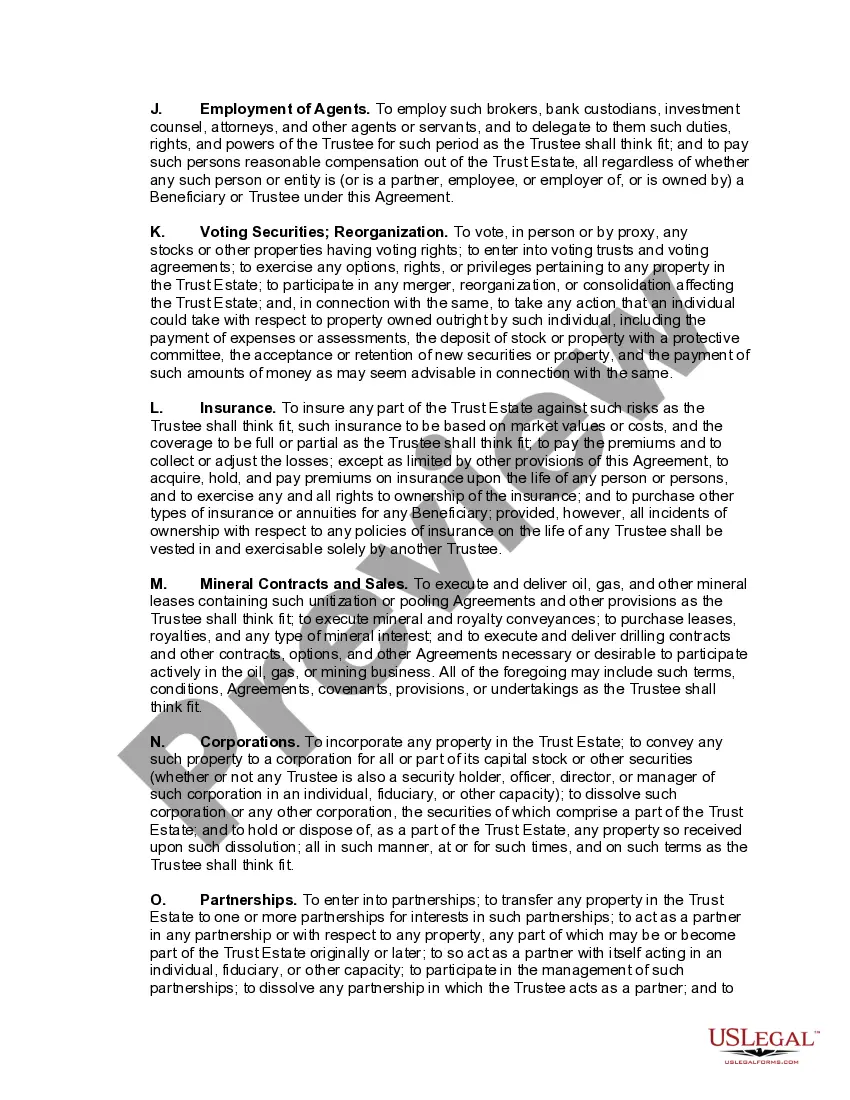

Minor Qualifying for Annual Gift-Tax Exclusion

Gifts in trust to minors are quite common, both as a means of building up a child's estate and as a way to minimize federal gift, income, and estate taxes payable by the trustor or the trustor's estate. A carefully drafted minor's trust can provide competent management of the property on the minor's behalf, while avoiding any problem of the minor's disability to act with respect to that property. Such a trust can effect substantial tax savings for the trustor-donor while regulating distribution of the trust income and principal in keeping with the needs of the minor.

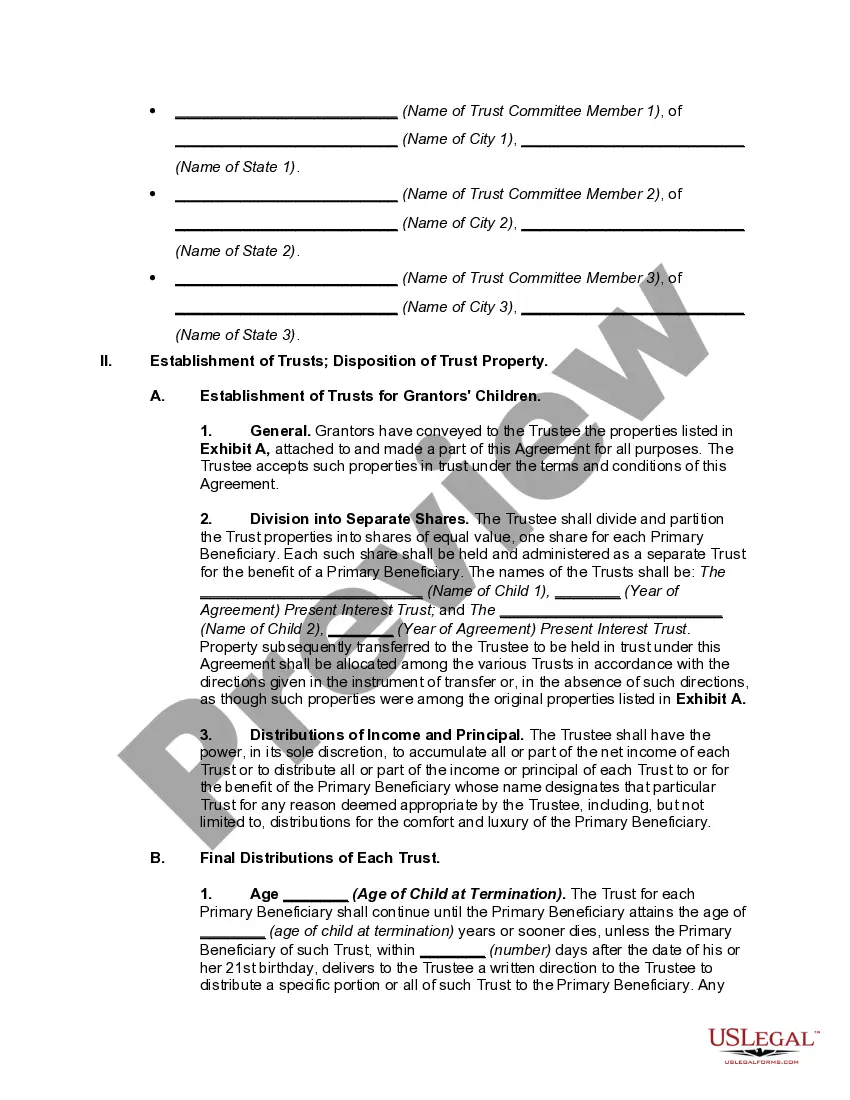

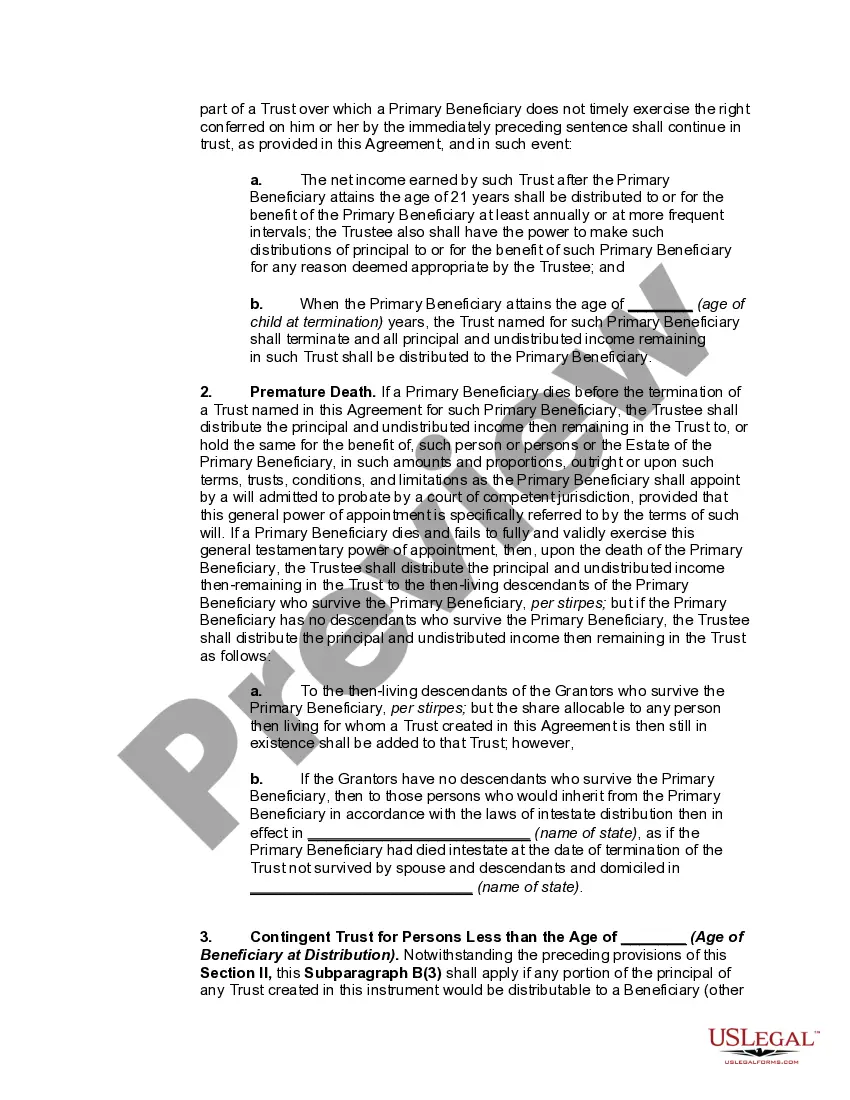

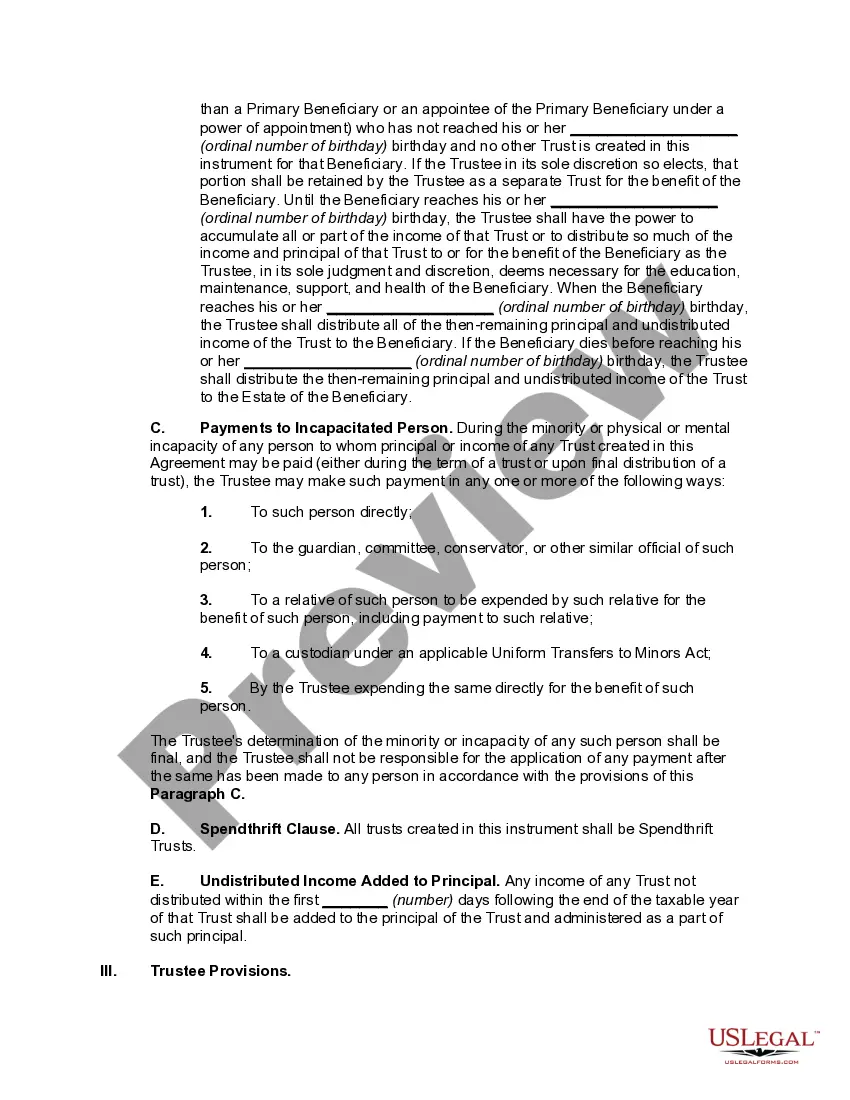

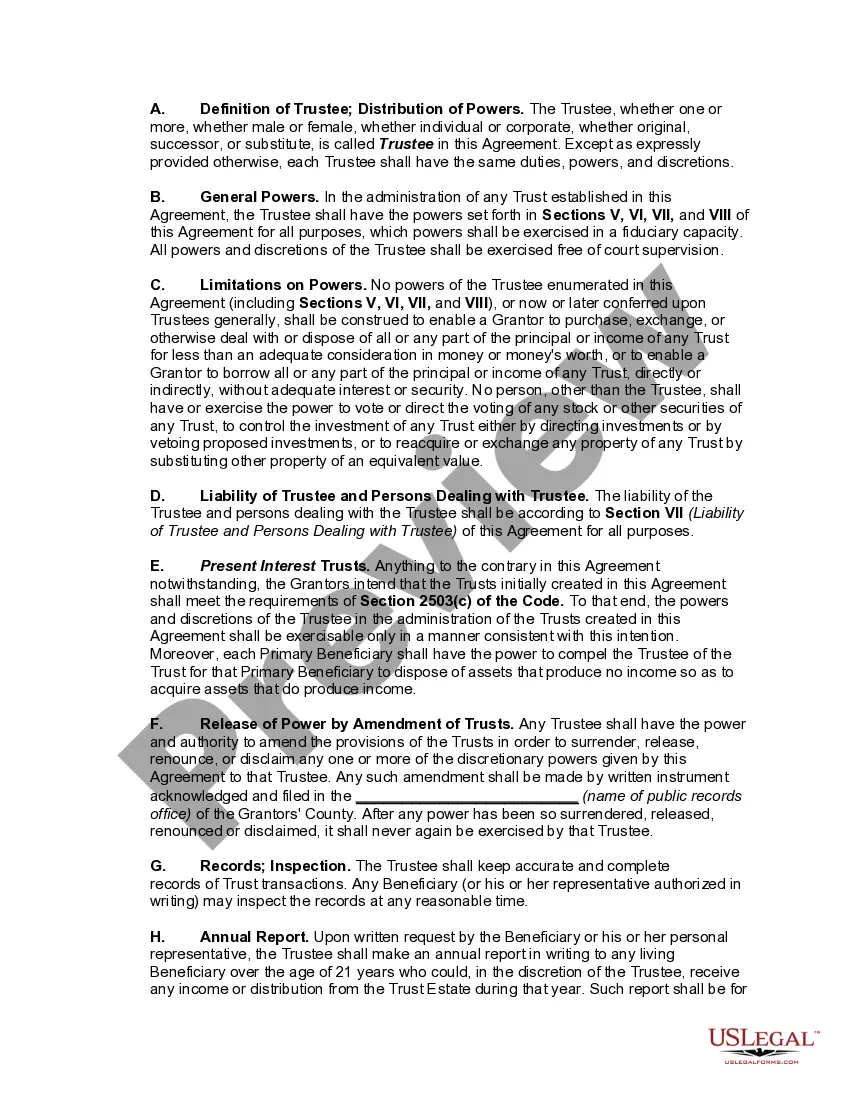

A section 2503(c) Minor's Trust is a separate legal entity (a trust) established to hold gifts in trust for a child until the child reaches age 21. The trust is named after the section of the Internal Revenue Code upon which it is based.

Normally, for a gift to qualify for the annual gift tax exclusion, it must be a gift of a present interest. This means the recipient must be able to use the gift immediately. A gift of a future interest in some property (e.g., the right to the money when the child turns 21) would not normally qualify, except for section 2503(c) of the Internal Revenue Code. Section 2503(c) sets out the conditions under which a gift of a future interest to a minor qualifies for the gift tax exclusion.

Aurora Colorado Multiple Trusts for Children -- Trust Agreement for Minor Qualifying for Annual Gift-Tax Exclusion

Category:

State:

Multi-State

City:

Aurora

Control #:

US-0977BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

Aurora borealis. noun. bright bands of color around the North Pole caused by solar wind and the Earth's magnetic field. Also called the northern lights.

Most Northern Lights are green in colour but sometimes you'll see a hint of pink, and strong displays might also have red, violet and white colours, often seen by aurora chasers on Northern Lights trips. The reason for all these colours lies in the composition of our earth's atmosphere.

Aurora is a mystical and romantic name that means "dawn" in Latin. An aurora also refers to a natural light display in the Earth's sky called the aurora polaris, or polar lights, visible only in high-latitude regions like the North and South Poles.

The most abundant gas is molecular nitrogen, and it radiates promptly in deep blue and red colors. Mixing these together gives purple. The bottom edge of a green auroral curtain gets this purple color when auroral elec-trons are accelerated to very high energy (Figures 7-8).

Aurora gained recognition with her debut extended play (EP), Running with the Wolves (2015), which contained the sleeper hit "Runaway". Later that year, she provided the backing track for the John Lewis Christmas advert, singing a cover of the Oasis song "Half the World Away".

Red Lights - Rare High Altitude Phenomenon Red is the rarest of the Northern Lights' colors and is created when solar particles collide with atomic oxygen at an altitude of over 241 kilometers (150 miles). At this altitude, the collisions are rare and produce a short-lived red flash.

Auroras can appear green, pink, dark red, blue, purple and even yellow!

The simple answer is that human eyes have difficulty perceiving the relatively ?faint? colors of the aurora at night.

Interesting Questions

More info

Get more help if you can't find an answer to your question. This guide is designed to help users complete the Plan Sets intake form.Choose one application and review your application checklist through MyAU once your application has been submitted. How Do You Use Our Forms? You can download, complete, and mail all forms to Aurora at the following address. Completing a One Medical Passport medical history online is easy. For most patients, filling out the entire questionnaire takes less than 30 minutes. Find registration forms you may need to acknowledge for your clinic or hospital visit to Aurora Health Care locations. OPTIONS TO SUBMIT AN APPLICATION FOR OPEN WAITING LISTS: All applications must be submitted online via the MyHousing Applicant Portal. Review that all the information has been filled out and photos are correctly linked.