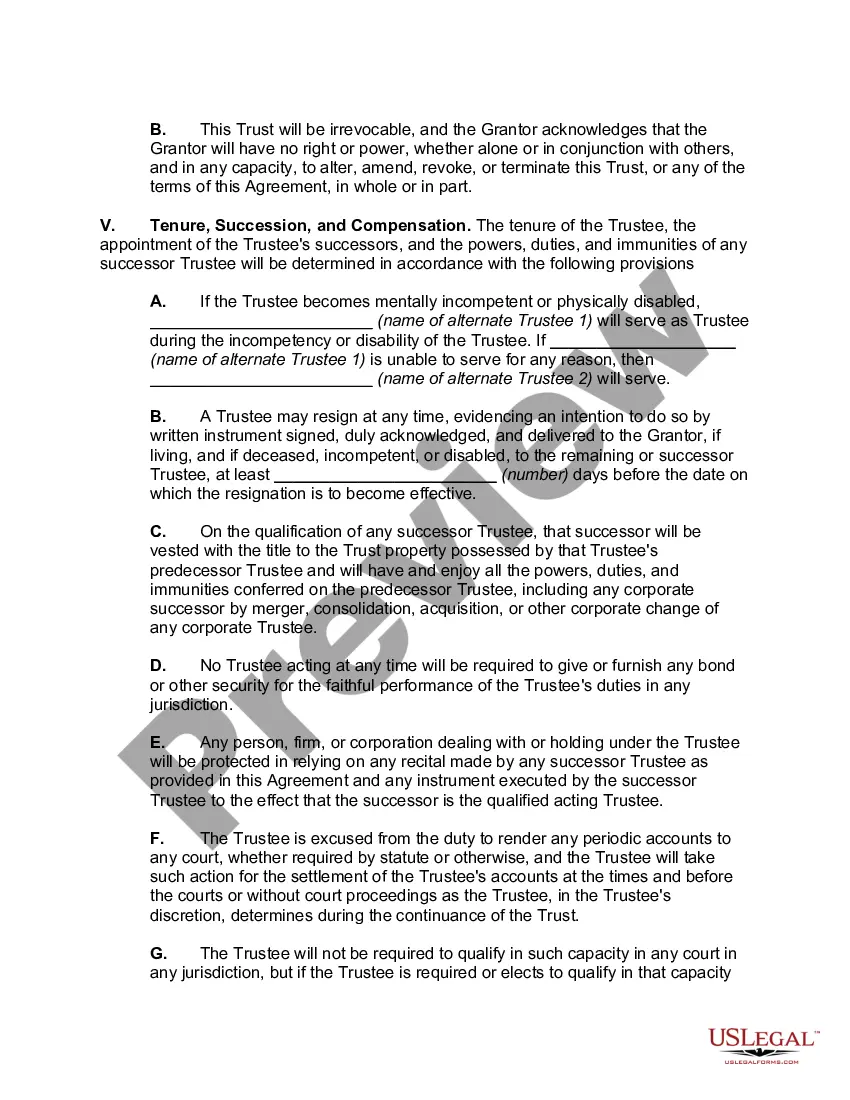

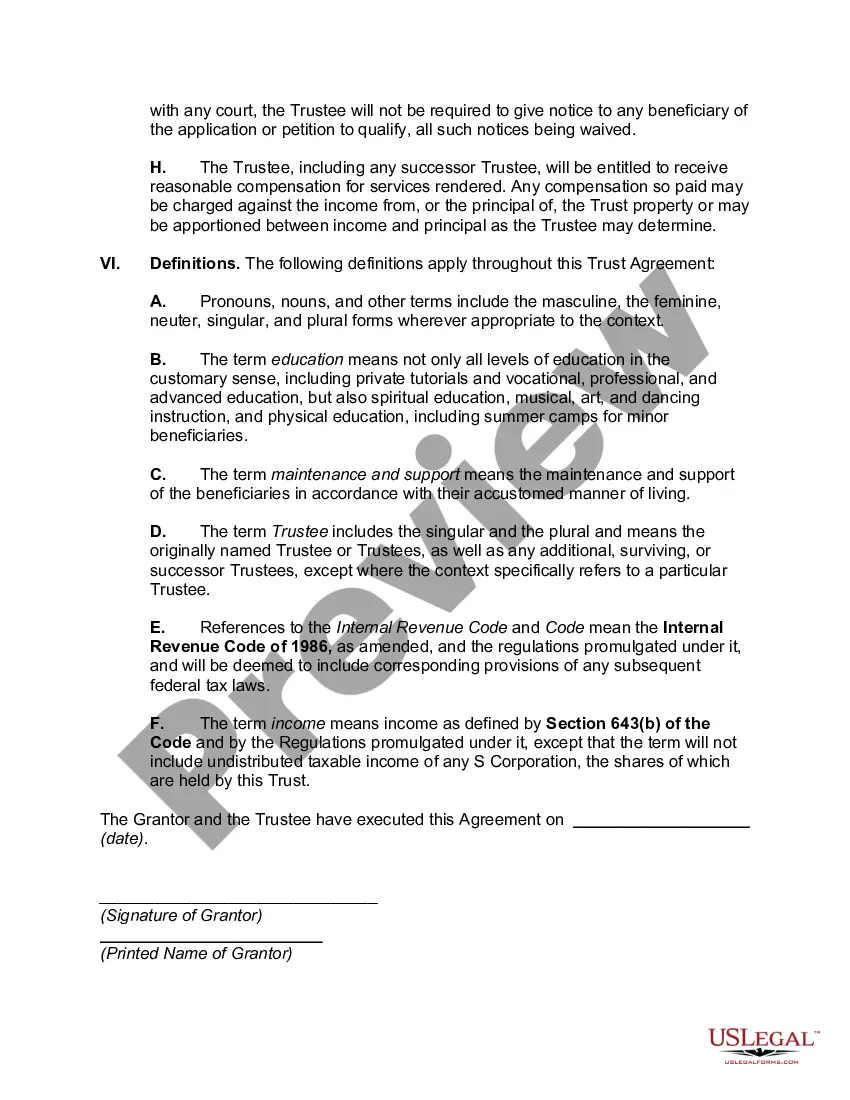

A Wake North Carolina Irrevocable Trust, which is a Qualifying Subchapter-S Trust, is a specific type of trust designed to meet the requirements set forth by the Internal Revenue Code (IRC) Section 1361(b)(3)(B). It allows the trust to qualify as an eligible shareholder for a Subchapter S corporation. Subchapter S corporations are small businesses that elect to be taxed under the Subchapter S of the IRC. This allows the corporation to avoid double taxation, with profits and losses passing through directly to shareholders' personal tax returns. The Wake North Carolina Irrevocable Trust that qualifies as a Subchapter-S Trust must adhere to several key criteria. Firstly, it must be a trust established under North Carolina law. To qualify, the trust must also be irrevocable, which means that it cannot be altered, amended, or terminated without the consent of the beneficiaries and the trustee. Furthermore, the trust must meet the qualifying requirements outlined in the IRC Section 1361(b)(3)(B). This includes limiting the trust's beneficiaries to individuals, estates, or specific types of trusts. The trust cannot have any non-resident alien individuals as beneficiaries. It should have only one class of stock and may not issue preferred stock. There are no specific types or variations of Wake North Carolina Irrevocable Trusts which are Qualifying Subchapter-S Trusts. However, there may be different variations of irrevocable trusts in general, such as charitable trusts, special needs trusts, or spendthrift trusts, among others. These types of trusts serve different purposes, cater to specific circumstances, and have distinct legal requirements. In summary, a Wake North Carolina Irrevocable Trust that qualifies as a Subchapter-S Trust is a trust established under North Carolina law. It must be irrevocable, limit beneficiaries to individuals or specific trusts, and adhere to the requirements of IRC Section 1361(b)(3)(B). By meeting these criteria, the trust can be considered an eligible shareholder of a Subchapter S corporation, allowing for advantageous tax treatment for the trust and its beneficiaries.

Wake North Carolina Irrevocable Trust which is a Qualifying Subchapter-S Trust

Description

How to fill out Wake North Carolina Irrevocable Trust Which Is A Qualifying Subchapter-S Trust?

Preparing legal paperwork can be cumbersome. Besides, if you decide to ask a lawyer to draft a commercial agreement, documents for proprietorship transfer, pre-marital agreement, divorce paperwork, or the Wake Irrevocable Trust which is a Qualifying Subchapter-S Trust, it may cost you a fortune. So what is the best way to save time and money and draw up legitimate forms in total compliance with your state and local laws and regulations? US Legal Forms is a great solution, whether you're searching for templates for your individual or business needs.

US Legal Forms is biggest online collection of state-specific legal documents, providing users with the up-to-date and professionally verified templates for any scenario accumulated all in one place. Consequently, if you need the latest version of the Wake Irrevocable Trust which is a Qualifying Subchapter-S Trust, you can easily find it on our platform. Obtaining the papers takes a minimum of time. Those who already have an account should check their subscription to be valid, log in, and select the sample with the Download button. If you haven't subscribed yet, here's how you can get the Wake Irrevocable Trust which is a Qualifying Subchapter-S Trust:

- Look through the page and verify there is a sample for your area.

- Check the form description and use the Preview option, if available, to make sure it's the template you need.

- Don't worry if the form doesn't suit your requirements - search for the correct one in the header.

- Click Buy Now once you find the needed sample and choose the best suitable subscription.

- Log in or sign up for an account to purchase your subscription.

- Make a payment with a credit card or via PayPal.

- Opt for the file format for your Wake Irrevocable Trust which is a Qualifying Subchapter-S Trust and download it.

Once finished, you can print it out and complete it on paper or import the samples to an online editor for a faster and more practical fill-out. US Legal Forms enables you to use all the documents ever purchased many times - you can find your templates in the My Forms tab in your profile. Try it out now!