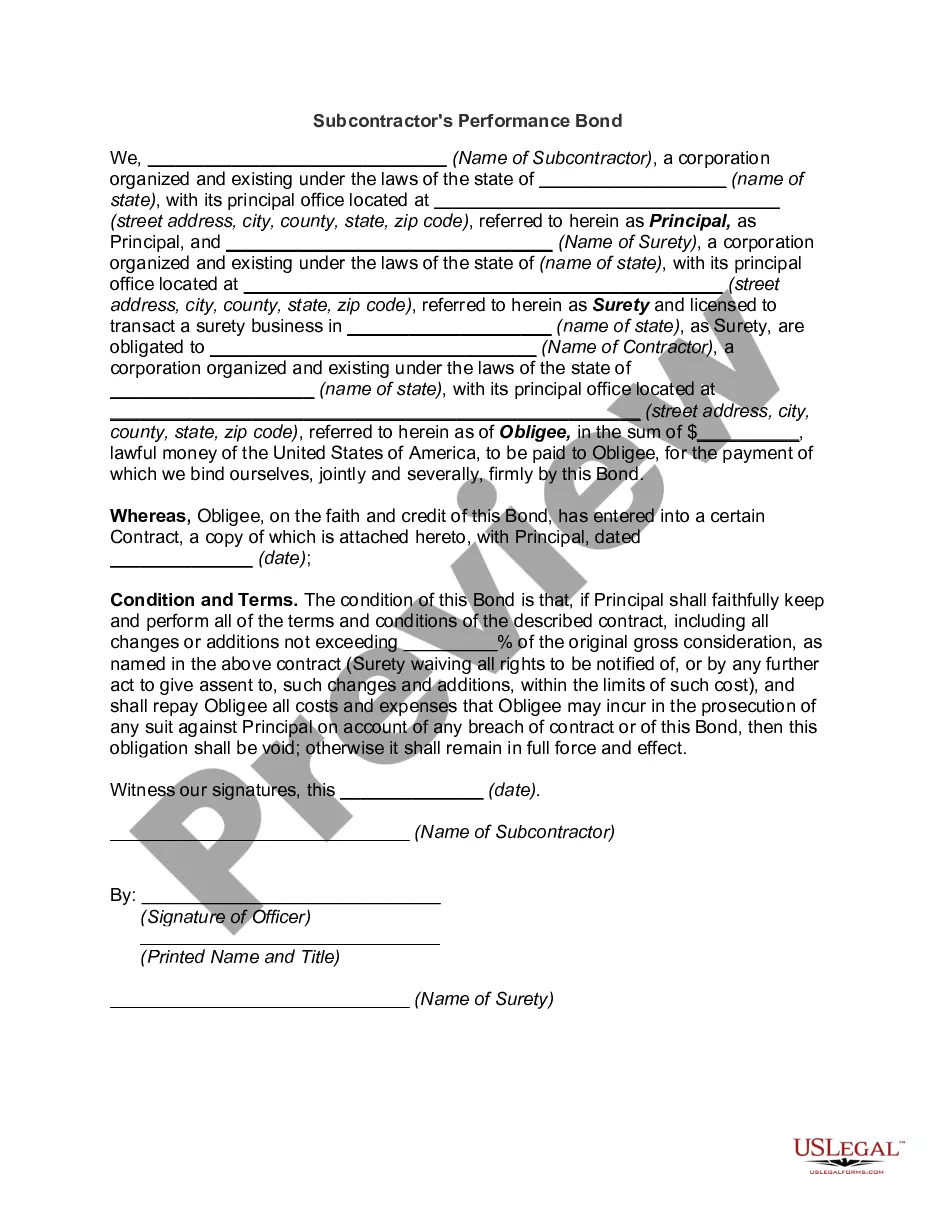

A Fairfax Virginia subcontractor's performance bond is a form of surety bond that provides assurance to project owners and general contractors in Fairfax, Virginia, that a subcontractor will fulfill its contractual obligations. It is a legally binding agreement between three parties: the subcontractor (the principal), the project owner or general contractor (the obliged), and the surety company (the issuer of the bond). Keywords: Fairfax Virginia, subcontractor's performance bond, surety bond, contractual obligations, project owner, general contractor, obliged, surety company. There are different types of Fairfax Virginia subcontractor's performance bonds designed to meet specific project requirements. The most common types include: 1. Bid Bond: This bond ensures that the subcontractor will execute the contract if awarded the project after winning a bid. It provides financial protection to the project owner or general contractor in case the subcontractor fails to enter into the contract. 2. Payment Bond: This bond guarantees that the subcontractor will make timely payments to suppliers, subcontractors, and laborers involved in the project. It protects the obliged from financial claims and ensures that all parties receive the due payment. 3. Performance Bond: This bond ensures that the subcontractor will perform the contracted work according to the agreed-upon terms, specifications, and timelines. It offers financial protection to the project owner or general contractor in case the subcontractor fails to complete the project or performs substandard work. 4. Maintenance Bond: Also known as a warranty bond, this type of bond guarantees the subcontractor's work for a specific period after project completion. It ensures that any defects or issues arising from the subcontractor's work will be rectified during the maintenance period, typically at the subcontractor's expense. 5. Supply Bond: This bond applies specifically to subcontractors involved in the supply or delivery of materials, equipment, or goods for a project. It guarantees that the subcontractor will fulfill their obligations related to the supply and ensures any potential losses are covered. 6. Subdivision Bond: This bond is required for subcontractors working on public infrastructure projects such as roads, bridges, and utilities. It ensures that the subcontractor will complete the project in compliance with all applicable laws, regulations, and specifications. Obtaining a Fairfax Virginia subcontractor's performance bond is often a prerequisite for subcontractors bidding on projects or entering into contracts with project owners or general contractors. It provides an added layer of financial security for all involved parties and helps facilitate smoother project execution and completion.

Fairfax Virginia Subcontractor's Performance Bond

Description

How to fill out Fairfax Virginia Subcontractor's Performance Bond?

Laws and regulations in every area differ around the country. If you're not a lawyer, it's easy to get lost in a variety of norms when it comes to drafting legal documents. To avoid pricey legal assistance when preparing the Fairfax Subcontractor's Performance Bond, you need a verified template valid for your county. That's when using the US Legal Forms platform is so helpful.

US Legal Forms is a trusted by millions online catalog of more than 85,000 state-specific legal templates. It's a perfect solution for specialists and individuals searching for do-it-yourself templates for different life and business scenarios. All the forms can be used multiple times: once you obtain a sample, it remains accessible in your profile for subsequent use. Therefore, if you have an account with a valid subscription, you can just log in and re-download the Fairfax Subcontractor's Performance Bond from the My Forms tab.

For new users, it's necessary to make a few more steps to get the Fairfax Subcontractor's Performance Bond:

- Analyze the page content to ensure you found the right sample.

- Utilize the Preview option or read the form description if available.

- Look for another doc if there are inconsistencies with any of your criteria.

- Utilize the Buy Now button to get the template once you find the correct one.

- Opt for one of the subscription plans and log in or create an account.

- Decide how you prefer to pay for your subscription (with a credit card or PayPal).

- Pick the format you want to save the document in and click Download.

- Fill out and sign the template on paper after printing it or do it all electronically.

That's the simplest and most economical way to get up-to-date templates for any legal scenarios. Find them all in clicks and keep your documentation in order with the US Legal Forms!