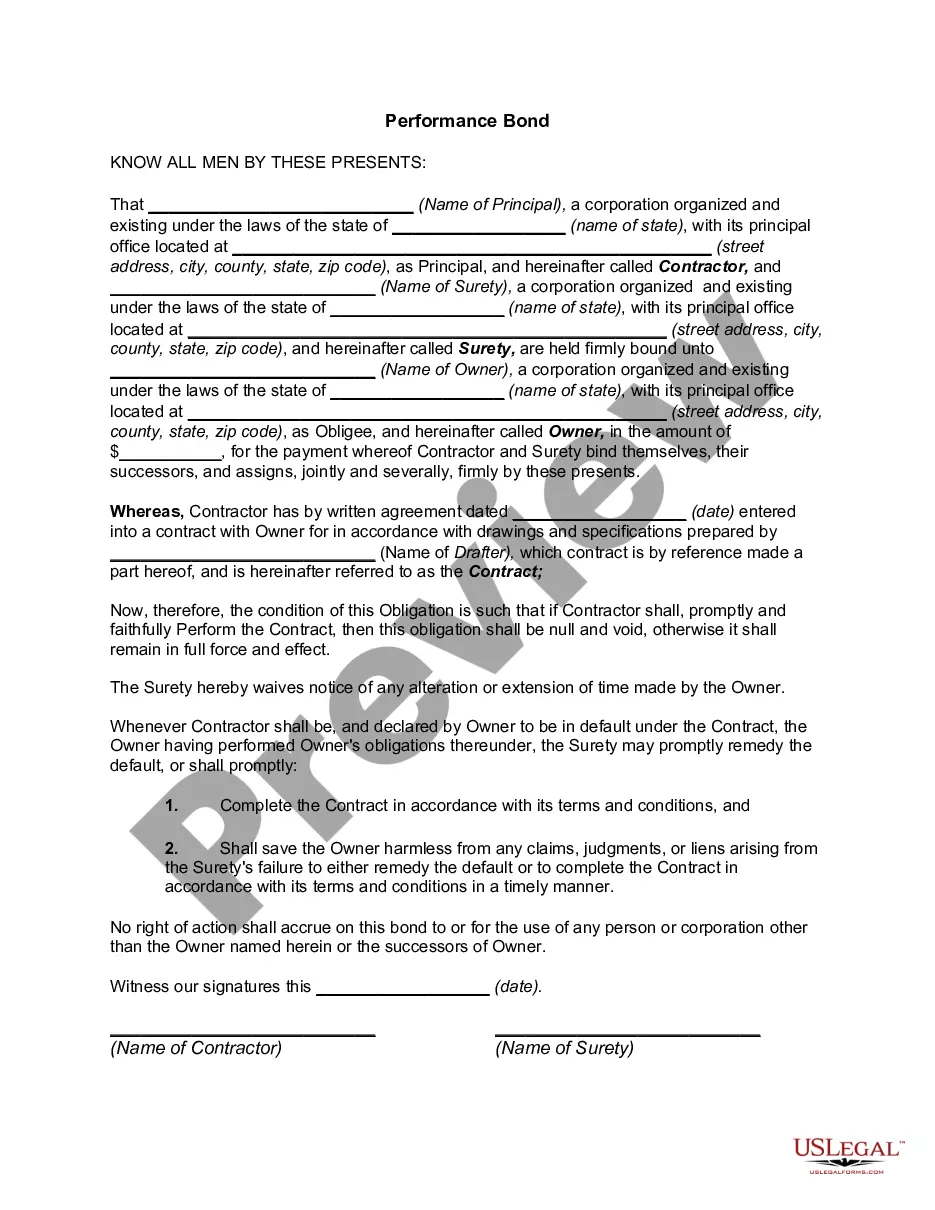

A Fairfax Virginia performance bond is a type of surety bond that ensures the successful completion of a construction project or other contractual obligations in Fairfax, Virginia. It acts as a protection for project owners (also known as obliges) against financial losses caused by default, non-compliance, or failure to meet the agreed-upon terms and conditions by the contractor (known as the principal). Performance bonds are a crucial aspect of construction projects as they provide financial security and peace of mind to both project owners and contractors. By issuing a performance bond, a bonding company or surety guarantees that the contractor will fulfill their contractual obligations, such as completing the project within the agreed-upon timeframe, meeting quality standards, and adhering to all applicable laws and regulations. In Fairfax, Virginia, there are various types of performance bonds available based on the specific requirements of the project: 1. Bid Bond: This type of bond is required during the bidding process and ensures that the contractor will enter into a contract if awarded the project. It provides the owner with compensation for any financial loss incurred if the contractor refuses to proceed after being awarded the contract. 2. Payment Bond: A payment bond guarantees that the contractor will pay all subcontractors, suppliers, and laborers involved in the project. It provides a safeguard for these parties, ensuring they will receive payment for their work and materials. 3. Maintenance Bond: A maintenance bond provides coverage for a specified period after the project's completion to protect against defects or faulty workmanship. It ensures that the contractor will rectify any issues that arise during this period. 4. Subdivision Bond: This bond is required when a contractor is developing a subdivision or public infrastructure project. It guarantees that the contractor will complete the project as specified and comply with all applicable regulations. 5. Supply Bond: A supply bond ensures that suppliers or manufacturers will provide the necessary materials as per the agreed-upon terms and conditions. It protects project owners from financial losses in the event of non-delivery or substandard supplies. When obtaining a Fairfax Virginia performance bond, contractors usually work with a surety company or bonding agency. These entities evaluate the contractor's financial strength, reputation, and ability to fulfill the contract requirements. The cost of the performance bond is typically a percentage of the total contract amount and varies depending on the contractor's creditworthiness and project scope. Overall, performance bonds play a vital role in ensuring the successful completion of construction projects in Fairfax, Virginia. They provide financial security, promote accountability, and protect the interests of project owners, contractors, and other parties involved.

Fairfax Virginia Performance Bond

Description

How to fill out Fairfax Virginia Performance Bond?

A document routine always accompanies any legal activity you make. Staring a business, applying or accepting a job offer, transferring ownership, and lots of other life situations demand you prepare official documentation that differs throughout the country. That's why having it all accumulated in one place is so helpful.

US Legal Forms is the most extensive online collection of up-to-date federal and state-specific legal forms. On this platform, you can easily find and download a document for any personal or business objective utilized in your region, including the Fairfax Performance Bond.

Locating forms on the platform is extremely simple. If you already have a subscription to our library, log in to your account, find the sample using the search field, and click Download to save it on your device. Following that, the Fairfax Performance Bond will be available for further use in the My Forms tab of your profile.

If you are using US Legal Forms for the first time, follow this simple guide to obtain the Fairfax Performance Bond:

- Ensure you have opened the right page with your local form.

- Use the Preview mode (if available) and browse through the template.

- Read the description (if any) to ensure the template corresponds to your needs.

- Look for another document via the search option in case the sample doesn't fit you.

- Click Buy Now once you find the necessary template.

- Decide on the appropriate subscription plan, then log in or create an account.

- Choose the preferred payment method (with credit card or PayPal) to proceed.

- Opt for file format and save the Fairfax Performance Bond on your device.

- Use it as needed: print it or fill it out electronically, sign it, and file where requested.

This is the easiest and most reliable way to obtain legal documents. All the samples available in our library are professionally drafted and verified for correspondence to local laws and regulations. Prepare your paperwork and manage your legal affairs efficiently with the US Legal Forms!