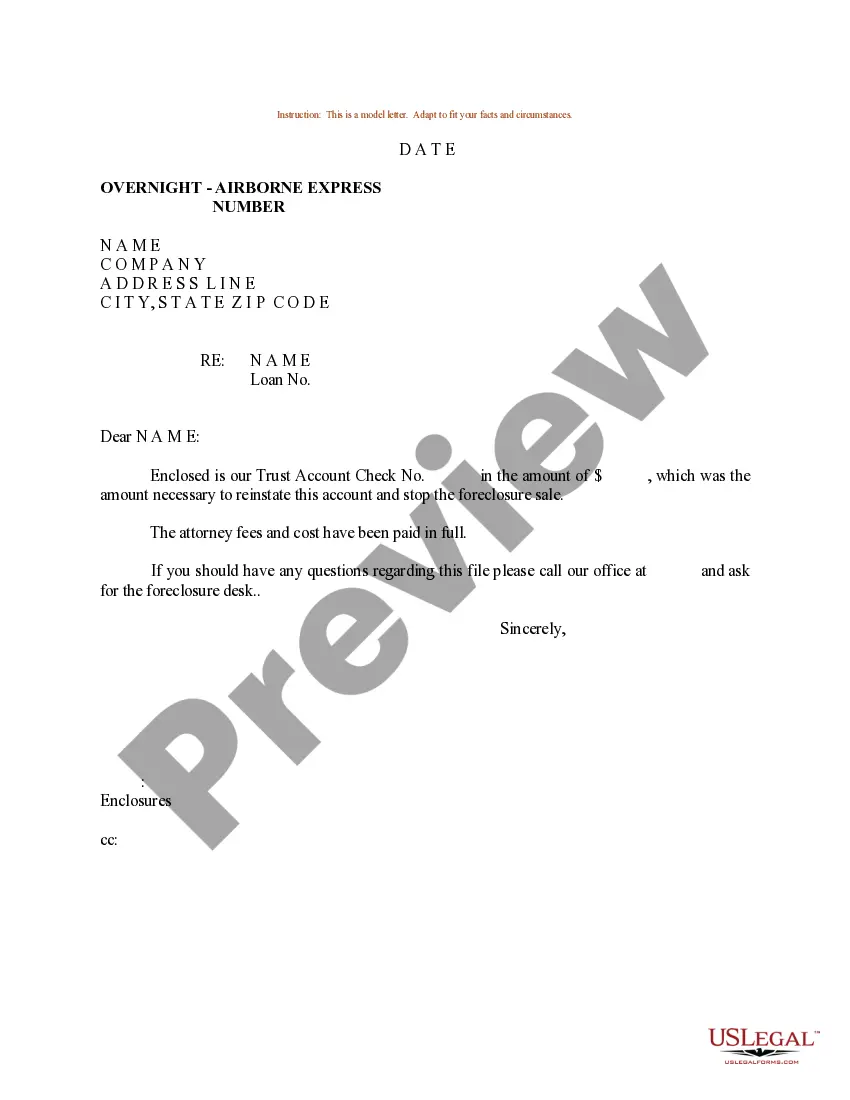

King Washington Sample Letter regarding Stop of Foreclosure Sale

Description

How to fill out King Washington Sample Letter Regarding Stop Of Foreclosure Sale?

How much time does it normally take you to draw up a legal document? Considering that every state has its laws and regulations for every life situation, locating a King Sample Letter regarding Stop of Foreclosure Sale meeting all regional requirements can be tiring, and ordering it from a professional attorney is often expensive. Many web services offer the most popular state-specific templates for download, but using the US Legal Forms library is most beneficial.

US Legal Forms is the most extensive web collection of templates, collected by states and areas of use. Apart from the King Sample Letter regarding Stop of Foreclosure Sale, here you can get any specific form to run your business or personal deeds, complying with your regional requirements. Specialists check all samples for their validity, so you can be sure to prepare your paperwork properly.

Using the service is fairly simple. If you already have an account on the platform and your subscription is valid, you only need to log in, choose the needed form, and download it. You can get the file in your profile at any moment later on. Otherwise, if you are new to the platform, there will be a few more actions to complete before you obtain your King Sample Letter regarding Stop of Foreclosure Sale:

- Check the content of the page you’re on.

- Read the description of the template or Preview it (if available).

- Look for another form utilizing the corresponding option in the header.

- Click Buy Now when you’re certain in the selected file.

- Choose the subscription plan that suits you most.

- Create an account on the platform or log in to proceed to payment options.

- Pay via PalPal or with your credit card.

- Change the file format if needed.

- Click Download to save the King Sample Letter regarding Stop of Foreclosure Sale.

- Print the doc or use any preferred online editor to complete it electronically.

No matter how many times you need to use the purchased template, you can find all the files you’ve ever downloaded in your profile by opening the My Forms tab. Give it a try!

Form popularity

FAQ

Reinstating the Loan Texas law allows the borrower to block a nonjudicial foreclosure sale by "reinstating" the loan (paying the overdue amount) within 20 days after the lender serves the notice of default by mail.

6 Ways To Stop A Foreclosure Work It Out With Your Lender.Request A Forbearance.Apply For A Loan Modification.Consult A HUD-Approved Counseling Agency.Conduct A Short Sale.Sign A Deed In Lieu Of Foreclosure.

To Whom It May Concern: I am writing this letter to explain my unfortunate set of circumstances that have caused us to become delinquent on our mortgage. We have done everything in our power to make ends meet but unfortunately we have fallen short and would like you to consider working with us to modify our loan.

Your letter should start with an introduction of who you are and what kind of loan you are applying for. Lead into your story with something like "We want to explain our foreclosure from six years ago." Then, launch right into the details that led you to lose your home. This is not the time to be shy or modest.

Your hardship letter will explain the hardship that has occurred that caused you to fall behind on your mortgage....Try to keep it simple. State the reason for the hardship in the opening paragraph.Explain how the hardship has ended, changed or is longer term.

How to write a letter of explanation The lender's name and address. Your name and your application number. The date you're submitting the letter and expected closing date (if you know it) A short statement that helps an underwriter fully understand your situation in regards to the reason for concern.

A "hardship letter" is a letter that you write to your lender explaining the circumstances of your hardship. The letter should give the lender a clear picture of your current financial situation and explain what led to your financial difficulties. The hardship letter is a normal part of the loss mitigation process.

Declare Bankruptcy To Stop Foreclosure Declaring bankruptcy in Texas is one option you have when deciding how to stop foreclosure proceedings. As soon as the petition is filed in court, an automatic stay is put in place that prevents a foreclosure from proceeding.

A demand letter simply restates the terms of the loan, and demands that the borrower rectify their accounts immediately. More common for a non-judicial foreclosure might be a breach letter, which is required before issuing an NOD.

Three of the most common methods of walking away from a mortgage are a short sale, a voluntary foreclosure, and an involuntary foreclosure. A short sale occurs when the borrower sells a property for less than the amount due on the mortgage.