San Diego California Sample Letter for Reinstatement of Loan - Compromise of Matter

Description

How to fill out Sample Letter For Reinstatement Of Loan - Compromise Of Matter?

How long does it usually take you to write a legal document? Because each state has its laws and regulations for every aspect of life, locating a San Diego Sample Letter for Reinstatement of Loan - Compromise of Matter that meets all local requirements can be tiring, and obtaining it from a professional lawyer is frequently expensive. Several online services provide the most common state-specific documents for download, but using the US Legal Forms database is most advantageous.

US Legal Forms is the largest online collection of templates, categorized by states and application areas. In addition to the San Diego Sample Letter for Reinstatement of Loan - Compromise of Matter, you can find any particular form to operate your business or personal matters, adhering to your regional needs. Professionals verify all samples for their legitimacy, allowing you to ensure that your documents are prepared accurately.

Utilizing the service is extremely straightforward. If you already possess an account on the platform and your subscription is active, you need only to Log In, choose the required form, and download it. You can access the file in your account at any time later. Alternatively, if you are a new user of the platform, there will be additional steps to take before you can obtain your San Diego Sample Letter for Reinstatement of Loan - Compromise of Matter.

Regardless of how many times you need to use the bought document, you can find all the templates you’ve ever downloaded in your account by selecting the My documents tab. Give it a go!

- Verify the content of the page you are viewing.

- Review the description of the template or Preview it (if available).

- Search for another form using the appropriate option in the header.

- Click Buy Now once you are confident in your selected file.

- Choose the subscription plan that fits you best.

- Create an account on the platform or Log In to move forward with payment options.

- Pay using PayPal or with your credit card.

- Adjust the file format if necessary.

- Click Download to acquire the San Diego Sample Letter for Reinstatement of Loan - Compromise of Matter.

- Print the document or utilize any preferred online editor to fill it out electronically.

Form popularity

FAQ

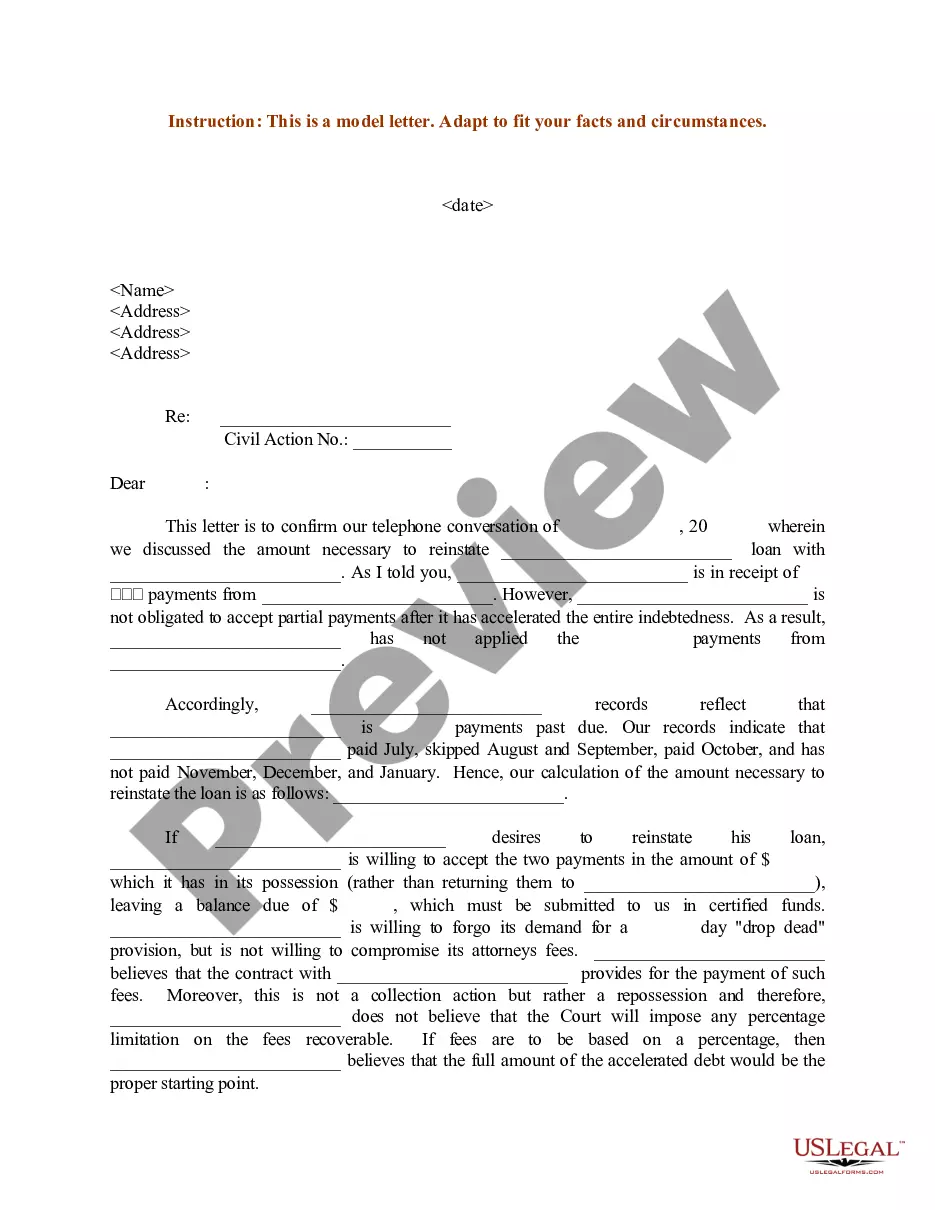

Some state laws let you reinstate your loan after a repossession if you can bring the loan current by paying the amount you are behind on your loan plus any costs the lender incurred during the repossession.

A reinstatement quote is what is given to a borrower that outlines what they owe. This will typically include: Back and current payments. Any late fees. Cost of property inspections.

Looking for Mortgage Analysis Services Homeowners are also allowed to negotiate the reinstatement of their mortgages loans with the lenders. Negotiating a reinstatement of a defaulted mortgage with the lender is a bit more involved than simply paying all missed payments and late fees, though.

Reinstatement Amount means the amount of Corporate Level Debt to the extent such obligations will be reinstated pursuant to the Plan, including, to the extent applicable, based on the elections of the holders of such Corporate Level Debt prior to the election deadline established by the Bankruptcy Court. Sample 2.

Foreclosure and Mortgage Reinstatement Regardless of the specific type of foreclosure in California, you always can reinstate your loan up to five days before your home's auction sale. To reinstate your mortgage in California you usually must pay your delinquent balance plus any late fees, at minimum.

Reinstatement involves making a single payment to catch up with everything due on a loan. By contrast, payoff involves paying the lender the total remaining balance of the loan. (Payoff before a foreclosure sale is commonly known as redemption, which is an equitable right available in every state.)

Mortgage reinstatement provides an option to avoid foreclosure. Instead, you can catch up on your payments and cover any late fees to restore the mortgage by paying the total amount past due. Once you are caught up, the defaulted mortgage will receive a clean slate.

Yes. For certain types of mortgages, after you sign your mortgage closing documents, you may be able to change your mind. You have the right to cancel, also known as the right of rescission, for most non-purchase money mortgages. A non-purchase money mortgage is a mortgage that is not used to buy the home.

In order to reinstate a loan, you need to make up any missed car payments plus any repossession fees in one lump sum. A reinstatement must be noted in your loan agreement, regardless of your state laws. If it's not listed, your lender isn't going to allow you to reinstate, even if you have the money to do so.

Reinstating a loan. A "reinstatement" occurs when the borrower brings the delinquent loan current in one lump sum. Reinstating a loan stops a foreclosure because the borrower catches up on the defaulted payments. The borrower also has to pay any overdue fees and expenses incurred because of the default.